News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Global finance giants are accelerating their push into crypto rails, with reports that Visa, Mastercard, BlackRock, and Coinbase are preparing to co-launch a joint stablecoin called OUSD—an initiative that underscores the industry’s growing focus on regulated, fiat-linked digital dollars as both payments infrastructure and a strategic liquidity layer.

WatcherGuru reported that Visa, Mastercard, BlackRock, Coinbase, and American Express are among the firms involved in the planned launch. While key details—such as the issuing entity, reserve composition, and regulatory domicile—were not disclosed in the report, the move lines up with a broader shift: major payment networks and asset managers are increasingly treating stablecoins as a scalable settlement medium rather than a niche crypto product.

The timing is notable. Regulators globally are tightening rules around issuance, custody, and distribution of stablecoins, while institutions are simultaneously testing tokenized cash and treasury-like instruments to reduce settlement friction. In that context, a consortium-style approach could be interpreted as an attempt to pool compliance capabilities, distribution reach, and market credibility—particularly if OUSD is designed for use across consumer payments, cross-border transfers, and on-exchange liquidity.

In Europe, the regulatory clampdown is already reshaping the competitive landscape. The European Union’s Markets in Crypto-Assets framework, known as MiCA, entered into force on Tuesday Eastern Time (July 1). Citing CoinDesk, PANews reported that crypto-asset service providers must now obtain licenses or exit the market. Of roughly 3,000 unlicensed crypto trading platforms operating across Europe, about 80% could face shutdown risk or may halt services for local users if they fail to meet requirements within the deadline.

The potential consumer impact could be substantial. The report estimated that more than 10 million users could be affected, potentially forcing a migration toward compliant venues—an outcome that may consolidate liquidity among regulated exchanges and custodians while reducing access to high-risk offshore products.

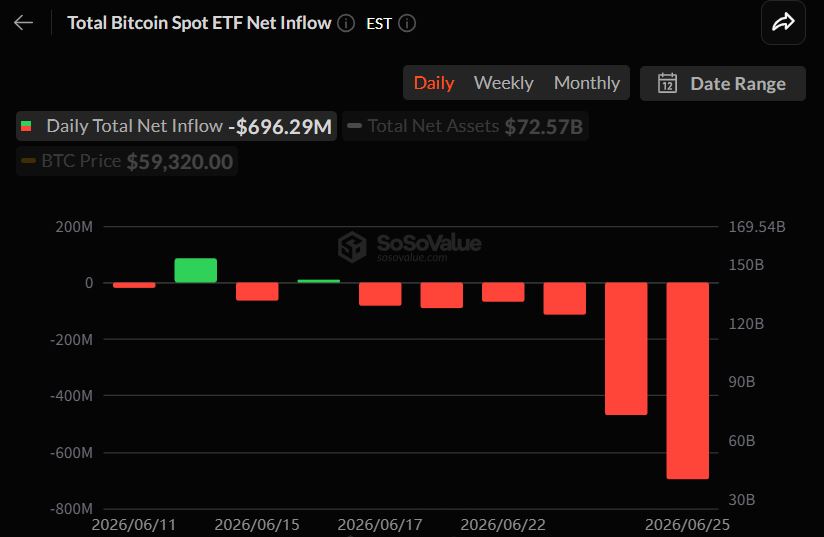

In the U.S., investor appetite for certain crypto market vehicles appears to have cooled. Spot Bitcoin (BTC) ETFs in the United States recorded net outflows of $4.5 billion in June, marking the worst monthly performance since their January 2024 launch, according to The Block via PANews. The data is being read by market participants as a signal that ‘institutional demand’ has softened—at least temporarily—amid changing macro expectations and ongoing debates over the longer-term role of ETFs as a primary gateway for traditional allocators.

At the same time, the U.S. Securities and Exchange Commission is widening its policy lens. According to ODaily, the SEC is soliciting public comment on a range of ‘new ETF’ concepts that include virtual-asset-related funds, investment opportunities built on blockchain technology, and event contracts—products that can resemble derivatives. The consultation suggests regulators are attempting to calibrate standards that balance financial innovation with risk controls as interest grows in ETFs offering onchain exposure and novel payoff structures.

Elsewhere in Asia, Taiwan passed a bill to establish a dedicated crypto regulatory framework, WatcherGuru reported. The legislation is aimed at formalizing oversight of local digital-asset markets, bringing crypto businesses into the regulated perimeter and improving regulatory clarity—an increasingly common policy direction among jurisdictions seeking to retain fintech competitiveness while reducing consumer and systemic risk.

On the adoption narrative, Coinbase executive John D’Agostino said in a CNBC interview that more than 40 countries have committed to acquiring Bitcoin in some form to incorporate it into national treasury frameworks, according to a repost shared by Bitcoin Magazine. While the claim is difficult to independently verify from the interview excerpt alone, it reflects the ongoing conversation around sovereign and quasi-sovereign BTC accumulation—whether through direct holdings, state-linked investment vehicles, or strategic reserves.

Corporate treasury dynamics were also in focus after a claim circulated about potential selling pressure from Strategy, one of the most prominent corporate Bitcoin holders. Bitcoin Historian said on X that Bloomberg raised the possibility Strategy could be forced to sell more than $1 billion worth of BTC to meet payment and financial obligations. The comments, as relayed, were not accompanied by a confirmed company announcement, and no verified sale plan has been disclosed.

On the technical side of the Bitcoin ecosystem, long-time Bitcoin Core contributor and BIP maintainer John Atack advised users to avoid sending Bitcoin during the second week of August, according to Bitcoin News via PANews. Atack cited the need for caution until the risk of potential chain reorganization fades during an upcoming network change. He said he intends to monitor developments by running both Core and Knots version 110 and to segregate holdings—remarks that arrive amid renewed community debate over implementation choices and governance tensions.

Legal risks around crypto platforms remain elevated. Reuters reported that around 1,700 UK investors have filed a group lawsuit against Binance and founder Changpeng Zhao, seeking at least £150 million in damages. Plaintiffs allege Binance sold high-risk derivatives, including leveraged products, to UK retail customers without regulatory authorization from late 2019, breaching the Financial Services and Markets Act. Binance said it will defend the claims but declined further comment on ongoing litigation. The UK’s Financial Conduct Authority barred crypto firms from offering derivatives to retail clients in 2021, after which Binance moved to restrict access for UK users.

In the U.S., prosecutors announced another major fraud case tied to crypto investment marketing. The Block reported that Christopher Alexander Delgado, the former CEO of Goliath Ventures, pleaded guilty to wire fraud, conspiracy to commit wire fraud, and money laundering in connection with an alleged $400 million scheme. Prosecutors said investors were lured with promises of high returns from crypto ‘liquidity pools,’ with at least $400 million collected and funds diverted to personal expenses, luxury travel, and an upscale lifestyle.

Delgado admitted causing at least $250 million in losses and agreed to forfeit assets including eight properties, 11 vehicles, 30 watches, more than 50 luxury handbags, and 29 pieces of jewelry, according to the report. He also faces substantial prison exposure: wire fraud charges can carry up to 20 years, while money laundering can carry up to 10 years under U.S. law.

Taken together, the developments capture a market in transition: large financial institutions are exploring stablecoins as mainstream settlement tools, regulators are forcing rapid compliance upgrades and market consolidation, and enforcement actions continue to target misconduct. The result is a crypto sector increasingly shaped by ‘regulatory perimeter’ dynamics—where access, liquidity, and credibility are progressively determined by licensing, supervision, and institutional-grade controls.

🔎 Market Interpretation

- Institutions are moving stablecoins from “crypto product” to “financial rail.” Reports of a consortium-led OUSD involving Visa/Mastercard/BlackRock/Coinbase (and cited involvement of AmEx) signal a strategy to embed fiat-linked tokens into payments, settlement, and exchange liquidity rather than treating them as speculative instruments.

- Regulation is becoming the primary market structure driver. EU MiCA taking effect accelerates a “comply or exit” moment that likely consolidates liquidity and user activity into licensed venues, reducing the footprint of offshore/high-risk platforms.

- Investor positioning is mixed: softer ETF flows, expanding product policy. US spot BTC ETFs saw heavy June outflows, suggesting near-term institutional risk appetite cooled, while the SEC simultaneously explores broader ETF constructs (virtual-asset funds, blockchain-linked opportunities, event contracts), indicating continued demand for regulated wrappers—even as standards tighten.

- Adoption narratives compete with risk headlines. Claims of sovereign BTC accumulation and corporate-holder selling pressure underscore how sentiment can pivot on unverified or partial information, especially during macro/regulatory shifts.

- Operational and legal risks remain elevated alongside mainstreaming. Bitcoin network-change caution, UK litigation against Binance, and a major US fraud guilty plea reinforce that “institutionalization” coexists with governance friction and enforcement actions.

💡 Strategic Points

- Stablecoin consortiums may be a compliance-and-distribution play. Pooling reserve management credibility (asset managers), network reach (payments rails), and exchange/onchain liquidity (crypto venues) can shorten go-to-market time—especially under tightening issuance and custody rules.

- Watch for OUSD design details that determine competitiveness:

- Issuer & domicile (which regulator, what license category)

- Reserve composition (cash, T-bills, repos) and attestation/audit cadence

- Redemption mechanics (T+0/T+1, fees, minimums) and who gets direct access

- Distribution surfaces (card settlement, merchant acquiring, remittances, exchange margin/liquidity)

- EU MiCA is likely to trigger rapid venue consolidation. If a large share of platforms cannot license in time, expect liquidity migration to regulated exchanges/custodians, fewer token listings, and more stringent onboarding/KYC—creating both compliance costs and competitive moats for approved players.

- ETF flows are a timing signal, not a final verdict. June outflows may reflect macro re-pricing and portfolio rotations; market participants should separate structural adoption (availability of regulated access) from cyclical demand (flows month-to-month).

- Policy expansion suggests “more products,” but with tighter constraints. SEC consultation on novel ETFs/event-contract-like exposures implies potential future approvals and/or clearer prohibitions; either outcome reduces ambiguity but can reshape which strategies are viable within regulated markets.

- Risk management priorities for participants:

- Counterparty risk: prefer licensed venues; verify segregation/custody arrangements

- Legal headline risk: derivatives marketing and retail targeting remain enforcement hotspots

- Protocol/operational risk: monitor network upgrade windows; consider settlement timing and confirmation policies during elevated reorg risk periods

- Be cautious with unverified market-moving claims. Statements about sovereign BTC buying or forced corporate selling can influence positioning, but without primary-source confirmation they should be treated as scenario inputs—not facts.

📘 Glossary

- Stablecoin: A token designed to track a fiat currency (typically USD) via reserves and redemption mechanisms.

- Crypto rails: Blockchain-based payment and settlement infrastructure used to move value and finalize transactions.

- Consortium stablecoin: A stablecoin launched/managed jointly by multiple firms to combine compliance, reserves, and distribution.

- MiCA (Markets in Crypto-Assets): EU-wide regulatory framework covering crypto-asset issuance and service providers, requiring licensing and compliance.

- CASP (Crypto-Asset Service Provider): An entity providing crypto services (exchange, custody, brokerage, etc.) subject to licensing under frameworks like MiCA.

- Spot Bitcoin ETF: An exchange-traded fund that holds Bitcoin directly, offering regulated exposure through traditional brokerage accounts.

- Net outflows: When redemptions/sales exceed new purchases/creations for an ETF over a period.

- Event contracts: Instruments whose payoff depends on whether a specific event occurs; can resemble derivatives.

- Chain reorganization (reorg): A situation where the blockchain replaces recent blocks with an alternative chain, potentially reversing recent transactions.

- Bitcoin Core / Knots: Two implementations/clients for running a Bitcoin full node; differences can reflect policy and governance preferences.

- Derivatives (crypto): Leveraged products (futures, options, perps) whose value is derived from an underlying asset like BTC; heavily regulated for retail access in many jurisdictions.

- Wire fraud / money laundering: US criminal offenses often used in prosecuting investment scams involving interstate communications and illicit fund flows.

- Regulatory perimeter: The boundary of activities/entities subject to formal supervision; being “inside” typically affects access, credibility, and liquidity.

Comment 0