News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Global markets ended the session split along unusual lines as a sharp round-trip in oil prices failed to dictate broader risk sentiment, while Bitcoin (BTC) and gold strengthened as preferred hedges amid intensifying Middle East uncertainty.

The whipsaw was triggered after reports that Iran swiftly rejected a 15-point ceasefire proposal presented by the United States, undermining hopes for a rapid de-escalation and pushing crude into extreme intraday volatility. U.S. equities and Treasury bonds, however, largely ‘looked through’ oil’s late rebound, closing according to their own technical and positioning dynamics rather than headline-driven energy moves.

Market attention shifted quickly from an initial ‘risk-on’ reaction—oil down and stocks up in after-hours trading—to renewed concern as Iran’s rhetoric hardened even after fresh reports of strikes near the Bushehr nuclear power facility. Iranian officials reiterated that the timeline for ending the conflict would be decided by Tehran, dampening expectations that diplomacy would quickly cap escalation risks.

Prediction market pricing reflected that skepticism. On Polymarket, the implied probability of a ceasefire before the end of April failed to rise meaningfully despite the U.S. proposal, signaling traders were reluctant to fade the geopolitical premium being priced into energy and volatility markets.

In oil, West Texas Intermediate (WTI) futures fell roughly 6% to 7% from the prior session’s highs before recovering most of the decline by the close. Key intraday catalysts included early reports of Iran rejecting the ceasefire plan, a mid-session spike that briefly pushed WTI to an intraday peak near $90 per barrel, and later headlines that President Trump is expected to visit China on May 14–15—news that some traders interpreted as a potential diplomatic off-ramp, helping stabilize crude before prices swung again on renewed war-related commentary.

U.S. equities finished modestly higher, but the gains were largely concentrated in the initial gap move following the ceasefire headline. Once the regular session began, major indices churned sideways and struggled to clear key technical resistance levels. Small caps outperformed on a relative basis, while the S&P 500 logged its sixth consecutive session with an intraday range of at least 1%, underscoring the market’s fragile footing.

Goldman Sachs’ trading desk said overall volumes were down about 3% versus the prior two weeks, while ETFs accounted for roughly 37% of tape activity—an indication that flows, rather than high-conviction discretionary risk-taking, were dominating price action. The bank noted hedge funds were net buyers concentrated in technology, financials, and consumer discretionary, while long-only managers leaned toward industrials, consumer staples, and healthcare.

Nomura’s Charlie McElligott framed the session as a symptom of broader paralysis. He pointed to ‘macro volatility compression’ turning into career risk, skepticism toward quick conflict resolution, weakening labor indicators, structural labor-market shifts tied to AI adoption, and growing concerns around private credit liquidity—all contributing to what he described as an environment where many investors are effectively unable to trade with confidence.

Treasury markets, meanwhile, decoupled from oil. Yields declined even as crude clawed back losses, with the 30-year yield down about 4 basis points and the 2-year down around 2 basis points, signaling demand for duration as a hedge against both geopolitical risk and growth uncertainty. A weak 5-year auction did little to alter the broader bid for bonds. Inflation expectations, as measured by breakevens, fell on the day.

Rate-cut pricing in the U.S. remained restrained, with markets still reflecting limited conviction in imminent easing and comparatively more sensitivity to upside inflation risks. In contrast, expectations in the U.K. and euro zone tilted slightly more dovish, suggesting investors see a clearer path for policymakers there to support growth if conditions deteriorate.

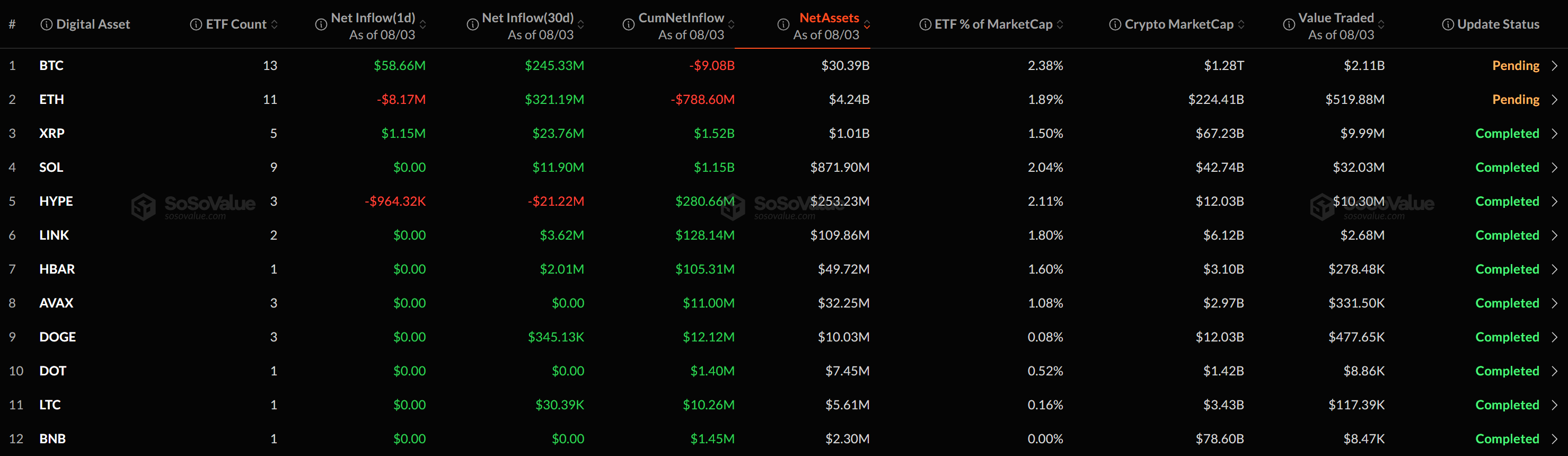

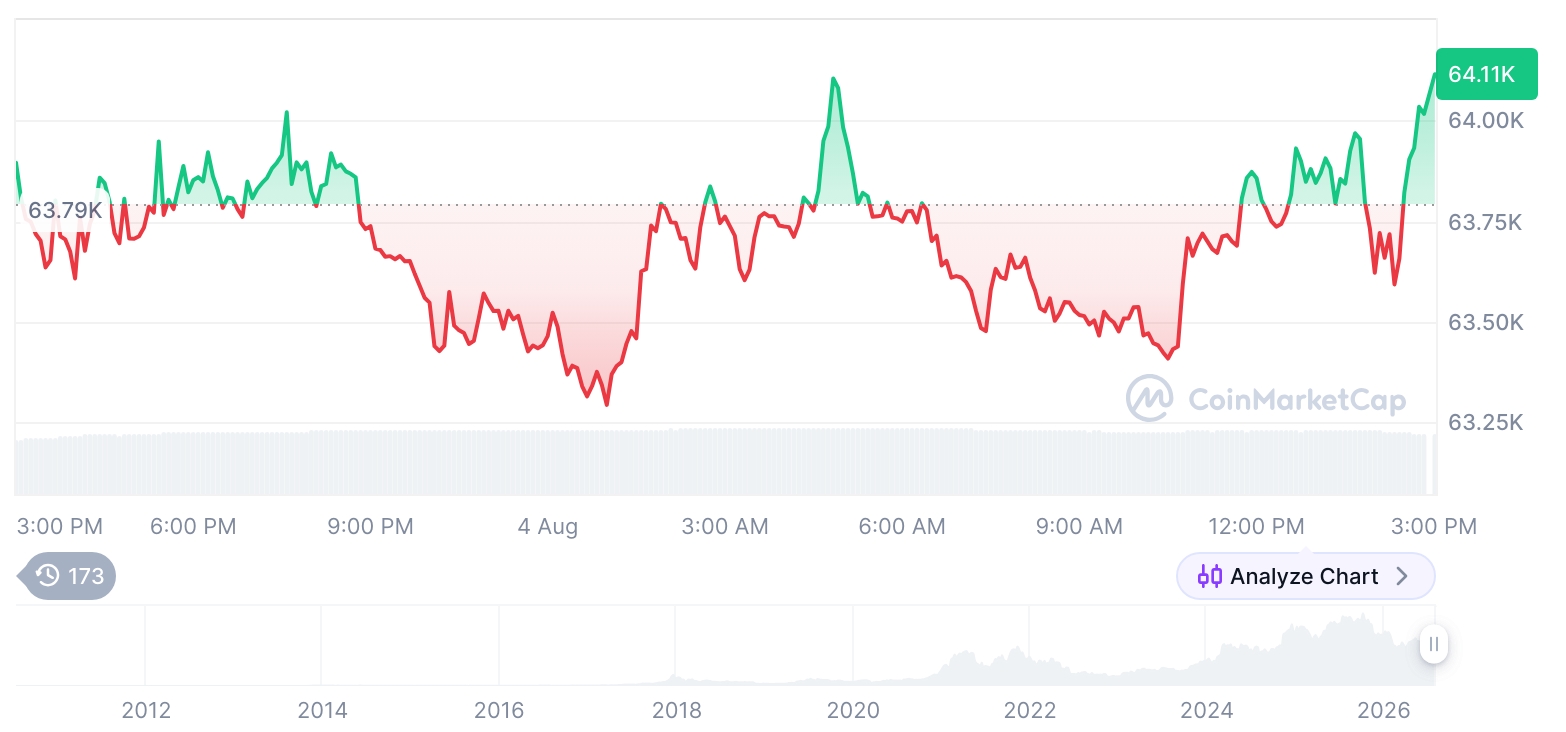

Crypto and precious metals stood out as the session’s clearest winners. Bitcoin (BTC) climbed to around $72,000 intraday before easing back to close near the $71,000 level. Gold extended a rebound from its 200-day moving average and attempted to push above $4,600 per ounce during the session. Notably, it was the first day since the outbreak of war that Bitcoin underperformed gold on a relative return basis, highlighting that markets were treating ‘hard’ defensive assets with renewed seriousness as geopolitical outcomes looked increasingly binary.

The U.S. dollar started weaker but firmed steadily through the session to finish near the prior day’s highs, reflecting a familiar pattern of initial risk repricing followed by renewed demand for liquidity and reserve currency exposure as headlines worsened.

Adding to the macro tension, U.S. import and export price data came in well above expectations, a result some analysts attributed partly to rising RAM prices. Outside the oil shock, the broader set of real-economy signals continues to look less supportive for equities, reinforcing concerns that earnings and valuations may be vulnerable if growth slows while inflation remains sticky.

Goldman Sachs strategist Shriti Kapa said the MSCI World Index is down roughly 7% since the outbreak of war in the Middle East—a meaningful move, though still limited in a longer historical context. However, she warned that equity valuations are higher than they were ahead of the 2022 energy shock and that the equity risk premium is close to zero. In what she described as a ‘binary’ risk environment, she argued that flexibility matters more than conviction—making ‘cash’ a practical advantage until uncertainty clears and investors can redeploy capital with better visibility.

For now, the session’s cross-asset message was stark: oil remains the volatility engine, but the market’s defensive bid is increasingly showing up in Bitcoin (BTC), gold, and long-duration Treasuries—and the next decisive move will likely depend less on technicals than on whether diplomacy can credibly alter the conflict’s trajectory.

🔎 Market Interpretation

- Cross-asset split: Oil saw extreme intraday swings, but broader risk markets (U.S. equities and Treasuries) did not mechanically follow crude’s late rebound, suggesting positioning/technicals outweighed single-headline energy moves.

- Geopolitics as the main volatility vector: Reports Iran rejected a U.S. ceasefire proposal and subsequent escalation rhetoric kept a geopolitical risk premium embedded in energy and volatility pricing.

- Defensive assets led: Bitcoin and gold strengthened as “hard” hedges, while long-duration Treasuries rallied (yields down), signaling demand for protection against both conflict escalation and growth uncertainty.

- Equity tape looked fragile: Stocks ended modestly higher but churned sideways after the open; the S&P 500 recorded another ≥1% intraday range day, indicating unstable market footing.

- Liquidity preference returned: The U.S. dollar dipped early but firmed into the close—consistent with a pattern of initial risk repricing followed by renewed demand for liquidity as headlines deteriorate.

- Macro backdrop remains uncomfortable: Hotter-than-expected U.S. import/export prices and falling inflation breakevens reinforced “sticky inflation vs slowing growth” concerns, limiting confidence in near-term rate cuts.

💡 Strategic Points

- Expect oil-driven volatility, not oil-led direction: Intraday crude spikes (down ~6–7% then back; peak near ~$90) can amplify volatility without reliably dictating equity/bond closes—risk frameworks should separate “volatility impulse” from “trend signal.”

- Hedging is rotating toward hard defensives: The session’s clearest defensive bid appeared in BTC, gold, and duration, implying investors may be diversifying hedges beyond USD-only or oil-only expressions.

- Watch prediction markets for regime shifts: Polymarket’s muted rise in ceasefire probability suggests traders are unwilling to fade the geopolitical premium—changes here could precede repricing in oil, vol, and risk assets.

- Positioning/flows matter more than conviction: Goldman noted lower volumes and high ETF share (~37%), pointing to flow-led price action—risks of sharp, non-fundamental swings remain elevated.

- Rates signal defensive duration demand: Falling 30Y (~-4 bps) and 2Y (~-2 bps) yields despite oil’s recovery indicates Treasuries are being used as a hedge against tail risks and growth downdrafts.

- Regional policy divergence: U.S. easing expectations stayed restrained, while U.K./euro zone pricing turned more dovish—relative rates could become a key driver of FX and global equity leadership.

- Valuation risk in a binary environment: With MSCI World down ~7% since the war began and equity risk premium near zero (per Goldman), “cash/flexibility” may be strategically valuable until conflict and inflation paths clarify.

- Key near-term catalysts to monitor:

- Credible diplomatic progress (or lack thereof) that changes the conflict trajectory

- Further strikes/headlines around critical infrastructure

- Inflation-linked data that shifts rate-cut probability

- Market internals: breadth, small-cap relative strength, and repeated wide intraday ranges

📘 Glossary

- WTI (West Texas Intermediate): A leading U.S. crude oil benchmark used in futures markets.

- Breakeven inflation: The inflation rate implied by the yield difference between nominal Treasuries and inflation-protected securities (TIPS); a market-based inflation expectation proxy.

- Duration: A measure of bond price sensitivity to interest-rate changes; “long duration” typically benefits most when yields fall.

- Risk-on / risk-off: Shifts in investor preference toward higher-risk assets (stocks, high beta) versus defensive assets (Treasuries, gold, cash).

- Technical resistance: A price level where an asset historically struggles to rise above, often influencing trader positioning and momentum.

- ETF tape activity: The share of total market trading volume attributable to exchange-traded funds, often associated with systematic or flow-driven moves.

- Equity risk premium (ERP): The extra return investors demand for holding equities over risk-free assets; a low/near-zero ERP implies limited compensation for equity risk.

- Macro volatility compression: A period where major macro variables (rates, FX, commodities) show reduced realized volatility, which can abruptly reverse during shocks.

- Prediction markets (e.g., Polymarket): Markets where prices reflect implied probabilities of real-world events, often used as a sentiment/probability gauge.

Comment 0