News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

The U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) have issued a joint interpretive framework that aims to clarify when a crypto asset should be treated as a security under federal securities laws—an attempt to narrow one of the industry’s most persistent legal blind spots. Framed as a 'Token Taxonomy', the guidance introduces five categories that will influence whether the SEC, the CFTC, or other regulators take the lead.

The guidance, released Wednesday ET, groups digital assets into 'Digital Commodity', 'Digital Collectible', 'Digital Tool', 'Stablecoin', and 'Digital Security'. While the agencies describe it as interpretive rather than legislative, the taxonomy is likely to shape compliance strategies, listing decisions, and token design choices across U.S.-facing crypto businesses.

Digital commodities: 16 tokens explicitly named

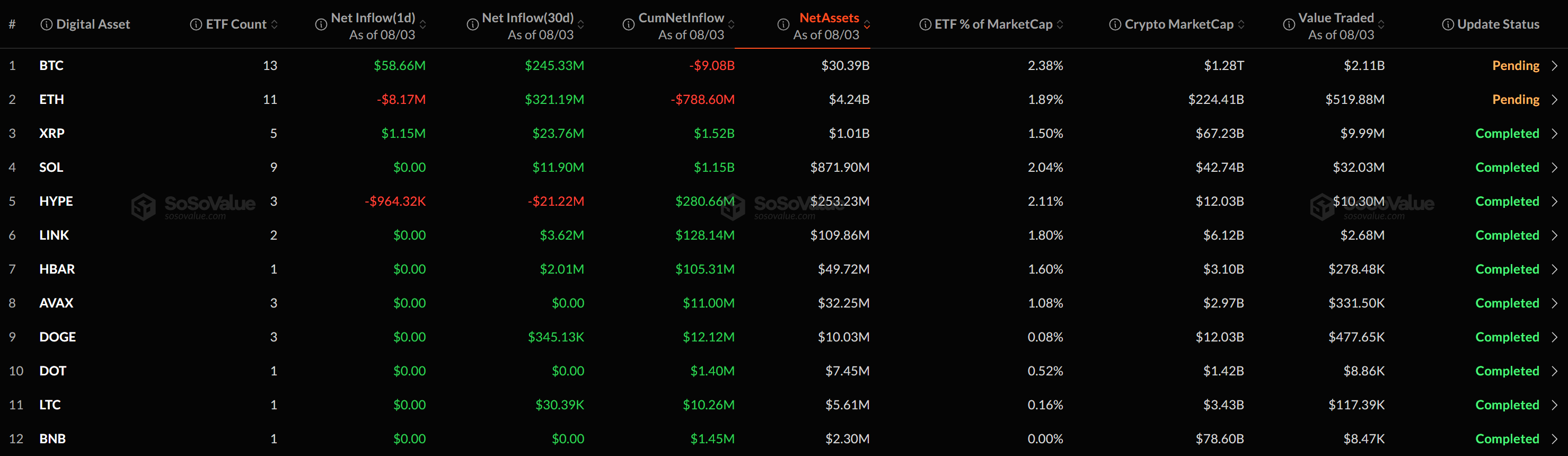

In the most market-moving section, the SEC explicitly identified 16 tokens as non-security 'digital commodities': Bitcoin (BTC), Ethereum (ETH), Solana (SOL), XRP (XRP), Cardano (ADA), Avalanche (AVAX), Aptos (APT), Bitcoin Cash (BCH), Chainlink (LINK), Dogecoin (DOGE), Hedera (HBAR), Litecoin (LTC), Polkadot (DOT), Shiba Inu (SHIB), Stellar (XLM), and Tezos (XTZ).

The document does not provide token-by-token reasoning, but it emphasizes that these assets do not meet the legal definition of a 'security'. It further notes that, with the exception of certain payment stablecoins that meet the forthcoming GENIUS Act standard, most crypto assets could still be treated as 'commodities' under the Commodity Exchange Act—bringing them into the CFTC’s oversight perimeter.

Market participants quickly focused on the breadth of the list, which includes both large-cap networks and meme-linked assets such as Dogecoin (DOGE) and Shiba Inu (SHIB). The guidance also points to additional assets that could plausibly fall into the digital commodity category—though not formally designated—including BONK, Ethereum Classic (ETC), HYPE, Stacks (STX), Sui (SUI), Bittensor (TAO), TRON (TRX), and Monero (XMR).

Digital collectibles: NFTs, fan tokens, and meme coins—unless fractionalized

The agencies also formalized 'digital collectibles' as a category covering crypto assets that represent or convey rights tied to art, music, video, trading cards, gaming items, and related cultural objects. Notably, the guidance states that meme coins can fall into this bucket—an acknowledgement that many such tokens trade more like cultural artifacts than productive assets.

The SEC cited CryptoPunks, Chromie Squiggles, fan tokens, dogwifhat (WIF), and VCOIN as examples. It also addressed a long-running hypothetical often raised in U.S. policy debates—whether a “tokenized Pokémon card” could be a security—suggesting it may qualify as a 'digital collectible', while adding that more facts would be needed to reach a definitive conclusion.

A key carve-out is likely to matter for NFT marketplaces and structured products: most 'fractionalized collectibles' may be securities because they tend to rely on the managerial efforts of others, an echo of the SEC’s longstanding Howey-based analysis. The guidance adds that a meme coin could shift categories over time—moving from collectible status to 'digital commodity' if it develops established functionality within an ecosystem.

Digital tools: membership, credentials, and non-transferable badges

A third category, 'digital tools', covers tokens designed for specific functional purposes rather than passive profit participation. The SEC describes many of these as potentially 'soulbound'—non-transferable tokens commonly used for identity, reputation, or access control.

To qualify, the token should not embed economic rights such as passive yield, profit-sharing, or claims on business revenue. The guidance points to use cases like memberships, tickets, credentials, proofs of ownership, and identity badges, mentioning Ethereum Name Service (ENS) domains and CoinDesk’s 'Microcosms' NFT-based Consensus ticket as illustrative examples. Market observers said projects like World ID, VeeFriends, and POAP could be assessed similarly depending on their design and distribution.

Stablecoins: GENIUS Act compliance as the dividing line

For payment stablecoins, the SEC says it will treat stablecoins meeting the GENIUS Act definition—scheduled to take effect in January—as non-securities and will not impose separate SEC registration requirements for issuance and redemption activities. Still, the guidance underscores that stablecoins remain subject to potentially extensive oversight from other regulators, reflecting the broader policy view that stablecoins sit at the intersection of payments, banking, and consumer protection.

Until the GENIUS Act takes effect, the SEC indicates that a narrower group of 'covered stablecoins' can be treated as non-securities if they do not pay interest or yield to holders and are backed solely by U.S. dollars or highly liquid, low-risk assets. USD Coin (USDC), PayPal USD (PYUSD), USAT, and KlarnaUSD were referenced as meeting these conditions.

Digital securities: Howey remains the gatekeeper

On the most contentious question—what constitutes a 'digital security'—the SEC reiterates that any asset failing the Howey Test is a security. Tokenized versions of already-regulated instruments, such as tokenized money market funds and tokenized equities, are also categorized as digital securities.

At the same time, the guidance states that certain activities are not, by themselves, treated as securities issuance: protocol mining and staking, 'wrapping' of non-security crypto assets, and certain types of airdrops. The effort is likely meant to separate network-level technical processes from capital-raising schemes, though the boundaries may still be litigated in practice.

For many lawyers and issuers, the central frustration remains: the SEC still does not provide a bright-line checklist for identifying digital securities beyond a case-by-case assessment of facts, including how a token was promoted and marketed. That uncertainty has historically affected early-stage projects that sell tokens while promising future utility, as promotional language can tilt an analysis toward an 'investment contract'.

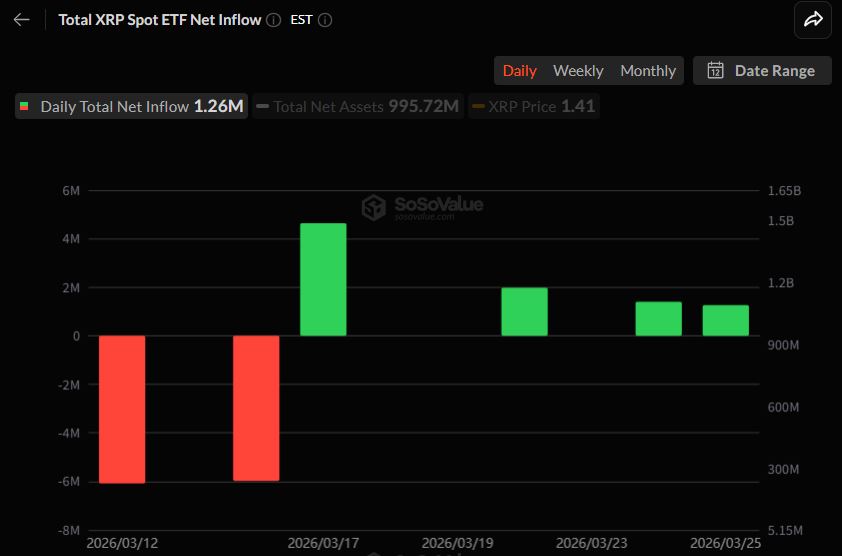

Why XRP’s placement will be closely watched

One of the most scrutinized inclusions is XRP (XRP). Despite prior court findings that certain sales were unregistered investment contracts under federal securities laws, the guidance places XRP among the non-security digital commodities. Market participants said that juxtaposition highlights the SEC’s attempt to separate an asset’s general status from specific distribution methods—an approach that, if adopted consistently, could reshape how exchanges and issuers evaluate legal exposure.

Market implications: more clarity, but not a full safe harbor

Overall, the taxonomy is being welcomed as a meaningful step toward regulatory clarity for major assets that have long traded in a legal gray zone. Still, the guidance preserves substantial ambiguity where it matters most for token issuers: the digital security category remains heavily dependent on facts and messaging rather than objective technical criteria.

Industry participants also caution that even assets placed in non-security categories—digital commodities, collectibles, tools, and qualifying stablecoins—could still trigger securities-law scrutiny if they are packaged, marketed, or sold in a manner that resembles an 'investment contract'. In that sense, the taxonomy may narrow uncertainty around asset types, while keeping the focus on distribution behavior—an outcome that could push projects toward more conservative launches in the U.S. market.

🔎 Market Interpretation

- Regulatory signal: The SEC and CFTC jointly introduced an interpretive “Token Taxonomy” to reduce uncertainty on when a crypto asset is treated as a security versus a commodity, influencing which regulator leads (SEC, CFTC, or others).

- Immediate market impact: The SEC explicitly named 16 tokens as non-security digital commodities (including BTC, ETH, SOL, XRP, ADA, DOGE, SHIB), a de-risking cue for listings and U.S.-facing market structure—though not a full immunity from enforcement.

- Behavior over label: Even if an asset fits “commodity/collectible/tool/stablecoin,” distribution and marketing can still create securities exposure (i.e., an investment-contract framework can override category expectations).

- NFT/meme coin reframing: The guidance treats many NFTs and even meme coins as “digital collectibles” (cultural/tradable artifacts), but warns that fractionalization often increases the chance of securities treatment.

- Stablecoin wedge: A key dividing line becomes GENIUS Act compliance (effective January). Before then, only non-yielding, conservatively backed “covered stablecoins” are signaled as non-securities.

- XRP spotlight: XRP’s inclusion as a non-security “digital commodity” despite prior case outcomes suggests an emerging distinction between an asset’s general status and specific sale methods—potentially reshaping exchange risk frameworks.

💡 Strategic Points

- Exchanges/listings: Treat the 16 named “digital commodities” as stronger candidates for U.S. availability, but maintain controls around how tokens are promoted, yield programs, and packaging that could resemble an investment product.

- Token issuers: Align token design and go-to-market with the category you want:

- Commodity path: Emphasize decentralized functionality and avoid issuer-led profit narratives.

- Collectible path: Frame as cultural/consumer item; avoid fractional structures and “managerial efforts” profit pitches.

- Tool path: Keep utility narrow and explicit; avoid embedded economic rights (yield, revenue share, passive profit expectation).

- Stablecoin path: Prepare for GENIUS Act standards; avoid yield/interest features if aiming for non-security treatment.

- NFT marketplaces & structuring desks: Reassess fractionalized NFTs, vault/pooled ownership, and revenue-sharing wrappers—these are highlighted as higher probability “digital securities.”

- DeFi protocols: The statement that mining, staking, wrapping, and certain airdrops are not automatically securities issuance may reduce some operational fear, but distribution incentives and marketing still matter.

- Compliance playbook update: Build an internal “taxonomy + Howey overlay” review:

- Classify the token by function (commodity/collectible/tool/stablecoin/security).

- Run a separate Howey / investment-contract analysis on specific offers, incentives, and communications.

- Document decentralization/functionality milestones if arguing a shift over time (e.g., meme coin evolving from collectible to commodity).

- Watchlist assets: The guidance hints that assets like BONK, ETC, STX, SUI, TAO, TRX, XMR could plausibly fit “digital commodity” characteristics without formal designation—useful for scenario planning, not reliance.

📘 Glossary

- Token Taxonomy: An interpretive classification system introduced jointly by the SEC/CFTC to group crypto assets into functional categories that influence regulatory posture.

- Digital Commodity: A crypto asset the SEC indicates does not meet the definition of a security; often implies possible CFTC commodity oversight under the Commodity Exchange Act.

- Digital Collectible: Tokens tied to cultural/consumer items (art, music, gaming items, fan tokens, some meme coins). May become a security if structured like an investment (e.g., fractionalization, manager-led profit expectations).

- Fractionalized Collectible: A collectible split into shares or pooled interests; often treated like an investment product due to reliance on third-party management and profit expectation.

- Digital Tool: Utility-focused tokens (often non-transferable “soulbound” style) used for access, identity, credentials, tickets—should avoid yield, profit-share, or revenue claims.

- Soulbound Token: A typically non-transferable token used for identity/reputation/access control, reducing “trading for profit” characteristics (though not dispositive).

- Stablecoin (Payment Stablecoin): A token designed to maintain a stable value (often pegged to USD). The SEC points to GENIUS Act compliance as the key non-security condition going forward.

- GENIUS Act standard: Referenced forthcoming legal standard (effective January) that the SEC plans to use to treat qualifying payment stablecoins as non-securities for issuance/redemption.

- Covered Stablecoin: Pre-GENIUS category signaled as non-security if non-yielding and backed by USD or highly liquid low-risk assets (examples cited: USDC, PYUSD, USAT, KlarnaUSD).

- Digital Security: A token that satisfies securities-law criteria (primarily via the Howey Test) or tokenized versions of regulated instruments (e.g., tokenized equities, money market funds).

- Howey Test: The U.S. legal test for an “investment contract” (a type of security), focusing on investment of money, common enterprise, expectation of profits, and reliance on the efforts of others.

- Wrapping: Creating a tokenized representation of another asset (e.g., wrapped BTC). The guidance says wrapping non-security crypto isn’t, by itself, securities issuance.

- Airdrop: Token distribution to users (often promotional or incentive-based). The guidance suggests certain airdrops are not automatically securities issuance, depending on facts.

Comment 0