News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

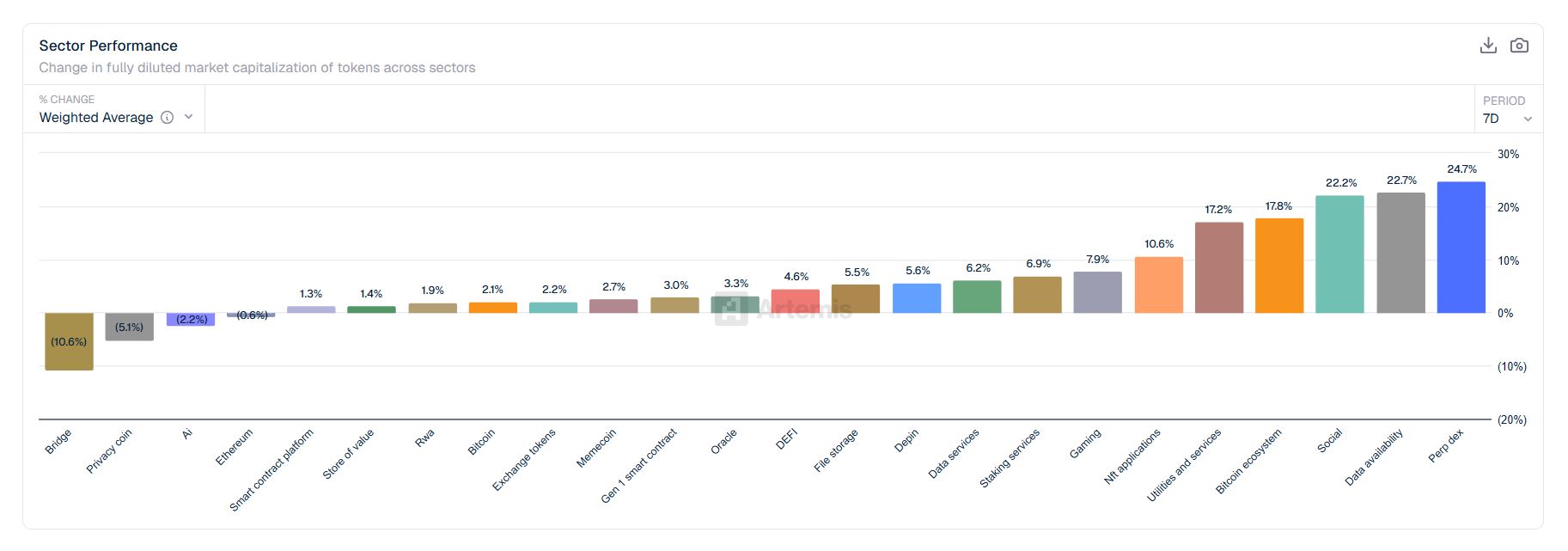

Crypto investors are rotating aggressively into deeper, infrastructure-adjacent themes such as 'derivatives DEX' and 'data availability', while last week’s leaders—particularly 'privacy' and Ethereum (ETH)—have started to give back gains, signaling a short-term shift in risk appetite and narrative leadership.

According to weekly sector performance data compiled by Artemis, the strongest gains as of April 21 UTC were concentrated in derivatives-focused decentralized exchanges, which recorded a 24.7% jump in weekly fully diluted valuation (FDV). Data availability followed with a 22.7% increase, alongside 'social' at 22.2% and the Bitcoin ecosystem at 17.8%, as multiple high-beta themes moved in tandem and emerged as the market’s new momentum cluster.

The move suggests capital is favoring areas tied to next-generation market structure and scaling—segments often associated with increased on-chain activity and the re-pricing of growth expectations. 'Data availability' refers to the layer of infrastructure that ensures transaction data is accessible for verification, a critical component for rollups and modular blockchain designs. The sharp gains in this cohort point to renewed interest in execution efficiency and throughput narratives rather than simple exposure to large-cap base assets.

Several cyclical sectors also showed a notable improvement in sentiment. Utilities and services, which rose 6.1% the previous week, accelerated to a 17.2% gain. NFT applications climbed 10.6% and gaming rose 7.9%, indicating that speculative appetite is broadening beyond a single category and returning to consumer-facing crypto themes.

More defensively positioned 'data and service' verticals posted steadier but widespread inflows. Staking services rose 6.9%, data services 6.2%, DePIN (decentralized physical infrastructure networks) 5.6%, and file storage 5.5%. The breadth of gains across these segments suggests allocation is not purely momentum-driven, but also consistent with investors seeking exposure to revenue-linked or usage-tied infrastructure narratives.

Core market categories remained positive but less explosive: DeFi gained 4.6%, oracles 3.3%, and first-generation smart contract platforms 3.0%. Meanwhile, meme coins rose 2.7%, exchange tokens 2.2%, and Bitcoin (BTC) itself added 2.1%, reflecting a generally constructive tape even as leadership rotated away from last week’s winners. Real-world assets (RWA), which had dropped 13.8% in the prior week, stabilized with a 1.9% increase—an early sign that forced selling or fast money exits may be easing.

On the downside, bridges were the weakest sector, falling 10.6% as capital continued to exit riskier plumbing layers often viewed through the lens of security and exploit risk. More notably, 'privacy coins'—the top-performing category last week—reversed to a 5.1% decline, while Ethereum (ETH) slipped 0.6%. The pullback in both segments points to near-term profit-taking and a market increasingly willing to rotate rather than chase crowded trades.

AI-related tokens also extended losses, down 2.2% for the week, underscoring an unusual pattern in which tech-adjacent crypto themes are correcting even as other speculative sectors rally. That divergence may reflect selective positioning rather than a broad “risk-on” regime, with traders favoring areas perceived to have clearer catalysts tied to on-chain adoption and new product cycles.

Overall, the latest FDV-based sector map highlights a market that remains upwardly biased but increasingly fragmented, with performance driven by rotation into targeted infrastructure trends rather than a uniform lift across major base layers. If the trend holds, leadership could remain concentrated in modular scaling and trading-venue narratives—while large-cap platforms such as Ethereum may need fresh catalysts to regain momentum.

🔎 Market Interpretation

- Narrative rotation is driving returns: Capital is moving away from last week’s leaders (privacy, ETH) and into infrastructure-adjacent, higher-beta themes—especially derivatives DEX (+24.7% FDV) and data availability (+22.7%).

- “Growth infrastructure” takes leadership: Outperformance in data availability and trading-venue narratives suggests investors are pricing in increased on-chain activity, scaling demand, and next-gen market structure rather than simply buying large-cap base assets.

- Risk-on, but selective: Consumer/speculative segments (NFT apps +10.6%, gaming +7.9%, utilities/services +17.2%) are improving, yet AI tokens fell (-2.2%), implying positioning is catalyst-driven rather than a broad-based tech rally.

- Risk is being repriced in “plumbing” layers: Bridges (-10.6%) lag due to persistent security/exploit overhang, indicating investors are avoiding infrastructure with asymmetric tail risk.

- Large caps are steady but not leading: BTC (+2.1%) and core categories (DeFi +4.6%, oracles +3.3%) remain positive, while ETH (-0.6%) signals fading momentum and profit-taking.

💡 Strategic Points

- Track leadership by cluster, not by market beta: The market is “upward biased but fragmented,” so relative strength may persist in modular scaling and trading infrastructure even if majors move sideways.

- Watch for confirmation via on-chain and product catalysts: Sustained leadership in derivatives DEX and data availability likely depends on user growth, volume/fees, new launches, and rollup/modular adoption metrics.

- Manage rotation risk: Last week’s winners (privacy) quickly flipped negative—highlighting the likelihood of short holding periods and rapid profit-taking in crowded themes.

- Avoid or hedge structurally risky segments: Bridges underperforming reinforces that security perception can dominate fundamentals; prudent sizing and diversification across infrastructure types may reduce tail-risk exposure.

- Look for stabilization signals in beaten categories: RWA moved from -13.8% (prior week) to +1.9%, suggesting forced selling may be easing—often an early setup for mean reversion if broader sentiment holds.

📘 Glossary

- FDV (Fully Diluted Valuation): Market cap assuming all tokens are circulating; useful for comparing sectors but can overstate value if large unlocks remain.

- Derivatives DEX: Decentralized exchanges offering perpetuals/options/futures; typically high-beta because activity and fees can scale quickly with volatility and speculation.

- Data Availability (DA): Infrastructure ensuring transaction data is published and retrievable for verification—critical for rollups and modular chains to maintain security.

- Rollups: Layer-2 systems that execute transactions off-chain and post proofs/data to a base chain to reduce costs and increase throughput.

- Modular blockchain design: Separating execution, settlement, consensus, and data availability into specialized layers to improve scalability and flexibility.

- DePIN: Decentralized Physical Infrastructure Networks—crypto networks coordinating real-world resources (e.g., wireless, compute, sensors) via token incentives.

- RWA (Real-World Assets): Tokenized claims on off-chain assets (e.g., treasuries, credit, commodities) traded/managed on-chain.

- Narrative leadership: The themes attracting the most incremental capital and attention, often changing quickly in crypto markets.

Comment 0