News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

First Digital, the issuer of the U.S. dollar stablecoin First Digital USD (FDUSD), is positioning stablecoins not as an end product but as foundational infrastructure for an emerging ‘AI agent’ economy—one in which autonomous software wallets can pay, route fees, allocate capital, and interact with tokenized real-world assets (RWAs) across blockchains.

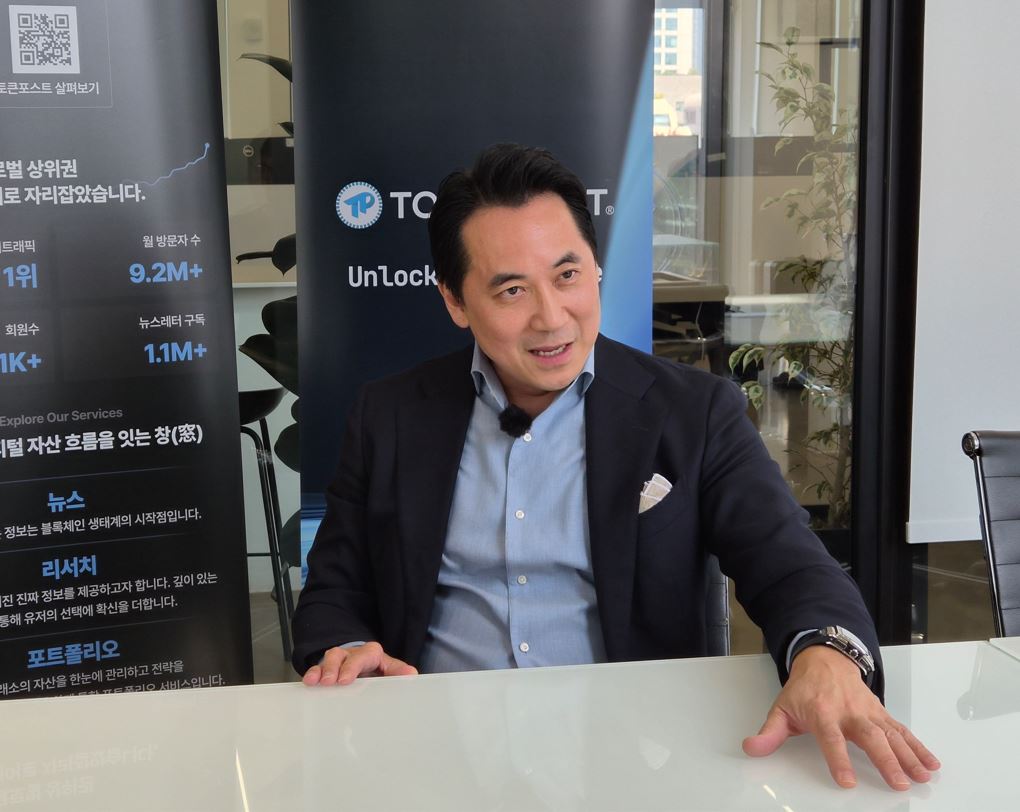

In an interview conducted on May 13 KST (May 13 UTC) in Seoul, First Digital founder and CEO Vincent Chok laid out a vision in which the company evolves beyond issuance into building a full-stack financial ecosystem where stablecoins are actively used in commerce and automated finance. The day before, on May 12 UTC, Chok presented at the Institutional Web3 Forum in Seoul, arguing that stablecoins are rapidly becoming core payment rails for AI-driven applications and outlining First Digital’s forthcoming platform, ‘Finance District’.

Chok’s framing reflects his background in traditional fiduciary services rather than crypto-native product cycles. Before moving into digital assets, he worked in trust and custody, pensions, inheritance structures, and real estate finance—experience that informs his emphasis on reserve management, audits, redemption mechanics, internal controls, and compliance. “If a trust is meant to last, the records must last as well,” he said, describing how questions around long-term recordkeeping and asset transfer pulled him toward blockchain’s utility beyond price speculation.

That approach, he argued, shaped First Digital’s evolution from institutional custody into stablecoins. “In traditional finance, custody is becoming close to free,” Chok said, describing margin compression that pushed the firm to expand into higher-value infrastructure. The pivotal lesson, he added, came from early conversations with a Tether co-founder: the essence of a stablecoin is not the token’s existence on-chain but the ‘trust structure’ behind it—where reserves sit, how they are verified, and whether the operational plumbing can withstand regulatory scrutiny and stress events.

First Digital launched FDUSD in June 2023, entering a market dominated by Tether (USDT) and Circle’s USD Coin (USDC). Chok acknowledged that timing helped—particularly as Binance phased out support for Binance USD (BUSD), leaving room for alternative dollar-denominated liquidity. But he insisted adoption was not simply opportunistic, saying First Digital won confidence by explaining its banking rails, treasury and reserve operations, and redemption design.

“Stablecoins look like something anyone can create,” Chok said. “But to build a successful stablecoin you need banks, exchanges, market makers, custody, and regulatory readiness. The first wall a new issuer hits is partnerships.” In his view, the competitive edge is less about which chain a stablecoin uses and more about the less visible machinery—accounting, attestations, tax and reporting obligations, AML standards, governance, and the ability to maintain consistent liquidity and redemptions across market conditions.

Chok described FDUSD’s differentiation in three areas: an operating footprint aligned with Asia’s banking and settlement rhythms, stronger utility during Asia trading hours, and what he called a conservative approach to reserve management and transparency, including regular attestation reports and multiple banking rails. FDUSD is available across several networks including BNB Chain, Ethereum (ETH), Sui, and Solana (SOL), though he stressed that technical deployment is the straightforward part compared with compliance and operational risk management.

He also addressed questions about Hong Kong’s developing stablecoin regulatory framework, saying First Digital has not applied for a Hong Kong dollar stablecoin license. While the firm has participated in regulatory discussions, its current focus remains on U.S. dollar stablecoins, he said. FDUSD’s issuer is based in the British Virgin Islands (BVI), while reserves are reportedly held with First Digital Trust, a Hong Kong-licensed trust company within the group. Chok characterized the structure as a deliberate separation between issuer operations and customer reserve assets—contrasting it with models where issuers both operate the business and directly control reserve management.

Still, the centerpiece of Chok’s Seoul message was not FDUSD’s market share, but what he sees as stablecoins’ next use case: automated payments and financial actions executed by AI agents. First Digital’s planned ‘Finance District’ platform is designed as a neutral layer connecting multiple stablecoins and blockchains, enabling AI agents to hold wallets, initiate transactions, and interact with savings and investment products. Two proposed components he highlighted are ‘Prism’, which automatically allocates transaction-related costs—such as gas fees, intermediary fees, and KYC/AML expenses—among participants, and ‘Vault’, a mechanism intended to route stablecoin deposits into RWA-linked strategies.

Chok illustrated Prism through an e-commerce scenario: a user instructs an AI agent to buy ingredients for a meal, after which the agent finds the items, orders them, and pays. Behind a single checkout, settlement would be split programmatically across the merchant, delivery provider, network fees, and platform commissions. “The user pays once, but in reality multiple parties must get paid,” Chok said. “Prism handles that distribution so each participant receives their share instantly at the moment of payment.”

On the investment side, Chok suggested AI agents could execute conditional strategies—such as incremental Bitcoin (BTC) buying when prices hit certain levels—by connecting to decentralized exchanges. For RWAs, he described Vaults as containers created by issuers of tokenized products—such as tokenized U.S. Treasuries, gold-linked tokens, or other real-world assets—where users deposit stablecoins and the vault executes a defined allocation or yield strategy. In his telling, the stablecoin itself is not promising yield; returns would come from the products or strategies the Vault deploys.

First Digital is also preparing a token called FDFI, which Chok described as a ‘rewards’ and ‘governance’ asset for the Finance District ecosystem. Users could earn FDFI by engaging with wallets, payments, and vault features, and it could later be used for platform access, payments, or AI usage credits. He said the firm does not want FDFI to become a superficial points program, and is exploring mechanisms that could tie value to underlying revenue streams—such as returns generated from FDUSD-based lending and borrowing—though he did not provide launch timelines or exchange partnerships beyond noting that a formal token reveal and major centralized exchange listings are being prepared.

Chok’s Seoul visit also included policy outreach. He said he met with South Korean lawmakers and industry stakeholders to discuss stablecoin regulation, and argued that Korea is well positioned to begin more formal debate given its advanced digital payments infrastructure and institutional interest. But he cautioned against copy-pasting overseas frameworks, emphasizing that a won-denominated stablecoin would face different constraints than dollar stablecoins due to currency convertibility, banking roles, and foreign-exchange considerations.

In his view, the most viable model would split responsibilities: banks contributing ‘trust’ through reserve custody and oversight, while tech firms handle tokenization, smart contracts, wallets, and user-facing payment flows. He pointed to Hong Kong’s iterative process—roundtables and multi-agency consultation—as a template for developing regulation that fits local markets rather than chasing a single global formula.

Asked whether First Digital would issue non-dollar stablecoins such as a won stablecoin, Chok suggested a partnership approach instead of direct issuance. Local issuers, he said, are better positioned to satisfy domestic regulatory requirements, while First Digital could provide custody, structural design, consulting, investment, and infrastructure connectivity. He tied that thesis back to Finance District, which he wants to function as an interchange layer where multiple licensed stablecoins can be swapped and used seamlessly—enabling scenarios such as foreign visitors converting into a won stablecoin inside their wallets and paying at merchants without visiting a traditional FX desk.

Beyond market efficiency, Chok framed the longer-term social impact around financial inclusion. He argued that stablecoins paired with AI wallets and fractional investing tools could lower access barriers for users underserved by traditional banking economics—particularly in regions where compliance costs discourage banks from servicing small-balance customers. The ultimate target, he said, is an environment where people can store value, invest in small increments across assets, and automate personal finance through agent-driven tools.

For Chok, the throughline is that stablecoins only matter if they become usable infrastructure outside exchanges. FDUSD, he insisted, is a starting point. The next phase is building systems in which autonomous agents can transact safely, distribute fees transparently, and allocate capital into regulated and tokenized products—provided that regulation, user experience, and security standards mature in parallel.

“We want to go beyond FDUSD,” Chok said, “and connect even underserved markets through the agent economy. Stablecoins are the critical starting point.”

🔎 Market Interpretation

- Stablecoins shifting from “product” to “infrastructure”: First Digital frames FDUSD as a baseline payment/settlement layer for an emerging AI-agent economy, where autonomous wallets can pay, split fees, and deploy capital programmatically.

- Competitive moat is operational trust, not chain choice: The article emphasizes that stablecoin defensibility is driven by reserve custody, redemption reliability, attestations/audits, banking rails, governance, AML, reporting, and stress resilience—more than technical issuance.

- Timing window aided adoption: FDUSD benefited from Binance’s BUSD wind-down, creating demand for alternative dollar liquidity, but First Digital argues execution and transparency converted that opening into sustained trust.

- Asia-centric positioning: FDUSD highlights utility during Asia trading hours and alignment with regional settlement rhythms, while remaining multi-chain (BNB Chain, Ethereum, Sui, Solana).

- Regulation and structure as a signaling tool: The BVI issuer + Hong Kong-licensed trust reserve custody model is presented as deliberate separation of operating entity and customer reserve assets—positioned as a risk-control and compliance-friendly architecture.

- Next battleground: “agentic” payments + tokenized yield rails: First Digital’s forthcoming “Finance District” aims to become a neutral interoperability layer across chains and stablecoins, targeting automated commerce and RWA-linked strategies.

💡 Strategic Points

- Partnerships are the first barrier to entry: Successful stablecoins require coordinated networks of banks, exchanges, market makers, custody providers, and compliance readiness; distribution and liquidity are as critical as issuance.

- Finance District as an interchange layer: Positioning the platform to connect multiple licensed stablecoins could reduce fragmentation and enable seamless conversion/use cases (e.g., travelers swapping into a local stablecoin in-wallet and paying merchants directly).

- Prism = programmable fee-routing for AI commerce: Designed to split a single user payment into multiple real-time settlements (merchant, delivery, gas/network fees, platform commissions, and potentially compliance-related costs), improving transparency and reducing reconciliation overhead.

- Vault = stablecoin on-ramp to RWA/tokenized strategies: Users deposit stablecoins into issuer-defined “containers” tied to tokenized Treasuries, gold, or other RWAs; yield is attributed to the underlying product/strategy—not the stablecoin itself—supporting clearer risk/return labeling.

- Token strategy (FDFI) aims to be utility-linked: Planned as rewards + governance, with exploration of tying value to platform revenue (e.g., lending/borrowing flows). Execution risks include regulatory classification, token incentive sustainability, and aligning emissions with real demand.

- Korea policy stance: avoid copy-paste frameworks: The article argues a won stablecoin differs materially from USD stablecoins due to FX constraints, convertibility, and banking roles; suggests a split model where banks provide reserve trust while tech firms deliver wallets, tokenization, and UX.

- Security and UX must mature with autonomy: AI agents executing payments/investments heighten requirements for permissions, transaction limits, audit trails, dispute handling, wallet security, and compliant identity workflows.

- Inclusion thesis depends on cost compression: If compliance and servicing costs can be automated/abstracted, stablecoins + AI wallets + fractional investing may open services to small-balance users underserved by traditional banking economics.

📘 Glossary

- Stablecoin: A blockchain token designed to track a stable reference value (commonly USD) and typically backed by reserves and redemption mechanisms.

- FDUSD: First Digital USD, a U.S. dollar stablecoin launched by First Digital in June 2023.

- USDT / USDC: Major USD stablecoins issued by Tether and Circle, respectively.

- Redemption: The process of exchanging stablecoins for the underlying fiat value (or equivalent) via the issuer/authorized channels—key for price stability and trust.

- Attestation: A third-party verification report (often periodic) describing reserve holdings and related controls; generally narrower than a full audit.

- Banking rails: The payment and settlement infrastructure (bank accounts, transfers, settlement networks) used to move fiat and manage stablecoin reserves.

- AML/KYC: Anti-Money Laundering / Know Your Customer compliance processes used to prevent illicit finance and verify user identity.

- AI agent economy: A market model where autonomous software agents (with wallets) can execute transactions, allocate capital, and interact with financial services under predefined rules.

- RWA (Real-World Asset): Off-chain assets (e.g., Treasuries, real estate, commodities) represented on-chain via tokenization.

- Tokenization: Converting rights to an asset or cash flow into tradable on-chain tokens.

- Gas fee: The network transaction fee paid to validators/miners on a blockchain (e.g., Ethereum) to process transactions.

- DEX (Decentralized Exchange): An on-chain marketplace for swapping tokens without a centralized intermediary.

- Finance District: First Digital’s planned platform intended to connect multiple stablecoins and blockchains for agent-driven payments and investment flows.

- Prism: A proposed Finance District component that programmatically allocates and distributes transaction costs and participant fees at payment time.

- Vault: A proposed mechanism routing stablecoin deposits into defined RWA-linked or strategy-based allocations, where yield stems from the underlying products.

- FDFI: A planned rewards/governance token for the Finance District ecosystem, potentially used for access, payments, or AI usage credits.

Comment 0