News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

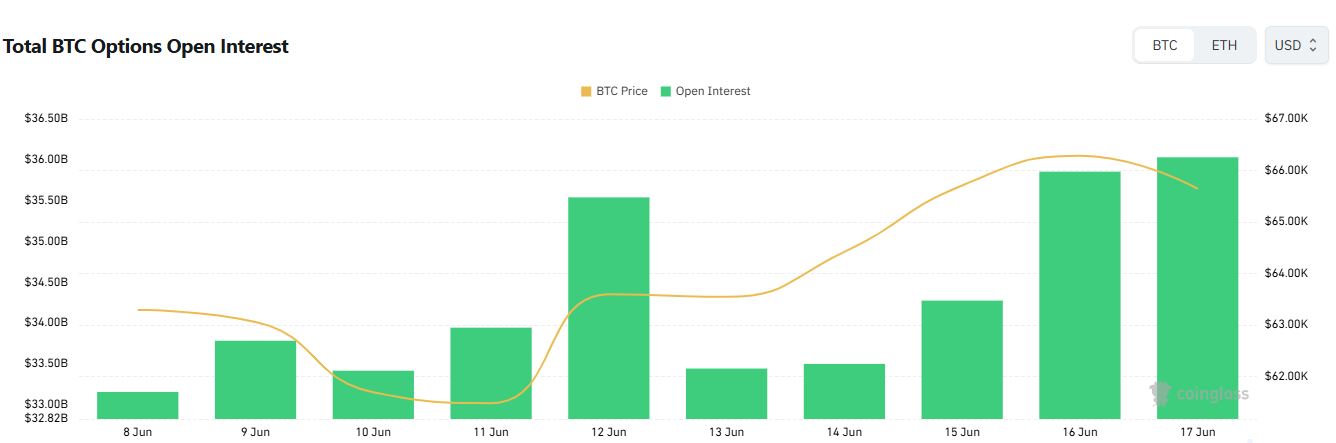

Bitcoin (BTC) options open interest climbed above $36 billion on Tuesday, underscoring sustained derivatives participation even as traders split their attention between aggressive upside bets and near-term downside protection.

According to CoinGlass data as of Tuesday 00:00 UTC, total BTC options 'open interest' (OI) reached $36.03 billion, up about 0.5% from $35.85 billion a day earlier. Calls continued to dominate positioning, accounting for 58.98% of OI versus 41.02% for puts—an overall structure that suggests traders are still leaning bullish in medium-dated exposure.

Trading activity, however, looked more balanced. Total BTC options volume over the past 24 hours was roughly $2.86 billion, with calls representing 51.82% and puts 48.18%. Market participants often interpret that kind of split as a sign that while longer-horizon positioning remains tilted toward upside, short-term flows include meaningful demand for hedges and volatility plays.

Deribit remained the primary venue, posting about $1.48 billion in volume. By venue, CoinGlass recorded approximately $630 million on Bybit, $373 million on Binance, $316 million on OKX, and $64 million on CME.

Positioning was heavily concentrated at a handful of large strikes and expiries. The biggest OI clusters were led by a $120,000 call expiring Dec. 25 on Deribit, followed by an $80,000 call expiring July 31, and a $60,000 put expiring June 26—an arrangement that combines far-out 'tails' on the upside with protection closer to current spot levels.

On a 24-hour volume basis, the most actively traded contract was the $63,000 put expiring June 19 on Deribit, suggesting heightened interest in near-term downside insurance around that level. Next were the $72,000 call expiring July 31 and the $65,000 put expiring June 26, both also on Deribit.

In options markets, calls grant the right—but not the obligation—to buy an asset at a preset price, while puts grant the right to sell. OI reflects the total number of outstanding contracts and is commonly used to gauge the market’s accumulated positioning. Rising OI typically indicates fresh capital entering longer-lived trades, while a near-even split in daily call and put activity can point to simultaneous risk-taking and hedging—an important backdrop as BTC traders brace for potential volatility around upcoming expiries.

🔎 Market Interpretation

- Derivatives participation remains elevated: BTC options open interest (OI) rose to $36.03B (+0.5% day/day), signaling sustained capital committed to options positioning.

- Medium-term stance skews bullish: Calls account for 58.98% of total OI vs 41.02% puts, implying traders are structurally positioned for upside over longer horizons.

- Short-term flow is two-sided: 24h options volume was $2.86B with calls 51.82% vs puts 48.18%, indicating ongoing upside participation alongside meaningful near-term hedging demand.

- Liquidity concentrated on Deribit: Deribit led with $1.48B volume, followed by Bybit ($630M), Binance ($373M), OKX ($316M), and CME ($64M), reinforcing Deribit’s role as the primary price-discovery venue for BTC options.

- Strike/expiry positioning suggests “upside tails + nearby protection”: Largest OI at a $120K call (Dec 25) and a large $80K call (Jul 31), paired with sizable $60K put (Jun 26)—a blend consistent with bullish longer-dated exposure while guarding against near-term drawdowns.

- Immediate hedging focus near ~$63K: Most traded contract was a $63K put (Jun 19), highlighting demand for short-dated downside insurance around that level.

💡 Strategic Points

- Read OI vs volume together: Call-heavy OI suggests bullish carry positioning, but near-even daily volume warns that traders are actively managing risk rather than expressing one-way conviction.

- Watch key expiries for volatility: Heavy activity into Jun 19 and Jun 26 implies these dates may amplify spot moves via hedging/adjustments as options approach expiry.

- Potential “pin” and gamma effects around popular strikes: Concentrated trading and OI near $60K–$65K puts can increase sensitivity of dealer hedging flows, potentially intensifying moves if BTC trades near those levels.

- Upside skew remains present: Large OI at $80K (Jul 31) and $120K (Dec 25) reflects persistent demand for upside convexity—often used as leveraged participation or tail exposure.

- Venue signals matter: With Deribit dominating turnover, changes in Deribit implied volatility, skew, and block prints may be more informative than smaller venue flows.

📘 Glossary

- Options Open Interest (OI): Total number of outstanding option contracts that have not been closed or expired; a proxy for accumulated market positioning.

- Call Option: Contract giving the holder the right (not obligation) to buy the underlying asset at a specified strike price by (or at) expiry.

- Put Option: Contract giving the holder the right (not obligation) to sell the underlying asset at a specified strike price by (or at) expiry.

- Strike Price: The preset price at which the option holder can buy (call) or sell (put) the asset.

- Expiry (Expiration Date): The date an option contract ends and settles or becomes void if not exercised.

- Hedging: Using derivatives (often puts or spreads) to reduce downside risk or volatility exposure.

- Implied Volatility (IV): The market’s priced expectation of future volatility, embedded in option premiums.

- Skew: The relative pricing/IV difference between calls and puts at different strikes, often reflecting demand for downside protection.

Comment 0