News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

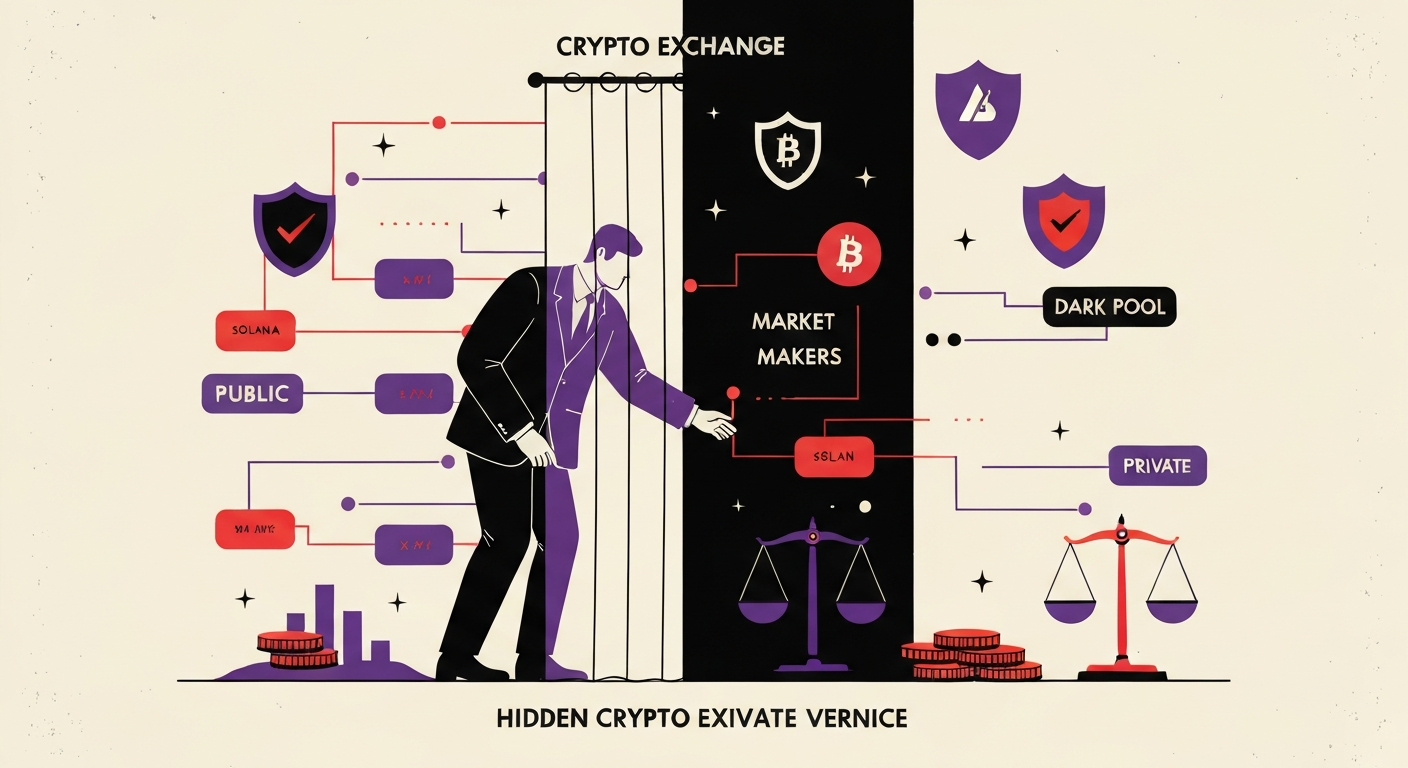

Crypto markets have long marketed ‘radical transparency’ as a feature, but for large traders and market makers it is increasingly becoming a structural handicap—one that can leak strategy, amplify price impact, and turn routine liquidity provision into a public spectacle. A new experiment aiming to bring ‘dark pool’-style execution on-chain is set to test how far the industry is willing to bend its transparency ethos in pursuit of institutional-grade trading.

Unlike traditional equities—where a large share of flow can be executed away from public order books—decentralized finance (DeFi) remains overwhelmingly observable by design. Orders, fills, and wallet movements on decentralized exchanges (DEXs) are recorded on-chain and can be tracked in near real time, then repackaged by analytics platforms such as DeFiLlama and Arkham. In practice, trades on venues like Hyperliquid are often as traceable as a public ledger can be.

That visibility carries a cost for the biggest liquidity providers. When a sufficiently large participant enters or exits a position, other traders can quickly detect the footprint and attempt to mirror or counter the strategy, eroding ‘alpha’ and increasing execution risk. Denis Dariotis, co-founder of trading firm GoQuant, described the dynamic as an “alpha problem,” arguing that on Hyperliquid major market makers may need to rotate strategies as frequently as every three weeks to avoid being copied.

The issue extends beyond strategy leakage. In crypto, the same transparency that supports auditability can also fuel narrative risk. When on-chain sleuthing converges on a recognizable firm, normal trading activity can be recast as market manipulation or blamed for broader market events—creating reputational exposure that traditional market makers rarely face to the same degree. In conventional finance, large blocks are often handled via ‘dark pools’ and off-exchange venues with post-trade reporting and regulatory oversight, limiting pre-trade signaling while preserving supervisory visibility.

GoQuant is now attempting to import a version of that model to DeFi. The firm plans to launch a Solana (SOL)-based DEX called ‘GoDark’ in May, positioning it as a privacy-first execution venue for professional traders. The core tooling relies on ‘zero-knowledge proofs (ZKPs),’ cryptographic methods that can validate transactions without revealing sensitive details. According to the project’s design goals, not only trade details but even the order-matching process would be obscured from outside observers—and potentially from node operators as well.

Yet the trade-offs are immediate. Speed remains a decisive factor for market makers, and GoDark’s reported test performance—around 25 to 50 milliseconds for matching—may be fast by DEX standards but still behind the latency profile of centralized exchanges, where high-frequency firms compete on razor-thin timing advantages. For retail users, this gap may be negligible; for professional liquidity providers, it can determine whether a venue is viable.

Liquidity is the second—and arguably bigger—challenge. GoDark plans to pool user capital into a market-making structure reminiscent of Hyperliquid’s HLP vault, distributing fees back to participants. The model has precedent across DeFi, but it also has a recurring weakness: volumes can evaporate once incentives taper off. Several DEXs that relied heavily on token rewards have seen activity fall sharply after promotional programs ended, raising doubts about whether privacy alone can sustain durable order flow.

Regulation may be the hardest constraint. Traditional dark pools do not publish pre-trade information but are subject to post-trade reporting and ongoing surveillance. A ZKP-based venue designed to minimize the availability of transaction records could collide with a regulatory environment that has increasingly emphasized ‘transparency’ in crypto markets. GoDark is reportedly planning automated screening aligned with the U.S. Treasury’s Office of Foreign Assets Control (OFAC), but that may not fully address broader supervisory expectations around auditability and market integrity.

Ultimately, the market’s verdict will hinge on two questions: whether GoDark can attract enough liquidity to be useful to the very institutions it is built for, and whether regulators will tolerate a ‘blind’ execution venue on a public blockchain. If successful, privacy-centric DEXs could become a key layer of infrastructure for institutional participation in DeFi. If not, the episode may reinforce the industry’s prevailing direction—toward more observable, compliance-friendly market structure rather than less.

Comment 0