News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

South Korea’s domestic politics is increasingly being treated as tradable risk on global crypto rails, as blockchain prediction market Polymarket lists high-volume contracts tied to Korean elections and even the tenure of President Lee Jae-myung.

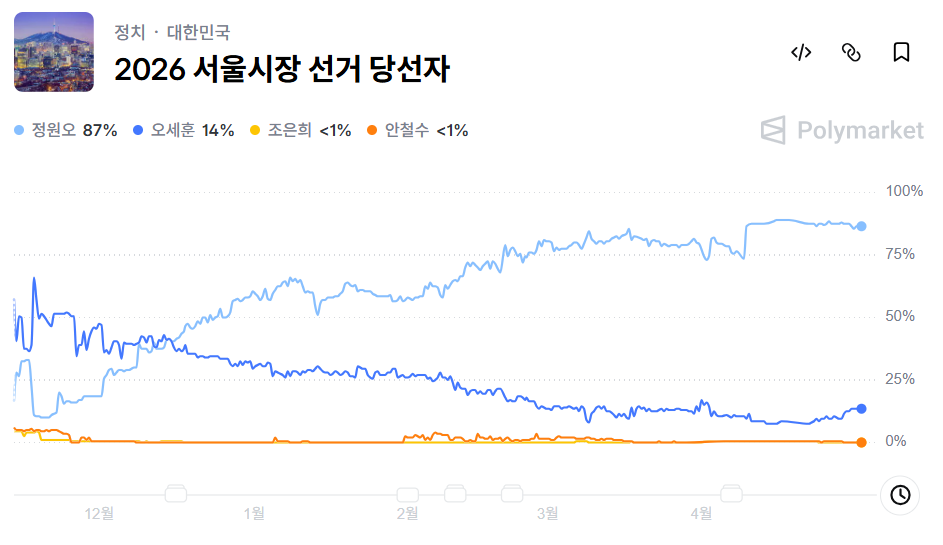

Data reviewed as of May 2, 2026 (UTC) shows Polymarket’s market on the winner of the June 3 Seoul mayoral election has amassed roughly $33.67 million in cumulative volume—about 46 billion won—underscoring how political outcomes are being converted into a liquid, 24/7 financial instrument for international traders.

Polymarket, headquartered in New York, allows users to buy and sell ‘Yes’/‘No’ contracts whose prices function as an implied probability. A ‘Yes’ share priced at $0.87 indicates the market assigns a roughly 87% chance to that outcome; a winning share settles at $1 while losing shares expire at $0. Unlike traditional opinion polling, participants risk real capital—an incentive structure proponents argue can make prediction markets faster at incorporating new information.

In the Seoul mayoral market, Democratic Party candidate Jung Won-oh was implied at 87% versus 14% for People Power Party candidate Oh Se-hoon, according to the market snapshot. A long tail of other figures—including Ahn Cheol-soo, Han Dong-hoon, Cho Kuk, Na Kyung-won, and Kang Hoon-sik—were all priced below 1%.

The pricing has moved sharply alongside political headlines. After a mid-April JTBC poll showed Jung leading 50% to 34%, the market tilted more decisively toward a Jung victory. On April 14, after President Lee publicly praised Jung by citing a 92.9% local approval metric, Jung’s implied odds jumped from 84% to 91% in a short window—illustrating how a single high-profile statement can be translated almost instantly into price.

Polymarket has also opened a new contract explicitly tied to presidential continuity. On April 24 (UTC), traders began betting on whether President Lee would leave office within 2026 through resignation or impeachment. Supporters of prediction markets argue that such contracts offer a continuous signal of perceived political stability; critics counter that they commodify democratic legitimacy and can create perverse incentives for manipulation.

The growing traction of prediction markets has been a broader U.S.-driven phenomenon. Polymarket and rival platform Kalshi have expanded rapidly over the past year, with Kalshi estimated to command around 90% share of the U.S. market while Polymarket remains highly competitive internationally. The two firms reportedly spent a combined $1 million on U.S. federal lobbying in 2025, and both have brought on President Trump’s eldest son, Donald Trump Jr., as an adviser. Polymarket has also established a Washington, D.C. office branded as ‘The Situation Room,’ signaling a sharper focus on policy and regulatory engagement.

That growth has been accompanied by intensifying controversy centered on two issues: ‘insider trading’ and gambling regulation.

On the insider information front, U.S. prosecutors charged U.S. Army Special Forces Master Sergeant Gannon Ken Van Dyke with allegedly using classified knowledge from a Venezuela-related operation to generate about $410,000 in Polymarket profits. The case drew outsized attention partly because many prediction-market traders transact through crypto wallets that do not publicly link to real-world identities, complicating enforcement and surveillance. Separately, an anonymous trader reportedly earned roughly $300,000 by correctly predicting four clemency actions announced at the end of Joe Biden’s presidency, fueling further scrutiny over whether politically sensitive contracts invite abuse.

Regulatory pushback has been even more complicated around sports. Sports-related contracts are estimated to account for roughly 90% of Kalshi volume and about 38% of Polymarket volume, placing the sector at the center of a jurisdictional clash. More than 20 U.S. states have moved to classify the platforms as unlicensed sports gambling and issued cease-and-desist orders. The companies, however, argue they are federally regulated ‘event contract’ venues under the Commodity Futures Trading Commission (CFTC), not state-regulated sportsbooks. In April, a federal appeals court sided with Kalshi in a key dispute, ruling that New Jersey regulators could not block its sports contracts—an outcome widely viewed as a tailwind for the broader industry.

Silicon Valley heavyweight Andreessen Horowitz has entered the debate, backing the industry’s framing of prediction markets as a ‘price discovery’ tool rather than gambling. In an 18-page submission filed with the CFTC in April, the venture firm argued that state-by-state restrictions create barriers to fair market access. It also contended that blockchain-based prediction markets can offer stronger transparency because on-chain transactions are auditable, even if user identities are not always visible.

CFTC Chair Mike Selig has taken an expansive view of federal authority, stating that event contracts resemble ‘swaps’ and therefore fall under the agency’s exclusive jurisdiction. At the same time, Democratic lawmakers have pushed the opposite direction. On April 30 (UTC), Senator Jeff Merkley led a group urging the CFTC to prohibit contracts tied to elections, wars, military operations, and government actions. Companion proposals such as the ‘Prediction Markets Are Gambling Act’ and the ‘STOP Corrupt Bets Act’ have been introduced in Congress, reflecting a growing political fight over where the line between information markets and gambling should be drawn.

In a self-referential twist, prediction markets are also pricing their own political risk. Traders currently imply only an 11% chance of a federal ban on sports prediction markets in the U.S. in 2026—an example of how the sector is attempting to quantify threats to its own business model in real time.

For South Korea, the appearance of high-liquidity contracts tied to Korean political outcomes raises policy and societal questions that go beyond novelty. First is regulatory reach: whether and how Korean authorities can respond when domestic political events are financialized on offshore platforms. Second is legal classification: whether Korea’s capital markets framework and criminal prohibitions on gambling can clearly encompass blockchain-based ‘event contracts,’ an area that remains contested even in the U.S. Third is a more fundamental question about democratic norms—whether markets pricing political outcomes constitutes legitimate information aggregation, or an uneasy form of ‘financialization’ that turns governance into a speculative asset class.

What is clear is that the mechanism is already in motion. The June 3 Seoul mayoral election will not only decide the leadership of South Korea’s capital; it will also trigger settlement on a global prediction market that has turned the result into a multi-tens-of-millions-of-dollars financial event.

🔎 Market Interpretation

- Politics as a tradable instrument: South Korea’s domestic political outcomes are being “financialized” via crypto-based prediction markets, with Polymarket offering liquid, 24/7 contracts on events like the Seoul mayoral election and even President Lee Jae-myung’s tenure.

- Seoul mayoral market shows institutional-like liquidity: The June 3 Seoul mayoral winner contract reached about $33.67M cumulative volume (~46B KRW) as of May 2, 2026 (UTC), signaling strong global trader participation and price responsiveness to headlines.

- Odds behave like real-time probabilities: Polymarket “Yes/No” share prices function as implied probabilities (e.g., $0.87 ≈ 87%), settling at $1 if correct and $0 if wrong—creating continuous market-based “probability” signals rather than periodic polling snapshots.

- Headline-to-price transmission is rapid: After a JTBC poll and President Lee’s public praise of Jung Won-oh, Jung’s implied odds quickly jumped (e.g., 84% → 91%), illustrating how narrative shocks can be instantly converted into market price changes.

- Regulatory risk is part of the pricing loop: Markets also bet on their own constraints; traders imply only an 11% chance of a U.S. federal ban on sports prediction markets in 2026, reflecting a self-referential risk-pricing dynamic.

💡 Strategic Points

- Watch implied odds as a “sentiment index,” not a forecast: Prices reflect trader positioning and information flow, but can be influenced by liquidity, large wallets (“whales”), and narrative momentum—especially in politically sensitive markets.

- Understand the settlement trigger and timing: For the Seoul race, settlement occurs when the election outcome is finalized—turning an election result into a direct financial payoff event for global participants.

- Incentives create both efficiency and vulnerability: Risking capital can tighten information aggregation versus polling, but also raises manipulation concerns (coordinated betting, information operations, or strategic rumor amplification).

- “Presidential continuity” contracts introduce legitimacy concerns: The Lee resignation/impeachment-in-2026 contract reframes governance stability as a tradable probability, which critics argue can commodify democratic legitimacy and invite perverse incentives.

- Offshore venue complicates Korean policy response: Korea faces questions of regulatory reach when contracts are listed abroad and traded via crypto wallets, limiting direct enforcement and creating cross-border jurisdiction gaps.

- Korean legal classification remains unresolved: Authorities may need to determine whether these contracts fall under capital-markets rules, gambling prohibitions, or a new category—mirroring the unresolved U.S. split between “event contracts” (CFTC) and state gambling frameworks.

- U.S. regulatory battle sets global precedent: Kalshi/Polymarket expansion, heavy lobbying, and a federal appeals court win for Kalshi on sports contracts strengthen the industry’s position, potentially influencing how other jurisdictions (including Korea) interpret similar products.

- Insider-information risk is a central threat vector: High-profile allegations (e.g., a U.S. soldier accused of using classified info; traders profiting from clemency outcomes) intensify scrutiny and may accelerate restrictions on political/government-action contracts.

- Policy scenarios for Korea: (1) tolerate as offshore “information markets,” (2) restrict access via platform/app/payment controls, (3) pursue coordinated international enforcement, or (4) develop a regulated domestic framework—each with tradeoffs for speech, market integrity, and investor protection.

📘 Glossary

- Prediction Market: A market where contracts pay based on the outcome of an event (election, policy decision, sports result), allowing prices to reflect collective expectations.

- Yes/No Contract: A binary contract that settles at $1 if the specified event happens (“Yes”) and $0 if it does not (“No”).

- Implied Probability: The probability suggested by the market price (e.g., $0.87 ≈ 87%), not a guaranteed forecast.

- Cumulative Volume: Total dollars traded over time on a market/contract; higher volume usually indicates greater liquidity and stronger price discovery.

- Liquidity: How easily traders can buy/sell without moving the price significantly; higher liquidity generally improves market reliability.

- Price Discovery: The process by which markets aggregate information into a price, often cited by the industry to distinguish prediction markets from gambling.

- Event Contract: A regulated derivatives-style instrument (as argued by platforms) tied to an event outcome; in the U.S., this intersects with CFTC oversight debates.

- CFTC (Commodity Futures Trading Commission): U.S. federal regulator overseeing derivatives markets; central to whether prediction markets are treated as swaps/derivatives rather than gambling.

- Cease-and-Desist Order: A legal demand (often from state regulators) to halt an activity alleged to violate local rules, such as unlicensed sports betting.

- On-chain Transparency: Transactions recorded on a blockchain are auditable; however, wallet identities may be pseudonymous, complicating enforcement.

- Insider Trading (in this context): Using non-public or classified information to trade outcome contracts for profit, raising serious legal and ethical concerns.

Comment 0