News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Bitcoin’s long-running narrative as ‘digital gold’ is colliding with a harsher reality: when geopolitical stress hits, investors still run to traditional havens, while crypto behaves more like a risk asset—and the parts of the crypto stack that do see crisis-driven demand are often ‘dollar-linked stablecoins’, not Bitcoin (BTC).

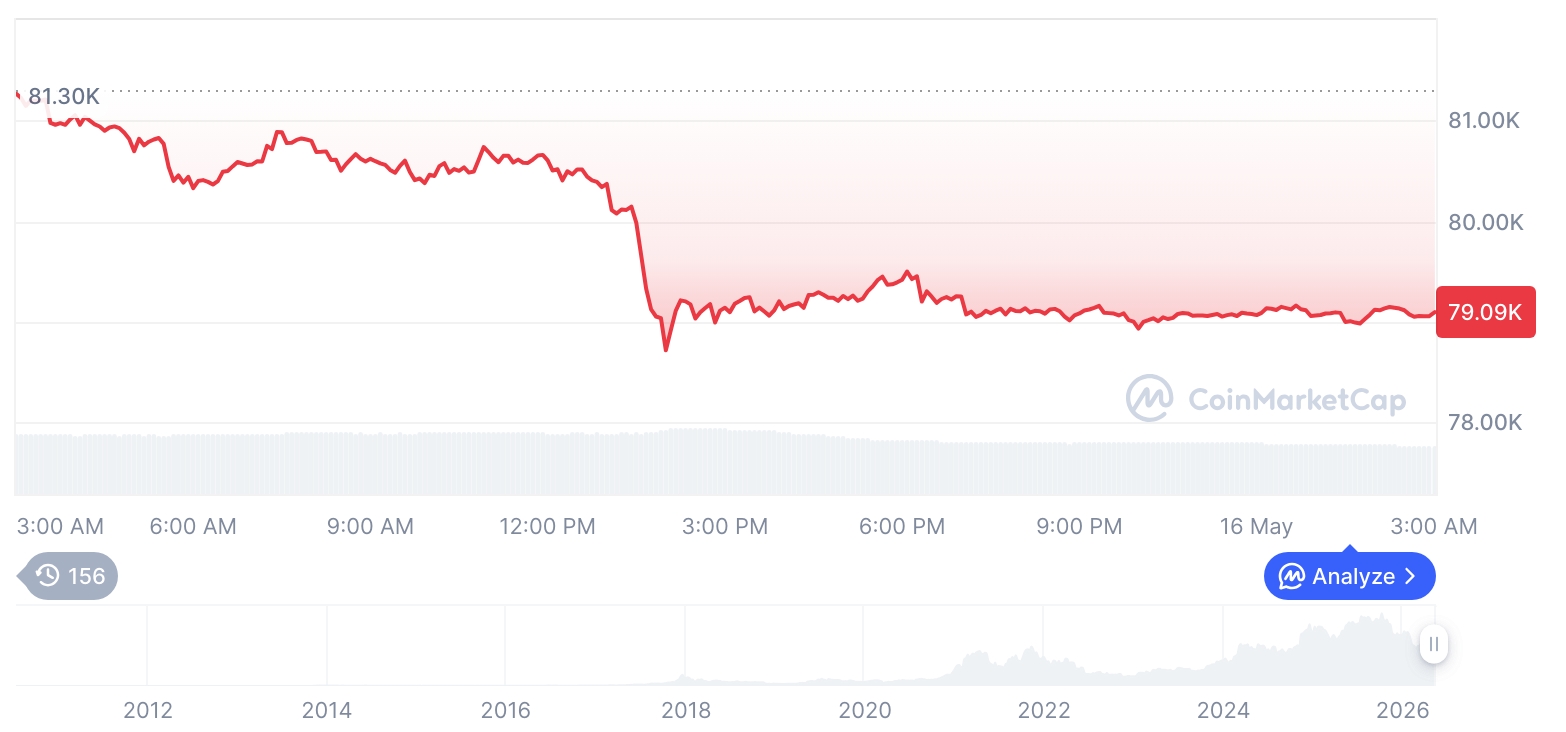

The shift became difficult to ignore after the Feb. 28 strike on Iran by the U.S. and Israel, a major geopolitical shock that arrived after ‘institutional participation’ in digital assets had become mainstream. Over the past year, gold rose 64% while Bitcoin fell 5%, undermining the idea that BTC reliably functions as a wartime hedge.

That divergence, the column argues, is not a sudden failure of crypto—but a delayed recognition that how an asset is marketed in white papers and conference stages can differ sharply from how it is traded under fear and uncertainty.

One shock, two faces of crypto

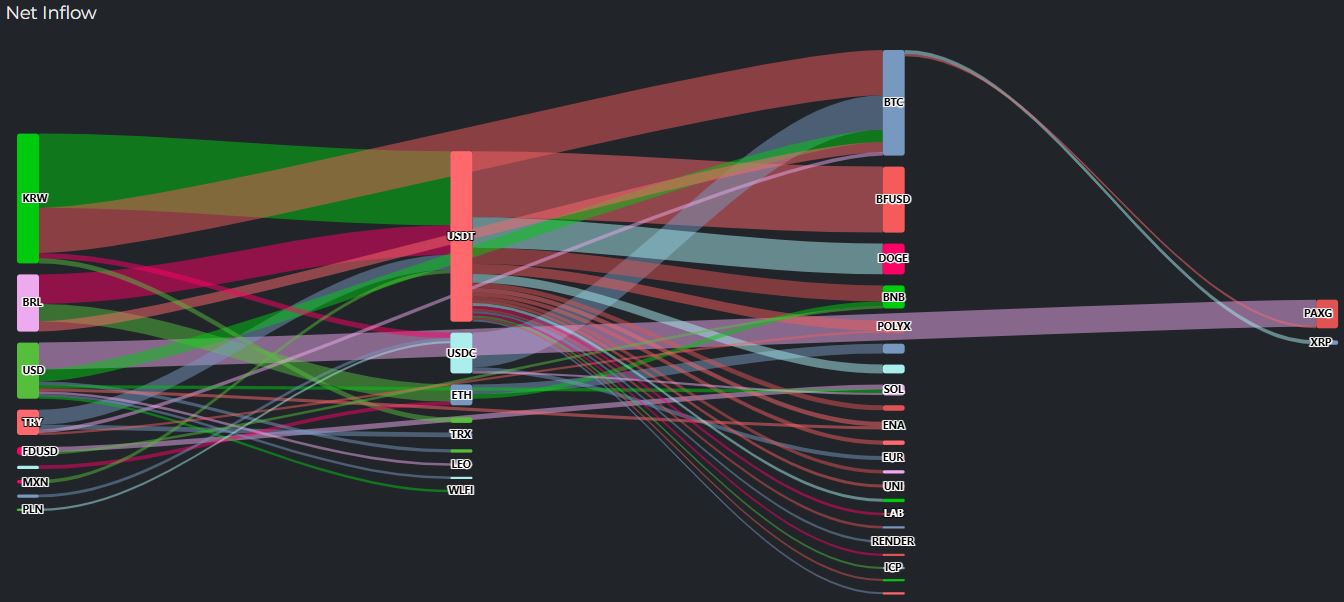

In the 48 hours after the strikes, roughly $10 million reportedly flowed out of Iranian exchanges. The more important question, however, was not the outflow itself but the destination.

According to the commentary, entities linked to Iran’s Revolutionary Guard were not leaning on Bitcoin for procurement and oil settlement. Instead, they favored ‘stablecoins’ pegged to the U.S. dollar—tools that can move value across borders while circumventing chokepoints in the traditional correspondent banking system, including SWIFT.

At the same time, Iranian citizens confronting inflation near 50% reportedly converted savings into Bitcoin, drawn by properties that can matter under authoritarian pressure: assets that are harder to seize, freeze, or deplatform. When authorities severely restricted internet access—cutting it by as much as 99%, the column claims—retail users’ access to exchanges deteriorated, while sophisticated wallets continued operating.

The episode highlighted crypto’s dual-use nature: the same rails can be a last-resort escape valve for individuals and a sanctions-evasion channel for state-linked actors. The industry, the author contends, has too often sheltered behind the claim that ‘technology is neutral’, ignoring how outcomes change depending on who holds the tool.

Institutions are playing a different game

While retail participants debate Bitcoin’s identity, institutional allocators appear to be treating BTC less as an anti-establishment symbol and more as an investable ‘asset class’—one that belongs in portfolios for diversification, liquidity access, and product demand rather than for war hedging.

The piece points to $18.7 billion in net inflows to Bitcoin ETFs in Q1 2026, alongside the rapid scale-up of BlackRock’s spot Bitcoin ETF with assets above $54 billion—levels that, in the author’s framing, resemble sovereign-scale pools just 18 months after launch. That institutional embrace is presented as both a victory and a myth-ender: Wall Street’s Bitcoin is not a revolutionary banner, but a fee-generating financial product.

Where the real transformation is happening: payments

The column argues that the deeper structural change is unfolding in payment networks, where stablecoins are increasingly positioned as a programmable settlement layer.

It cites Japan’s SBI Holdings selecting Solana (SOL) as a primary payment network for institutional operations—a notable decision given the availability of Ethereum (ETH) and private, permissioned alternatives. Solana, the commentary notes, processed $650 billion in stablecoin transactions in February alone, underscoring the scale at which public chains are now competing on throughput and cost.

Meanwhile, PayPal ($PYPL) has said it plans to expand its stablecoin to 70 countries, and Tether has introduced a wallet aimed at a user base in the hundreds of millions. The author frames these moves not as isolated crypto product launches, but as payment companies rebuilding global settlement plumbing around stablecoins.

The economic incentive is straightforward: traditional cross-border bank transfers can take three to five days and cost 6–8% in fees, while stablecoin settlement can occur in fractions of a second at near-zero cost. When the cost-speed gap becomes that wide, markets typically migrate toward the cheaper, faster rail—an industrial-era rule that still holds, the column argues.

After the hack, capital moved toward ‘regulated’ gravity

The author also points to a separate stress test: an April 1 exploit of Solana-based DeFi protocol Drift, where $285 million was allegedly stolen, with suspicion falling on North Korean hackers. Yet the key signal, the column argues, was what happened next.

Rather than returning to experimental DeFi, capital purportedly rotated toward ‘institutional-grade infrastructure’: regulated exchanges such as Kraken, Strategy (the company formerly known as MicroStrategy) with its large Bitcoin holdings, and the tokenized U.S. Treasury market—an on-chain segment the piece says grew 120% over the past year.

The pattern reflects an uncomfortable reality for decentralization maximalists: when large sums are at stake, markets increasingly prefer licensing, audits, and governance clarity over ideology. In that sense, recent regulatory trajectories—U.S. stablecoin and market-structure efforts, Europe’s MiCA framework, and updates across Singapore, Hong Kong, the UAE, and Japan—are converging on similar requirements: ‘100% reserves’, comprehensive audits, and AML obligations.

The implication is that market access is no longer determined by engineering alone. It is increasingly determined by compliance capacity.

Is South Korea ready?

Against that global backdrop, the column asks where South Korea stands. It argues the country has world-class consumer payment infrastructure—pointing to platforms such as Toss and KakaoPay—and notes that the Bank of Korea is advancing its deposit-token initiative through the next stage of ‘Project Hangang’. The government has also signaled ambitions to use deposit tokens for a portion of its budget execution by 2030.

But on the private-sector digital asset side, the author warns of policy drift. The Digital Asset Basic Act remains stalled, and South Korea lacks a clear legal foundation for issuing a won-denominated stablecoin. Meanwhile, other jurisdictions are moving: the U.S. Congress has advanced a market-structure bill often referred to as the ‘CLARITY’ Act, Japan is already experimenting with local-currency stablecoins, and Singapore’s DBS has entrenched itself as a regional hub for regulated digital asset infrastructure.

The opportunity: RWA and a won stablecoin

The column’s constructive thesis is that South Korea still has a window—if it acts quickly. Tokenized real-world assets (RWA) grew to $24 billion last year, up 266%, as real estate, private credit, corporate bonds, and U.S. Treasuries move on-chain. The potential addressable base of tokenizable assets, the author argues, exceeds $100 trillion.

South Korea, the piece adds, has unique candidates beyond conventional finance: K-content intellectual property, K-pop music royalties, and webtoon IP—assets with demonstrated global demand. But to monetize and distribute them at scale, the ecosystem needs reliable settlement and compliant distribution rails. A ‘won stablecoin’ could serve as the payment instrument, while regulated RWA platforms could provide issuance and secondary-market infrastructure.

Still, the author stresses that the winning formula is not deregulated experimentation. Global capital is increasingly choosing environments that are credible: clear rules, verifiable reserves, independent audits, and unambiguous accountability. The market’s questions have become blunt: “Is it legal? Is it audited? Who is responsible when something breaks?” Systems that cannot answer risk being bypassed.

Bitcoin isn’t gold—but it isn’t useless

The column closes by reframing Bitcoin’s value proposition. BTC may not trade like gold during war scares, but that does not make it a failed asset. It remains a scarce, 24/7-traded digital commodity with relatively low counterparty risk and minimal custody costs—traits that can justify its role in portfolios without relying on exaggerated labels.

Stablecoins’ rise, the author argues, is similarly pragmatic rather than ideological. They solve an operational problem: how to move $10 million across borders in seconds, with final settlement and limited FX risk—provided the system is lawful, licensed, and auditable.

In that light, the Iran shock did not “break” digital assets. It clarified what this market is becoming: less a geopolitical hedge or a replacement for central banks, and more a ‘programmable payment infrastructure’—financial plumbing that moves capital faster and cheaper.

For South Korea, the choice is presented as urgent: build compliant rails for won stablecoins and RWA now, or import rules and infrastructure built elsewhere later. The next 18 months, the piece argues, are likely to be decisive as capital concentrates in licensed venues, payments migrate toward stablecoins, and real-world assets continue moving on-chain.

🔎 Market Interpretation

- “Digital gold” stress test failed: After a major geopolitical shock (Feb. 28 U.S./Israel strike on Iran), market behavior reinforced that gold remains the dominant crisis hedge while Bitcoin trades more like a risk asset. Over the past year cited: gold +64% vs BTC -5%.

- Crisis demand concentrates in stablecoins, not BTC: The most scalable “flight to utility” inside crypto during geopolitical stress appears to be USD-pegged stablecoins, which combine fast cross-border transfer with lower friction than bank rails and can bypass legacy chokepoints.

- Crypto shows two simultaneous crisis use-cases:

- Individuals: Under high inflation and political constraints, some citizens reportedly turn to BTC for seizure resistance/censorship resistance.

- State-linked/illicit actors: The same rails can facilitate sanctions evasion, with stablecoins favored for settlement-like functionality.

- Institutionalization changes BTC’s “why”: With $18.7B net inflows to Bitcoin ETFs in Q1 2026 and a spot BTC ETF exceeding $54B AUM, Bitcoin is increasingly treated as a liquid investable product (diversification, access, fees) rather than an anti-system hedge narrative.

- Payments are the center of gravity: Stablecoins are framed as programmable settlement infrastructure competing directly with correspondent banking—driven by dramatic speed/cost differences (bank transfers 3–5 days and 6–8% vs near-instant/near-zero settlement).

- After DeFi shocks, capital migrates “up the compliance stack”: Following an alleged $285M exploit tied to North Korean actors, the article argues funds rotated toward regulated exchanges, large “institutional-grade” vehicles, and tokenized U.S. Treasuries (said to be +120% YoY), signaling preference for licensing, audits, and clear accountability.

- Regulation is converging globally: Across the U.S. (stablecoin and market-structure efforts), EU MiCA, and Asian hubs (Singapore/HK/UAE/Japan), common denominators are emerging: 100% reserves, audits, and AML—making compliance capacity a decisive competitive advantage.

- South Korea’s strategic window: Despite strong domestic payments and central bank deposit-token pilots, legal uncertainty (e.g., stalled Digital Asset Basic Act; no clear won-stablecoin basis) risks Korea importing standards and infrastructure later rather than shaping them now.

💡 Strategic Points

- Reposition BTC realistically in portfolios: Treat Bitcoin as a scarce, 24/7-traded digital commodity with low counterparty risk and low custody overhead—not as a reliable “war hedge.” This framing aligns better with actual crisis-period correlations and investor behavior.

- Stablecoins are the near-term product-market fit: The article’s core claim is that infrastructure value accrues to the parties that enable lawful, auditable stablecoin settlement at scale—wallets, issuers, exchanges, payment processors, and compliance tooling.

- Public chains are competing on throughput/cost: Japan’s SBI selecting Solana for institutional payment use (despite Ethereum and permissioned options) and the cited $650B stablecoin transaction volume in one month are used to argue that chain selection will be driven by performance, reliability, and cost—not ideology.

- “Regulated gravity” thesis for capital allocation: After exploits and geopolitical episodes, the piece suggests capital prefers venues that can answer: Is it legal? Is it audited? Who is accountable? Market structure is trending toward licensed intermediaries + transparent reserves + governance clarity.

- South Korea: combine a won stablecoin with RWA rails:

- Opportunity set: Tokenized RWA cited at $24B (+266%) with a potential tokenizable base > $100T.

- Differentiators: Beyond typical financial RWAs, Korea can tokenize K-content IP, K-pop royalties, and webtoon IP—but needs compliant issuance, custody, disclosure, and secondary-market rules.

- Settlement requirement: A won-denominated stablecoin (or regulated deposit token) functions as the domestic settlement instrument, reducing FX friction and enabling programmable payments for IP/RWA distribution.

- Policy actions implied by the column:

- Create a clear legal basis for won stablecoin issuance (reserve standards, redemption rights, supervision).

- Standardize proof of reserves, independent audits, and AML/KYC obligations to meet global interoperability expectations.

- Enable regulated RWA marketplaces with disclosure, custody, and investor-protection requirements.

- Coordinate deposit-token initiatives (e.g., Project Hangang) with private-sector stablecoin/RWA development to avoid fragmented rails.

- Time horizon emphasis: The next ~18 months are framed as pivotal as payments migrate to stablecoins, RWAs expand on-chain, and liquidity concentrates in compliant venues.

📘 Glossary

- Bitcoin (BTC): A decentralized digital asset with a fixed supply schedule; trades continuously and is often framed as a commodity-like asset.

- Digital gold narrative: The thesis that BTC behaves like gold—especially as a crisis hedge—an idea challenged here by observed wartime/geopolitical correlations.

- Stablecoin: A token designed to maintain a stable value (commonly 1:1 to the U.S. dollar) used for trading, settlement, and payments.

- USD-pegged / dollar-linked stablecoin: Stablecoins redeemable (in principle) for dollars or dollar-equivalent assets; widely used as a cross-border settlement proxy.

- SWIFT / correspondent banking: Legacy messaging and banking networks enabling cross-border transfers, often slower and more expensive with multiple intermediaries.

- ETF (Exchange-Traded Fund): A regulated product that trades on exchanges and provides exposure to an underlying asset (here, spot Bitcoin) without direct self-custody.

- Spot Bitcoin ETF: An ETF backed by actual Bitcoin holdings (not futures), enabling institutional and retail access via brokerage accounts.

- DeFi (Decentralized Finance): On-chain financial applications (trading, lending, derivatives) executed via smart contracts rather than traditional intermediaries.

- Exploit / hack: Theft or loss caused by vulnerabilities in smart contracts, infrastructure, or operational security; often triggers “risk-off” rotation.

- Tokenized U.S. Treasuries: On-chain representations of Treasury exposures used as collateral/settlement assets; often positioned as a regulated, yield-bearing “safe” on-chain instrument.

- MiCA: The EU’s Markets in Crypto-Assets regulation—framework covering issuance, disclosure, and service providers, including stablecoin requirements.

- AML (Anti-Money Laundering): Compliance controls to detect/prevent illicit financial activity (KYC, transaction monitoring, reporting).

- RWA (Real-World Assets): Tokenized claims on off-chain assets such as bonds, credit, real estate, or IP royalties, enabling on-chain issuance and transfer.

- Deposit token: A tokenized form of bank deposits (typically redeemable at par), often explored as a regulated alternative to privately issued stablecoins.

- Programmable settlement: Payments that can be automated with rules (smart contracts), enabling conditional transfers, instant reconciliation, and composable workflows.

Comment 0