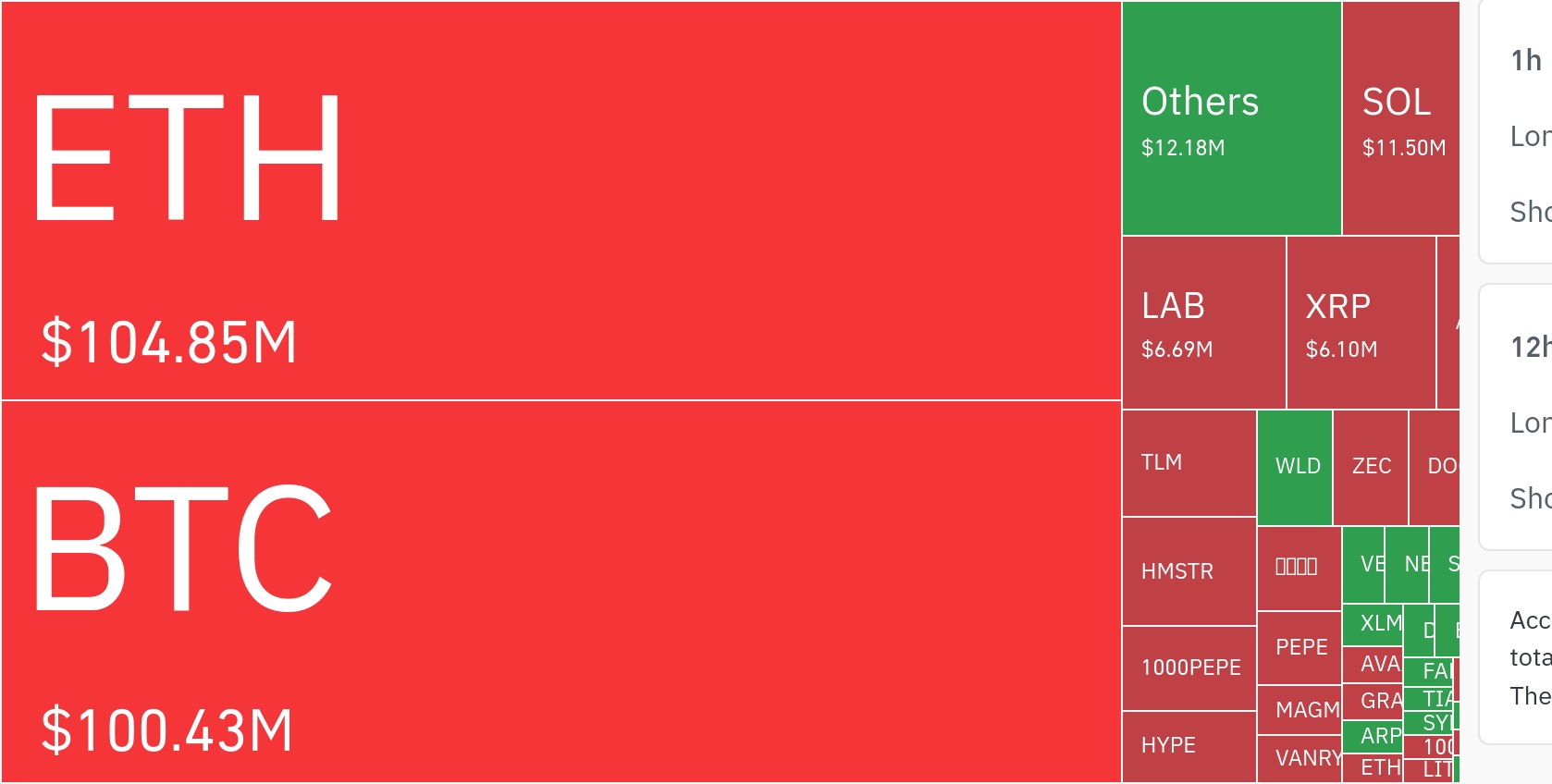

News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Digital asset markets entered the week with a rare mix of supportive ‘institutional demand’ signals and elevated macro-risk headlines, as fresh inflows into crypto investment products coincided with renewed geopolitical uncertainty in the Middle East and a busy U.S. policy calendar that could influence liquidity expectations.

According to CoinShares, digital asset investment products recorded $1.2 billion in net inflows over the past week, marking a fourth consecutive week of additions. Total assets under management climbed to $155 billion, data shared by Wu Blockchain on Monday UTC showed. Bitcoin (BTC) led the move with $933 million of net inflows, while Ethereum (ETH) attracted $192 million—its third straight week of net additions—reinforcing the view that allocators are concentrating exposure in the sector’s most liquid benchmarks.

The flow data comes as several macro developments complicate risk sentiment. Reports citing regional intelligence feeds said U.S. Central Command directed 38 vessels to return to Iranian ports amid heightened tensions, stoking concerns about maritime logistics and potential spillovers into global markets. In parallel, Odaily reported that President Trump was expected to review proposals at a National Security Council meeting aimed at reopening the Strait of Hormuz and ending hostilities—an issue closely watched by investors given the strait’s role as a critical conduit for global oil shipments. Iran’s Foreign Minister Abbas Araghchi also said Tehran is reviewing a U.S. proposal for talks, according to CGTN, adding to expectations of a potential diplomatic off-ramp.

In crypto, corporate accumulation remained a focal point. Strategy ($MSTR) disclosed it bought an additional 3,273 BTC last week for roughly $255 million at an average price of about $77,906 per coin, according to reports carried by Odaily. As of April 26, Strategy held 818,334 BTC acquired for approximately $61.81 billion, with an average cost basis of about $75,537. The firm’s continued purchases have become a bellwether for public-market appetite for Bitcoin exposure, particularly during periods when ETF flows and broader ‘liquidity inflow’ narratives are under scrutiny.

Traditional finance infrastructure players also signaled deeper engagement with blockchain rails. Western Union ($WU) is planning to launch a Solana (SOL)-based stablecoin, USDPT, as soon as next month, The Block reported, with PANews relaying the details on Monday UTC. The token is designed primarily for settlement between Western Union headquarters and its agent network rather than consumer-facing payments, positioning it as a potential alternative to legacy cross-border messaging and settlement channels such as SWIFT. The company is also building a digital asset network linking crypto wallets to its retail and agent footprint, with the goal of enabling wallet users to convert digital assets into local currency at Western Union locations. Separately, Western Union reportedly aims to roll out U.S. dollar–based stablecoin cards across dozens of markets later this year, allowing consumers to hold and spend stablecoins globally.

On the regulatory front, market participants are increasingly focused on a narrow U.S. legislative window. Odaily reported that the period around the Memorial Day holiday—May 25 this year—has emerged as a key timing marker for visible progress on a crypto market structure bill, with observers warning that momentum could fade as the summer election cycle intensifies. Outstanding points under debate reportedly include stablecoin yield and certain DeFi-related sales conduct. More than 100 organizations have urged the Senate Banking Committee to begin formal consideration, calling for the next step forward on the ‘Clarity’ bill framework intended to codify regulatory principles and reduce policy whiplash.

Meanwhile, shifting expectations around the Federal Reserve’s leadership are re-entering the conversation as a potential driver of rates and dollar liquidity assumptions. Odaily reported that Sen. Thom Tillis said he would support the confirmation of Kevin Warsh as Fed chair, removing what sources described as the last major obstacle to President Trump’s choice. Tillis had previously withheld support while a Justice Department inquiry involving Jerome Powell was ongoing, arguing the probe represented an attack on central bank independence; the investigation was reported to have concluded last Friday.

Still, Goldman Sachs ($GS) cautioned that a leadership change would not necessarily translate into rapid easing. In a client note cited by Odaily, Goldman economist David Mericle said a new chair would face constraints from the Federal Open Market Committee, and that it could be difficult to push through faster cuts amid internal disagreement and continued uncertainty tied to the Middle East conflict. Goldman maintained its baseline call for two 25-basis-point rate cuts—one in September and one in December—suggesting easing expectations remain intact but not imminent.

In DeFi, Circle said Circle Ventures is purchasing Aave (AAVE) tokens, framing the move as support for a protocol it says is helping shape the future of on-chain finance. The announcement points to a widening effort by the stablecoin issuer to strengthen ties with core DeFi infrastructure as competition intensifies across lending, liquidity, and payments.

Exchange-traded product flows also broadened beyond BTC and ETH. XRP (XRP) spot ETFs recorded $15.74 million in net inflows last week, according to SoSoValue data cited by PANews, covering the April 20–24 period in U.S. Eastern Time. Bitwise’s XRP ETF led weekly inflows at $8.86 million, bringing cumulative inflows to about $426 million, while Franklin’s XRPZ added $4.66 million for the week, lifting cumulative inflows to roughly $349 million. Total net asset value across XRP spot ETFs stood near $1.1 billion, representing about 1.23% of XRP’s market capitalization, with cumulative inflows reported at $1.29 billion.

Taken together, the week’s headlines underscore a market being pulled in two directions: crypto-native indicators are flashing continued accumulation and product inflows, while geopolitics and U.S. policy timing remain key variables for broader risk appetite. For traders and long-term allocators alike, the near-term tone may hinge less on crypto-specific narratives and more on whether macro uncertainty eases enough to keep capital moving into ‘high-beta’ exposure.

Comment 0