News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

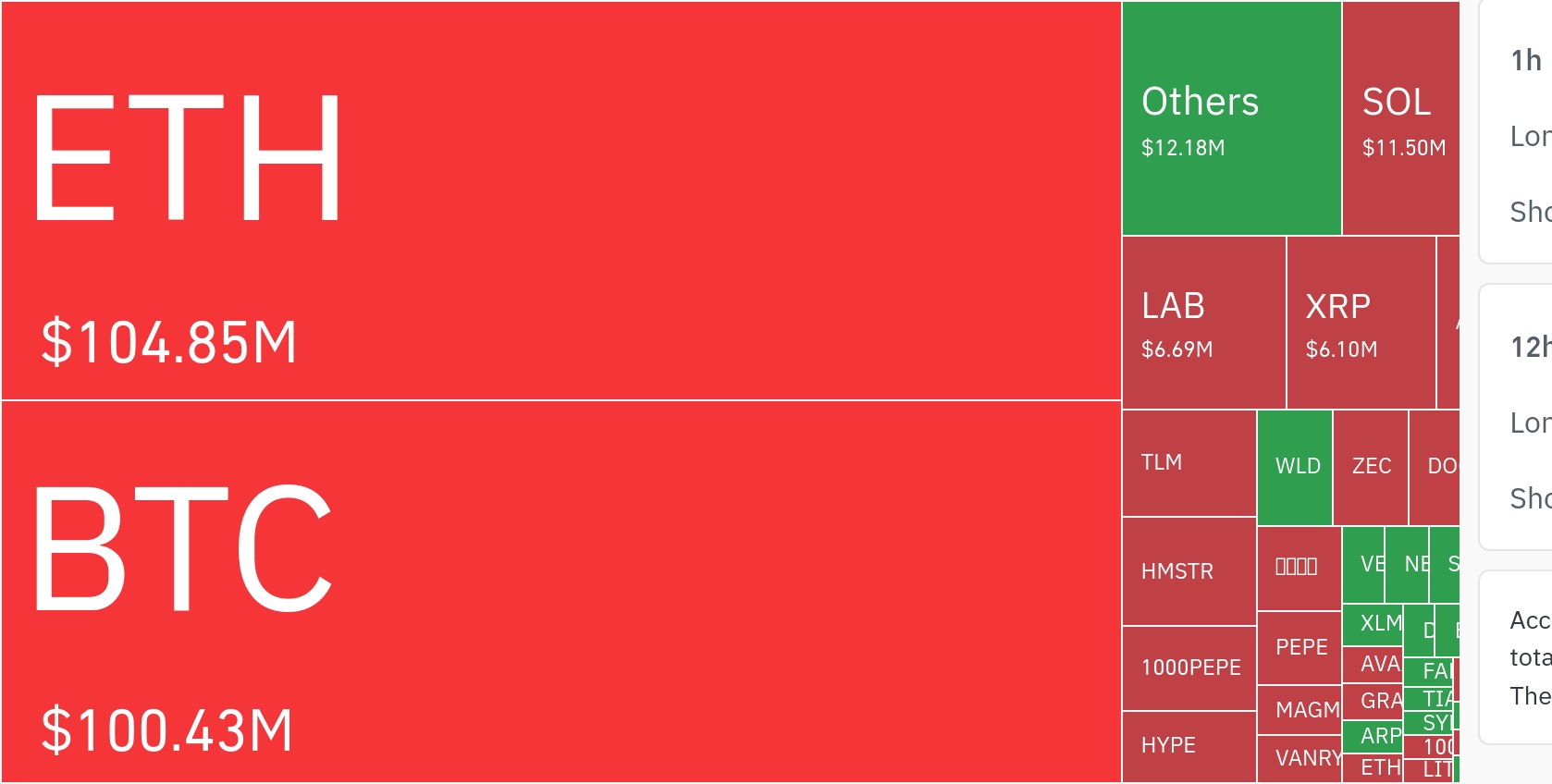

As crypto markets grapple with heightened volatility and sudden macro-driven moves, one investor lesson is resurfacing: ‘black swan’ events cannot be predicted—but portfolios can be built to withstand them.

The idea, popularized by risk theorist Nassim Nicholas Taleb, has regained traction among traders after a series of abrupt swings across major digital assets underscored how quickly sentiment and liquidity can reverse. In practice, the message challenges the common retail impulse to commit to a single narrative—bullish or bearish—and instead emphasizes flexibility and resilience when conditions change.

Taleb, a Lebanese-American mathematician, statistician, and former Wall Street options trader, is best known for developing the framework around ‘black swans’—rare, high-impact events that are difficult to foresee yet disproportionately shape market outcomes. In books including The Black Swan, Antifragile, and Skin in the Game, he argues that forecasting models tend to underestimate extremes, leaving investors exposed to abrupt shocks. Taleb has also been widely cited for profiting during the 2008 financial crisis by positioning for ‘tail risk’—the low-probability scenarios with outsized consequences.

In trading terms, the philosophy echoes the approach associated with legendary speculator Jesse Livermore: avoid ideological attachment to direction and follow the market’s observable trend. Rather than declaring permanent allegiance to a bull or bear thesis, the discipline is to buy when the market confirms strength and sell when it signals weakness—then reverse quickly when evidence suggests the trend has turned.

That mindset carries particular relevance for crypto, where leverage, fragmented liquidity, and a constant flow of policy headlines can amplify moves. A narrative that seems dominant in the morning can be undermined by a sudden change in risk appetite, an unexpected regulatory development, a large liquidation cascade, or an abrupt shift in macro expectations. Traders who refuse to reassess can end up magnifying losses precisely when the market regime changes.

From a risk-management perspective, Taleb’s framework points less to prediction and more to design: constructing exposure so the portfolio is not fragile to extreme outcomes. For crypto participants, that often translates into constraints on leverage, diversified custody and venue risk, position sizing that assumes large drawdowns are possible, and liquidity planning for periods when spreads widen and exits become costly. The goal is not certainty about what will happen next, but durability when the improbable arrives.

The broader implication for digital-asset markets is straightforward: as crypto integrates further into global risk systems, ‘black swan’ dynamics—sharp, discontinuous repricing driven by shocks rather than gradual trends—are likely to remain a feature, not a bug. In that environment, adaptability and ‘tail risk’ awareness may matter as much as conviction.

Comment 0