News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Crypto markets digested a mix of regulatory milestones, institutional positioning, and notable on-chain flows this week, with fresh data showing public companies ramping up Bitcoin (BTC) accumulation even as broader indicators continue to point to a subdued risk environment.

According to a monthly update cited by Odaily and shared by BitcoinTreasuries.net, publicly listed companies bought roughly 110,000 BTC in the second quarter of 2026. The tracker said that figure was about 1.8 times the combined net buying seen across the prior two quarters, underscoring sustained 'institutional demand' for Bitcoin as corporate treasuries expand digital asset exposure.

In the U.K., Coinbase ($COIN) said it has received authorization from the Financial Conduct Authority (FCA) to offer investment services, enabling the exchange to provide crypto, equities, and derivatives through a single platform. Coinbase said the approval falls under the MiFID framework, which allows regulated firms to offer trading and investment services across a broader set of financial instruments.

The company said advanced traders will be able to access crypto, equities, and commodity-linked perpetual futures, while retail users will gain access to stock trading. Coinbase also outlined plans to expand into stablecoin-based payments, savings and lending products, derivatives, and tokenized real-world assets—an effort to position itself as a multi-asset venue as traditional finance and crypto rails converge. Coinbase already holds an electronic money institution license in the U.K. and is registered as a cryptoasset service provider.

Despite the corporate bid for BTC, on-chain and market-structure signals suggest bearish pressure has remained persistent. The Block, citing Glassnode data, reported that Bitcoin has traded for five consecutive months below both the 'realized price'—a proxy for the market’s average cost basis—around $76,600, and the short-term holder cost basis around $72,200. Glassnode data also showed long-term holder loss selling rising sharply, with the share of loss-related realized value increasing from about 15% in February to roughly 43% more recently. Daily realized losses briefly reached $280 million, the largest reading since December 2022.

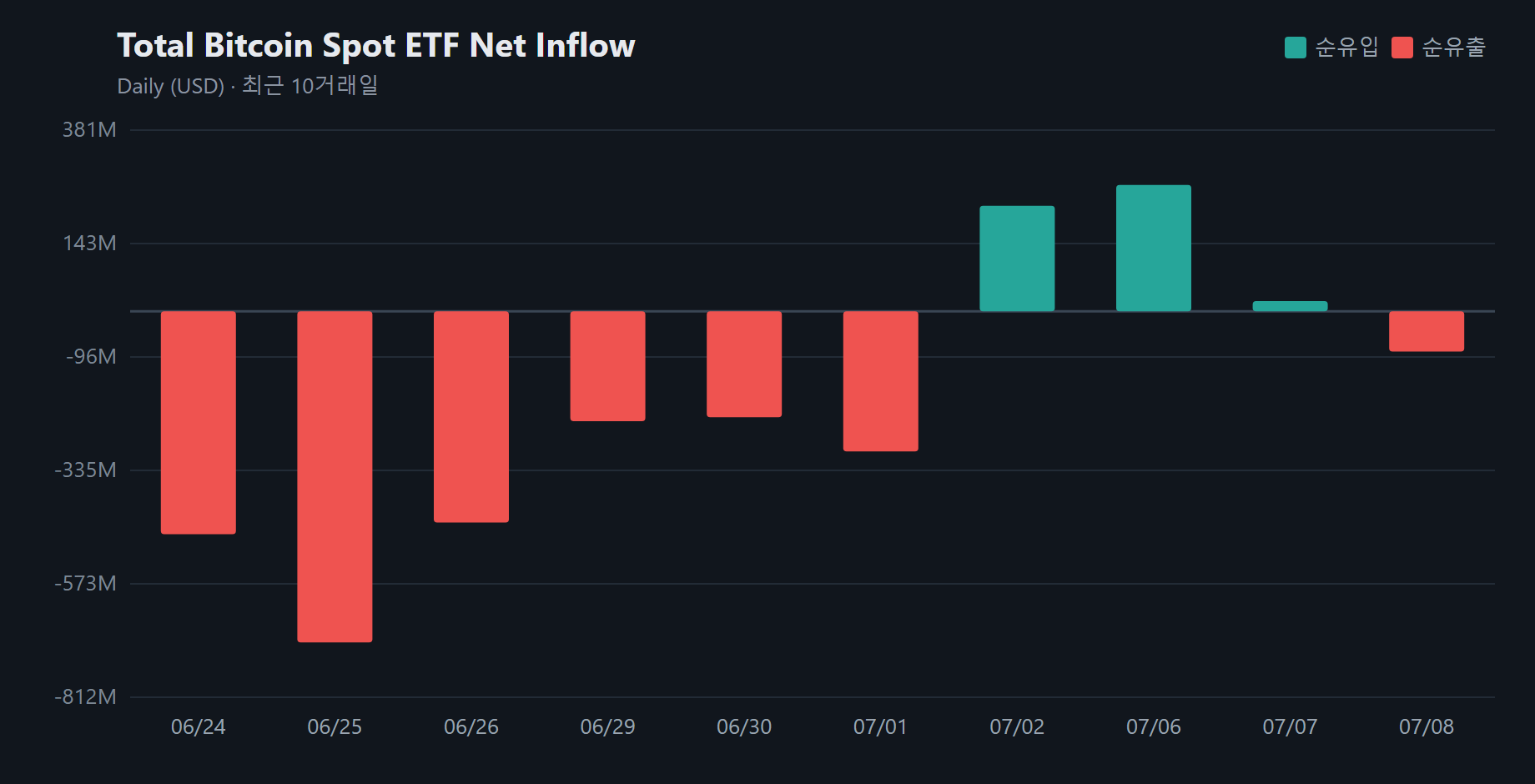

Institutional flow data has also softened. Spot Bitcoin ETFs in the U.S. turned to net outflows after mid-May, according to the report, with the 30-day average daily net outflow peaking near $193 million in early June before easing to around $89 million. Derivatives markets have shown signs of 'deleveraging' alongside a tilt toward long positioning, but analysts said on-chain indicators and institutional flows have yet to signal a decisive rebound.

Regulatory scrutiny remained in focus in the U.S. as well. The Information reported, cited by Cointelegraph and relayed by PANews, that the U.S. Department of Justice warned internal staff that Binance’s cooperation in crypto-related investigations could diminish. Binance denied the report, saying its cooperation with law enforcement has not changed and will not change.

In Europe, OSL Group said its subsidiary OSL EU secured a Markets in Crypto-Assets Regulation (MiCAR) license from Austria’s Financial Market Authority (FMA), registering as a crypto-asset service provider (CASP). The license allows the firm to use the EU’s 'passporting' regime to offer regulated digital asset services across 30 European Economic Area (EEA) jurisdictions. OSL EU said it will provide custody, spot trading, fiat on/off-ramps and exchange services, and crypto transfers for institutional and eligible clients under FMA supervision.

The approval arrives as the bloc tightens the transition from legacy national registrations to full CASP status. While more than 1,200 crypto firms have held country-by-country registrations across the EU, only about 210 have reportedly converted to formal CASP licenses ahead of the July 1, 2026 deadline.

ETF flow data showed weakness extending beyond Bitcoin. SoSoValue data indicated that U.S.-listed spot Solana (SOL) ETFs recorded total net outflows of $8.65 million on July 8 ET. The largest daily redemption came from Bitwise Solana Staking ETF (BSOL), which lost $6.61 million, while Grayscale Solana Trust (GSOL) saw $2.04 million in net outflows. Total net assets across the spot SOL ETF category stood near $894 million, with cumulative net inflows of about $1.14 billion.

On-chain watchers also flagged several large transfers whose intent was not immediately clear. Whale Alert reported that 827 BTC—worth roughly $52.1 million at the time—moved on July 9 from Coinbase Institutional to an unidentified wallet. Separately, about 190.7 million USD Coin (USDC), valued at approximately $190.8 million, was transferred on July 8 from Aave to an unidentified whale wallet, a move that can be associated with 'liquidity management' or position adjustments in lending markets. Whale Alert also tracked a transfer of about 1.2319 billion Ethena (ENA), worth roughly $94.1 million, between unidentified wallets on July 9.

In index-product news, Bitwise added Hyperliquid (HYPE) to the Bitwise 10 Crypto Index ETF (BITW), according to a report cited by Wu Blockchain. Bitwise said the rebalance was based on market-cap rankings and weight optimization, with HYPE taking an approximate 0.95% allocation after inclusion. The report noted Hyperliquid recorded $1.34 trillion in trading volume and $320 million in revenue in the first half of 2026, while HYPE was up roughly 165% year-to-date. Stellar (XLM) was also added, while Polkadot (DOT) and Avalanche (AVAX) were removed.

Taken together, the developments highlight a market split between ongoing institutional buildout—through corporate BTC accumulation and regulatory licensing—and a more cautious trading backdrop reflected in ETF outflows and elevated loss realization. The coming weeks will test whether regulatory clarity and product expansion can translate into sustained 'liquidity inflow' amid still-fragile sentiment.

🔎 Market Interpretation

- Corporate Bitcoin bid strengthens: Publicly listed companies purchased ~110,000 BTC in Q2 2026 (about 1.8× the combined net buying of the prior two quarters), signaling ongoing treasury-led accumulation even as broader risk appetite remains muted.

- Price still below key cost bases: Bitcoin has traded five straight months below both the realized price (~$76.6k) and the short-term holder cost basis (~$72.2k), consistent with lingering bearish market structure.

- Capitulation pressure increasing: Long-term holder loss selling is rising (loss-related realized value share ~15% → 43%), and daily realized losses briefly hit $280M (largest since Dec 2022), highlighting stress beneath the surface.

- Institutional vehicles losing momentum: U.S. spot BTC ETFs shifted to net outflows after mid-May; 30-day avg daily outflows peaked near $193M in early June and eased to ~$89M, implying weaker marginal demand through ETFs.

- Regulatory ‘two-speed’ backdrop: Coinbase gained U.K. FCA authorization under a MiFID framework to broaden into a multi-asset venue, while Europe continues MiCAR conversion—only ~210 firms reportedly converted to CASP licensing out of ~1,200 registrations ahead of the July 1, 2026 deadline.

- Scrutiny persists around major exchanges: Reports that DOJ warned Binance cooperation could diminish were denied by Binance, keeping compliance and enforcement risk in focus for market participants.

- Alt exposure also seeing outflows: U.S.-listed spot SOL ETFs recorded net outflows of $8.65M (July 8 ET), suggesting the risk-off tone is not limited to Bitcoin products.

- Large on-chain transfers add uncertainty: Notable moves (e.g., 827 BTC from Coinbase Institutional; 190.7M USDC from Aave; 1.2319B ENA between unknown wallets) can indicate liquidity rebalancing, collateral shifts, or strategic positioning—without immediate directional clarity.

- Index products are rotating toward newer liquidity centers: Bitwise added Hyperliquid (HYPE) (~0.95% weight) and Stellar (XLM) while removing DOT and AVAX, reflecting changing market-cap rankings and trading activity concentration.

💡 Strategic Points

- Separate “treasury demand” from “tradable liquidity”: Corporate BTC accumulation can be sticky but may not immediately lift prices if ETF flows and derivatives positioning remain cautious; track whether ETF outflows stabilize as a condition for broader upside participation.

- Watch realized price & STH cost basis as regime markers: Sustained reclaim of ~$72.2k (STH) and ~$76.6k (realized price) would signal improving market footing; continued rejection keeps downside/sideways risk elevated.

- Monitor loss realization for “seller exhaustion” clues: Spikes like the $280M realized-loss day can precede stabilization if followed by declining loss volume; persistence would imply ongoing distribution and fragile sentiment.

- Regulatory licensing as a growth catalyst—timing matters: Coinbase’s U.K. approval and OSL’s MiCAR license can expand product scope (multi-asset trading, tokenized RWAs, payments), but market impact depends on actual user migration and capital deployment, not announcements alone.

- EU MiCAR transition risk/opportunity: Firms missing CASP conversion may face operational constraints; compliant venues could gain market share via passporting across ~30 EEA jurisdictions—potentially reshaping liquidity venues in Europe.

- DeFi stablecoin movements can foreshadow leverage shifts: Large USDC withdrawals from lending venues (e.g., Aave) may imply collateral repositioning, risk reduction, or preparation for OTC/spot deployment; confirm with utilization rates, borrowing APRs, and TVL changes.

- Alt product flows as sentiment barometer: SOL ETF outflows alongside BTC ETF outflows suggest broad risk aversion; a turn in SOL flows can act as an early read on re-risking appetite.

- Index rebalances may drive marginal demand: Additions (HYPE, XLM) can see temporary inflow support from index-linked buying; removals (DOT, AVAX) may face mechanical selling pressure around rebalance windows.

📘 Glossary

- Realized Price: The average on-chain cost basis of all coins (price at last movement). Trading below it often indicates broad unrealized losses and weaker sentiment.

- Short-Term Holder (STH) Cost Basis: Average cost basis of recently acquired coins (commonly ~155 days). Trending below it signals newer buyers are underwater.

- Long-Term Holder (LTH) Loss Selling: When older holders realize losses by spending/selling coins. Rising LTH loss realization can indicate capitulation or late-cycle stress.

- Realized Loss: The dollar value of losses locked in when coins are sold/spent below their acquisition cost basis.

- Spot ETF Net Flows: Net creations/redemptions in ETF shares that reflect aggregate investor demand. Sustained outflows often pressure spot market liquidity conditions.

- Deleveraging: Reduction of leveraged positions in derivatives (closing longs/shorts), typically lowering open interest and dampening volatility temporarily.

- MiFID: EU/UK regulatory framework governing investment services and market operations. Authorization can enable broader offerings (e.g., equities, derivatives) under regulated standards.

- FCA: The U.K. Financial Conduct Authority, responsible for regulating financial firms and markets.

- MiCAR: The EU’s Markets in Crypto-Assets Regulation—harmonizes crypto regulations across the EU, including licensing and consumer protections.

- CASP: Crypto-Asset Service Provider—an entity licensed under MiCAR to offer services like custody, exchange, and transfers.

- Passporting (EEA): Ability for a licensed financial firm in one EEA jurisdiction to offer services across other EEA countries under a common regulatory regime.

- Perpetual Futures: Derivative contracts with no expiry; prices track spot via funding rates. Can amplify leverage-driven moves.

- Tokenized Real-World Assets (RWAs): Traditional assets (e.g., bonds, funds, commodities) represented on-chain via tokens to enable programmable settlement and broader accessibility.

Comment 0