News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

With the first quarter set to close on March 31, crypto investors are being urged to do something many avoid in a drawdown: open their portfolios, review decisions in cold detail, and separate market damage from self-inflicted mistakes. The message lands as Bitcoin (BTC) and Ethereum (ETH) head into quarter-end nursing steep losses, while traditional ‘risk-off’ assets have held up far better—an uncomfortable contrast that is shaping sentiment and positioning going into Q2.

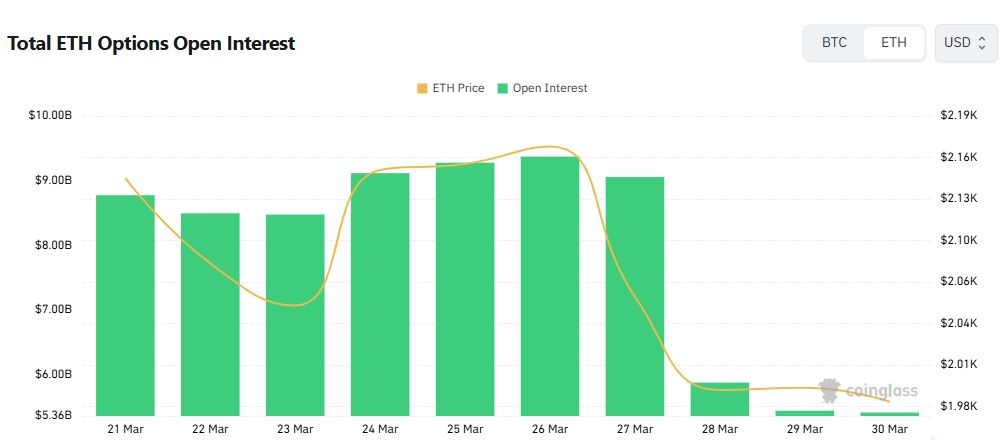

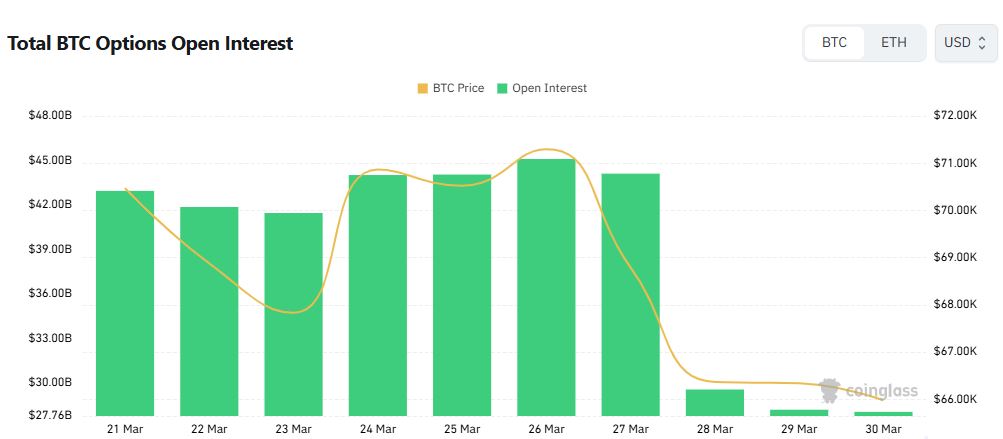

As of Monday ET, Bitcoin is down roughly 23% for the quarter, while Ethereum has fallen about 32%. Over the same period, gold has climbed around 19%, and the S&P 500 has slipped only modestly, underscoring how decisively capital has leaned away from high-beta crypto exposures. The broader digital asset market has shed approximately $900 billion in total market capitalization during Q1, according to figures cited in the report.

Sentiment indicators remain deeply pressured. The Crypto Fear & Greed Index is sitting at 13—‘extreme fear’—a condition the report says has persisted for more than 46 consecutive days, marking the longest such streak since the aftermath of the FTX collapse in late 2022. While fear gauges can sometimes be interpreted as contrarian, the duration of the current reading is being framed less as a buy signal and more as evidence that confidence has not yet stabilized.

Macro and flow dynamics have compounded the downturn. The report points to a renewed uptick in inflation that has weakened expectations for near-term rate cuts, alongside net institutional outflows from spot crypto ETFs. Geopolitical risk in the Middle East is also cited as an additional layer of uncertainty, reinforcing demand for safety and liquidity rather than speculative exposure. Together, those forces have made quarter-end ‘window dressing’ rallies harder to rely on and have increased the cost of being early on a rebound.

Instead of predicting an imminent reversal, the report’s central argument is behavioral: the day before a quarter closes is when performance and process are easiest to audit. It encourages investors to parse losses into two buckets—what the market imposed and what came from poor sizing, broken rules, or thesis drift—before the psychological reset of a new quarter makes prior mistakes easier to rationalize away.

The report segments this advice through four investor “types,” each with different risk tolerances and decision-making styles. For data-driven, long-horizon builders, the emphasis is on documenting Q1 trades and distinguishing disciplined execution from rule-breaking. It also notes that ‘smart money’ appeared to add exposure during February’s pullback, citing whale accumulation of about 3.7% of holdings during that period—an observation used to argue for planning rather than panic. The warning: don’t rewrite a multi-year thesis because of a single quarter’s drawdown.

For conviction-led participants, the guidance is sharper: articulate the evidence behind belief. If the rationale cannot be written down in concrete terms, the report argues, what feels like conviction may be mere attachment. Even long-term holders are urged to diagnose whether losses were primarily market-driven or the result of oversized positions, because entering Q2 without a post-mortem increases the odds of repeating the same errors.

More tactical traders are advised to inventory every Q1 entry and exit to identify which ‘signals’ repeatedly triggered action—and whether those triggers produced consistent outcomes. In that framing, the pattern matters more than the P&L number. The report cautions against initiating new positions purely on hopes of a quarter-end bounce, noting that a prolonged ‘extreme fear’ regime can signal that rebound timing remains unclear, and that the urge to “make the quarter look better” can distort judgment.

Finally, for opportunistic allocators focused on rotating into relative strength, the report highlights that some AI-linked and gold-correlated tokens outperformed the broader market in Q1. Investors are encouraged to check whether their portfolio captured those pockets of resilience—and if not, to document why the opportunity was missed. The broader takeaway is risk management rather than revenge trading: poor Q1 performance, it argues, is not a justification for escalating aggression in Q2.

As Q1 comes to a close, the report’s conclusion is straightforward: investors who skip the portfolio review now are more likely to carry the same behavioral errors into the next quarter. In a market still defined by ‘extreme fear,’ weakening rate-cut expectations, and uncertain institutional flows, process discipline may matter as much as any single directional call—especially when the next macro catalyst is not yet clearly in view.

🔎 Market Interpretation

- Q1 risk-off dominance: Bitcoin (-23%) and Ethereum (-32%) underperformed while gold (+19%) and the S&P 500 held up better, reinforcing a clear preference for safety/liquidity over high-beta crypto exposure.

- Confidence remains fragile: Crypto Fear & Greed Index at 13 ("extreme fear") for 46+ days—framed less as a contrarian buy signal and more as persistent instability in sentiment.

- Macro headwinds and flows: Renewed inflation reduced near-term rate-cut expectations, while spot crypto ETF institutional outflows added pressure; Middle East geopolitical risk amplified risk aversion.

- Positioning into Q2: Quarter-end "window dressing" rallies are portrayed as less reliable; being early on a rebound is costlier amid unclear catalyst timing and shaky flows.

- Scale of the drawdown: The digital asset market lost roughly $900B in market cap over Q1, highlighting broad-based deleveraging and tighter risk budgets.

💡 Strategic Points

- Run a Q1 post-mortem before the reset: Separate losses into (1) market-imposed drawdown and (2) self-inflicted errors (oversizing, broken rules, thesis drift) to avoid repeating them in Q2.

- Builders (data-driven, long horizon): Document trades and rule adherence; don’t rewrite a multi-year thesis because of one quarter. Note: report cites whale accumulation (~3.7% added in February) as a reason to plan rather than panic.

- Conviction-led investors: Write down the evidence behind each conviction. If it can’t be stated concretely, it may be attachment. Re-check position sizing so “long-term” doesn’t become “overexposed.”

- Tactical traders: Inventory every entry/exit and map triggers to outcomes; prioritize process consistency over quarter-end P&L optics. Avoid new positions based solely on hopes of a bounce during prolonged extreme fear.

- Opportunistic/rotation allocators: Review whether you captured Q1 relative strength (AI-linked and gold-correlated tokens mentioned). If missed, document why (mandate limits, signal absence, execution delay) to refine rotation rules.

- Risk management over revenge trading: Poor Q1 performance is not a rationale to increase aggression; tighten decision frameworks while macro catalysts and institutional flows remain uncertain.

📘 Glossary

- Drawdown: Peak-to-trough decline in an asset or portfolio over a period.

- Risk-off: Market regime where investors prefer safer, more liquid assets (e.g., cash, government bonds, gold) over higher-risk assets.

- High-beta: Assets that tend to move more than the broader market—often amplifying both gains and losses.

- Crypto Fear & Greed Index: A sentiment gauge (0–100) where low values indicate fear; “extreme fear” signals strong negative sentiment.

- Contrarian indicator: A metric some traders use to take the opposite side of crowded sentiment (e.g., buying when fear is high).

- Spot crypto ETF flows: Net money entering or leaving exchange-traded funds that hold actual crypto; outflows can reflect reducing institutional exposure.

- Window dressing: End-of-quarter positioning to improve the appearance of holdings/performance, sometimes creating temporary price moves.

- Thesis drift: Gradual deviation from the original investment rationale without explicit reevaluation.

- Whale accumulation: Net buying by very large holders; often tracked as a potential signal of longer-horizon positioning.

- Relative strength: Assets outperforming a benchmark or peers during the same period.

Comment 0