News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

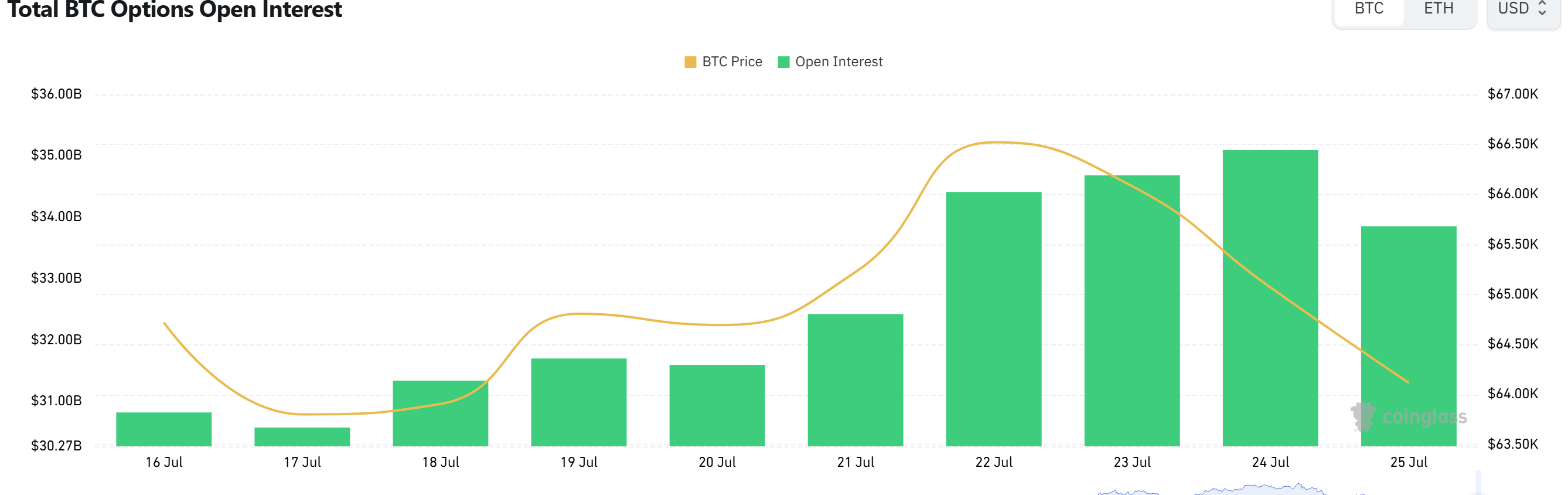

Bitcoin (BTC) options positioning showed a notable shift over the past day, with open interest rising above $30 billion and traders concentrating activity in a high-strike $380,000 call expiring in late June—an unusual focal point that underscores how speculative upside bets can coexist with short-term hedging demand.

Data compiled by CoinGlass at 12:00 a.m. ET on Apr. 6 showed total BTC options open interest (OI) at $30.63 billion, up about 3.1% from $29.71 billion a day earlier. The OI mix remained tilted toward calls—typically associated with bullish positioning—at 56.71%, versus 43.29% for puts.

Trading activity, however, told a more nuanced story. BTC options volume over the past 24 hours was about $1.45 billion, with puts accounting for 53.41% and calls 46.59%. The split suggests that while the broader outstanding positioning still reflects a call-heavy structure, more recent flows leaned defensive—consistent with short-term protection buying or volatility trades rather than outright directional conviction.

By venue, Deribit led dollar-denominated volume at roughly $809 million, followed by Bybit at $392 million, OKX at $255 million, CME at $241 million, and Binance at $243 million. The exchange mix highlights Deribit’s continued dominance in crypto-native options liquidity, while CME’s substantial share reflects ongoing participation from more traditional, regulated-market players.

The largest OI concentrations were clustered in longer-dated and widely watched strikes on Deribit, led by a $120,000 call expiring Dec. 25, a $60,000 put also expiring Dec. 25, and an $80,000 call expiring May 29. Such “sticky” OI levels are often interpreted as higher-conviction positioning or structured hedges that accumulate over time rather than purely tactical trades.

In contrast, the most actively traded contracts over the last day were more tactical and event-sensitive. The top contract by 24-hour volume was a $380,000 call expiring June 26 on Deribit—followed by a $67,000 put expiring Apr. 24 on Deribit and a $68,500 call expiring Apr. 6 on Bybit. The prominence of an extreme out-of-the-money June call can reflect low-premium ‘lottery ticket’ positioning, volatility plays, or structured strategies that use far-upside calls as overlays—rather than a straightforward forecast that BTC will reach that level by expiry.

Options are derivatives that can be used to gain leveraged exposure to price moves or to hedge existing holdings. A ‘call option’ generally expresses upside exposure, while a ‘put option’ is commonly used to position for downside or to protect against losses. OI measures the number of outstanding contracts and is often watched as a proxy for accumulated positioning and medium-term risk appetite. When OI rises while short-term volume skews toward puts, it can indicate that fresh positioning is being built even as traders simultaneously pay for near-term protection—signaling a market that remains engaged but cautious about short-term drawdowns.

🔎 Market Interpretation

- Open interest expands, risk engagement rises: Total BTC options OI increased to $30.63B (+3.1% day/day), indicating new/added positioning rather than a market in retreat.

- Positioning remains structurally bullish, but flows turned defensive: The outstanding OI is still call-heavy (56.71% calls), yet 24h trading volume leaned to puts (53.41%)—a common pattern when traders add hedges or trade short-term volatility while maintaining longer-term upside exposure.

- Speculative tail bets gained attention: The most traded contract was an extreme $380,000 June 26 call on Deribit, suggesting “lottery ticket” upside positioning, volatility/convexity overlays, or structured strategies—not necessarily a literal price forecast.

- Key strikes signal where markets anchor expectations: Largest OI clusters on Deribit were concentrated in widely watched, longer-dated strikes (e.g., $120k call Dec 25, $60k put Dec 25, $80k call May 29), often interpreted as more persistent hedging/positioning levels.

- Liquidity remains crypto-native, with a growing traditional footprint: Deribit led volume (~$809M), while CME participation (~$241M) underscores continued engagement from regulated-market traders alongside crypto venues.

💡 Strategic Points

- Read the divergence correctly (OI vs. volume): Rising OI with put-skewed short-term volume often points to new risk being added with near-term protection, rather than a simple bearish shift.

- Differentiate “sticky” OI from tactical volume: Large, longer-dated OI concentrations can reflect structured hedges or longer-horizon views, while the day’s most active trades (e.g., near-term puts/calls) are more event- and volatility-sensitive.

- Extreme OTM calls can be portfolio overlays: Far-upside calls may be used as low-premium convexity (small cost, large payoff in tail scenarios) or as part of spreads/structured products; interpret them alongside put flows and term structure rather than in isolation.

- Monitor strike clustering for “magnet” levels: High OI at prominent strikes (e.g., $60k put, $80k/$120k calls) can influence dealer hedging dynamics and market attention as expiries approach.

- Venue mix can hint at participant type: Deribit dominance suggests crypto-native activity, while CME share can imply institutional hedging, basis/vol trades, or macro-driven positioning.

📘 Glossary

- Option: A derivative contract giving the right (not obligation) to buy/sell an asset at a preset price by a set date.

- Call option: Benefits from price upside; right to buy at the strike price.

- Put option: Benefits from price downside/protection; right to sell at the strike price.

- Strike price: The price level at which the option can be exercised.

- Expiration: The date the option contract ends (e.g., Apr. 24, May 29, Jun. 26, Dec. 25).

- Open interest (OI): Number of outstanding option contracts; a proxy for accumulated positioning and market engagement.

- Options volume: Contracts traded over a period (e.g., 24h); reflects current flow and near-term sentiment/hedging.

- Out-of-the-money (OTM): An option with a strike far from the current spot price; typically cheaper and more speculative.

- Hedging: Using derivatives (often puts) to reduce downside risk of an underlying position.

- Volatility trade: Strategy aiming to profit from changes in implied/realized volatility rather than pure direction.

Comment 0