News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

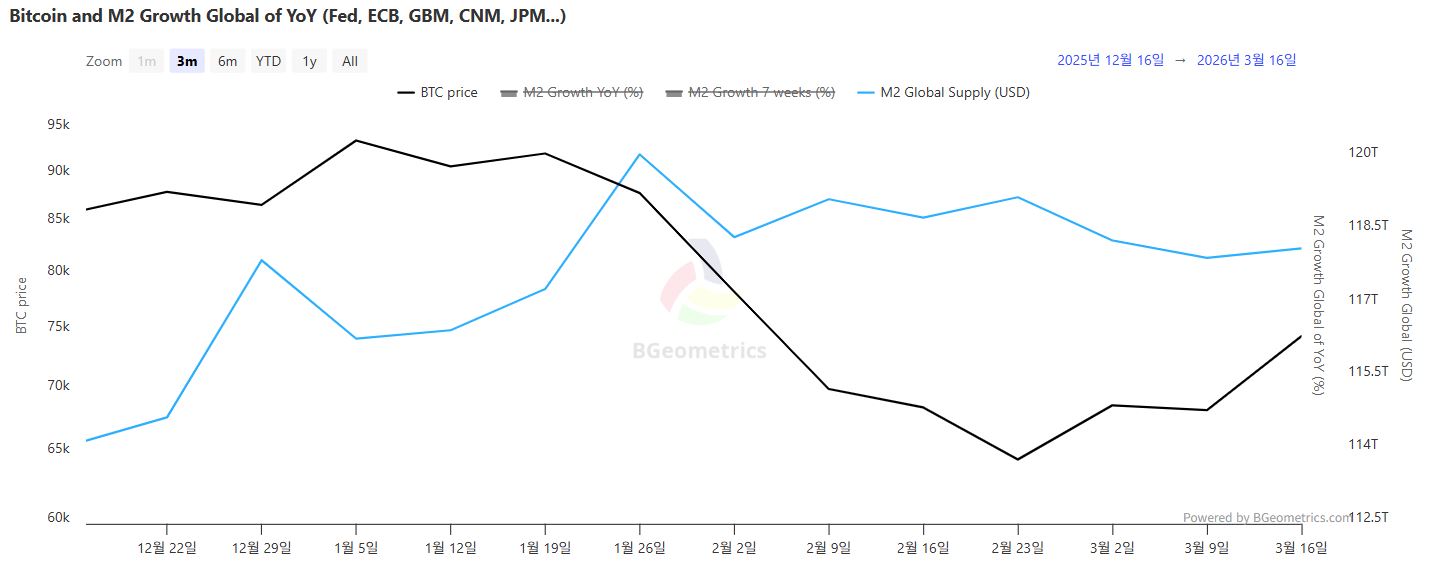

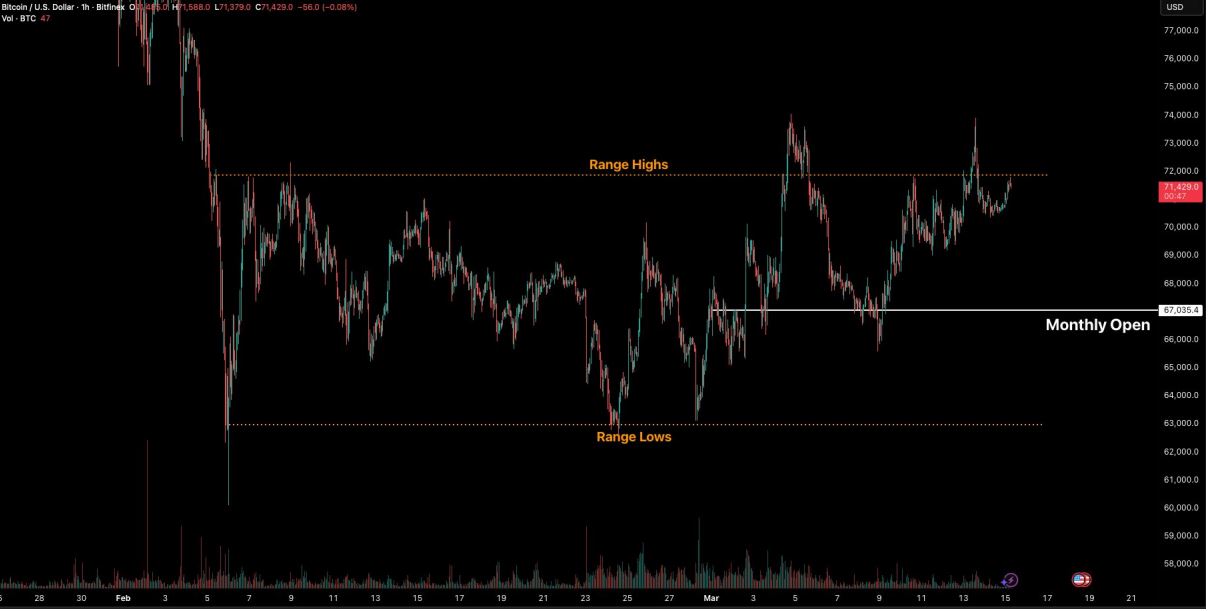

The U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission have jointly issued finalized interpretive guidance on when crypto assets are securities—formally classifying Bitcoin (BTC) and Ethereum (ETH) as 'digital commodities' and aiming to close a decade-long chapter of regulatory ambiguity.

The announcement, delivered Tuesday UTC alongside industry remarks attributed to SEC Chair Paul Atkins at the Digital Chamber’s Blockchain Summit 2026, lays out a unified federal framework intended to reduce compliance whiplash for exchanges, issuers, and institutional investors operating across U.S. markets.

At the center of the policy is a five-part taxonomy that separates crypto assets by their primary function and the presence—or absence—of reliance on an issuer’s 'essential managerial efforts,' a concept tied to the long-running investment-contract analysis under U.S. securities law.

First, the agencies designate a 'Digital Commodity' bucket covering widely traded networks whose value is deemed to arise mainly from programmed blockchain operation and market supply-demand rather than from a promoter’s ongoing business execution.

In that category, the guidance explicitly lists a group of major tokens—including Bitcoin (BTC), Ethereum (ETH), Solana (SOL), XRP (XRP), Dogecoin (DOGE), Cardano (ADA), Chainlink (LINK), Polkadot (DOT), Stellar (XLM), and Tezos (XTZ)—as non-securities, a clarification likely to be closely watched by U.S. spot markets and derivatives venues alike.

Second, the SEC framework identifies 'Digital Collectibles'—a broad umbrella for NFTs such as CryptoPunks and other culturally or entertainment-driven tokens—arguing these instruments generally represent consumptive or expressive value rather than a securities-style claim on an enterprise.

Third, it defines 'Digital Tools' as tokens or token-like rights used for practical functions such as identity, access, membership, or ticketing, citing examples like Ethereum Name Service (ENS) domains and NFT-based event tickets, and stating these assets are generally not securities when used primarily as utilities.

Fourth, the guidance addresses dollar-pegged tokens as 'Payment stablecoins' and points to the GENIUS Act enacted in 2025, under which stablecoins issued by authorized payment-stablecoin issuers are excluded from securities treatment under the specified conditions.

Fifth, it draws a bright line around 'Digital Securities,' defined as tokenized versions of traditional financial instruments such as stocks and bonds, which remain subject to the existing securities regime—an approach that implicitly encourages compliant tokenization while warning against relabeling conventional products as crypto to evade oversight.

Beyond classification, the agencies also tackled some of the market’s most litigated questions by stating that common network activities—protocol mining, protocol staking, and certain airdrops—do not, by themselves, constitute securities transactions when they lack the core features of an investment contract.

For proof-of-work networks, solo mining and participation in mining pools are described as operational contributions to network security rather than investments made in expectation of profits driven by a third party’s managerial work, signaling a more standardized compliance posture for infrastructure participants.

For proof-of-stake networks, the guidance extends the same logic to solo staking, delegated staking, custodial staking, and liquid staking, and further notes that mechanics such as slashing-related rewards, early unbonding, alternative reward payments, and pooling arrangements do not automatically trigger securities-law treatment.

Airdrops also receive explicit treatment: where recipients provide no consideration and receive a non-security crypto asset, the distribution is framed as failing the 'investment of money' element of the Howey analysis, reducing risk for certain network-launch and community distribution models while still leaving room for enforcement if promotional promises dominate the facts.

The agencies added that 'wrapping'—issuing a 1:1 token backed by a non-security crypto asset—does not transform the underlying exposure into a security, an important detail for cross-chain liquidity and collateral design used throughout decentralized finance.

Still, regulators cautioned that even a token categorized as a non-security can be sold as part of an investment contract if an issuer makes promises that lead buyers to reasonably expect profits from that issuer’s 'essential managerial efforts,' effectively separating the nature of the token from the nature of the offering.

In a notable nuance, the guidance suggests an investment-contract relationship can extinguish if the issuer fulfills those commitments or explicitly renounces them, and that secondary-market trading may fall outside securities laws where it is reasonable to conclude that the original promises no longer attach to the asset.

Market participants interpreted the move as a potential catalyst for 'institutional demand' by narrowing the gray zone that has historically constrained broker-dealers, custodians, and asset managers, even as firms will still need to document facts-and-circumstances around marketing, disclosures, and post-launch conduct.

The finalized rules may also reverberate beyond the U.S., particularly in South Korea, where exchange listing decisions and staking-service policies have been sensitive to U.S. enforcement signals; clearer non-security status for large-cap assets such as XRP (XRP), Solana (SOL), Cardano (ADA), and Chainlink (LINK) could reduce perceived cross-border compliance risk.

South Korea’s ongoing debate over follow-on digital-asset legislation—often described as a second-stage framework to complement the Virtual Asset User Protection Act—could also draw on the U.S. emphasis on issuer promises and sales practices when crafting standards for tokenized securities and borderline offerings.

Traders will be watching whether higher regulatory certainty accelerates global capital flows into crypto markets, a dynamic that can influence local pricing dislocations such as the 'Kimchi premium' during periods of rapid inflow or constrained arbitrage.

The guidance takes effect upon publication in the Federal Register, according to the agencies, and the SEC said it will continue to solicit market feedback and refine interpretive benchmarks—setting the stage for a more predictable compliance environment while keeping enforcement tools available for offerings built on profit-promising promotion.

Comment 0