News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

FTX said it will begin its next round of creditor distributions on July 31, moving roughly $900 million in repayments as the collapsed exchange continues to unwind one of the largest failures in crypto history. The payment schedule matters for markets because each tranche can shift near-term liquidity—particularly if recipients choose to rotate recovered funds back into digital assets or, conversely, convert them to cash.

According to statements from the FTX Recovery Trust and FTX, this will be the company’s fifth creditor repayment. Eligible creditors are expected to receive funds within one to three business days through BitGo, Kraken, or Payoneer accounts. Under FTX’s restructuring plan, ‘convenience class’ claims below $50,000 are slated to receive 120% of allowed claim value, while other claims are expected to be paid at roughly 103% to 105%.

FTX filed for bankruptcy in November 2022. Since then, the FTX Recovery Trust has distributed about $10 billion, reflecting a recovery process aided by asset sales, cash management, and proceeds tied to the broader rebound in parts of the crypto market. Former CEO Sam Bankman-Fried was sentenced in 2024 to 25 years in prison; a recent appeal of his conviction and sentence was denied last month.

In parallel, traditional finance continues to broaden its product lineup for crypto exposure. T. Rowe Price launched an actively managed multi-token spot exchange-traded fund, T. Rowe Price ($TROW) confirmed in a product release cited by local reports. The ETF, trading on NYSE Arca under the ticker TKNZ, received U.S. Securities and Exchange Commission approval for listing and trading on June 12, 2026.

TKNZ is managed by Blue Macellari, head of digital assets at T. Rowe Price, and is designed to allow active weight adjustments based on market conditions such as trend shifts, momentum, and ‘sector rotation.’ As of July 17, the fund’s allocations were reported at 41.13% Bitcoin (BTC), 18.31% Ethereum (ETH), 11.12% BNB (BNB), 9.46% Solana (SOL), 9.42% XRP (XRP), and 6.14% Hyperliquid, with the six assets accounting for more than 95% of holdings. The structure underscores how quickly multi-asset crypto exposure is moving from passive single-coin products toward more portfolio-like approaches that resemble thematic equity funds.

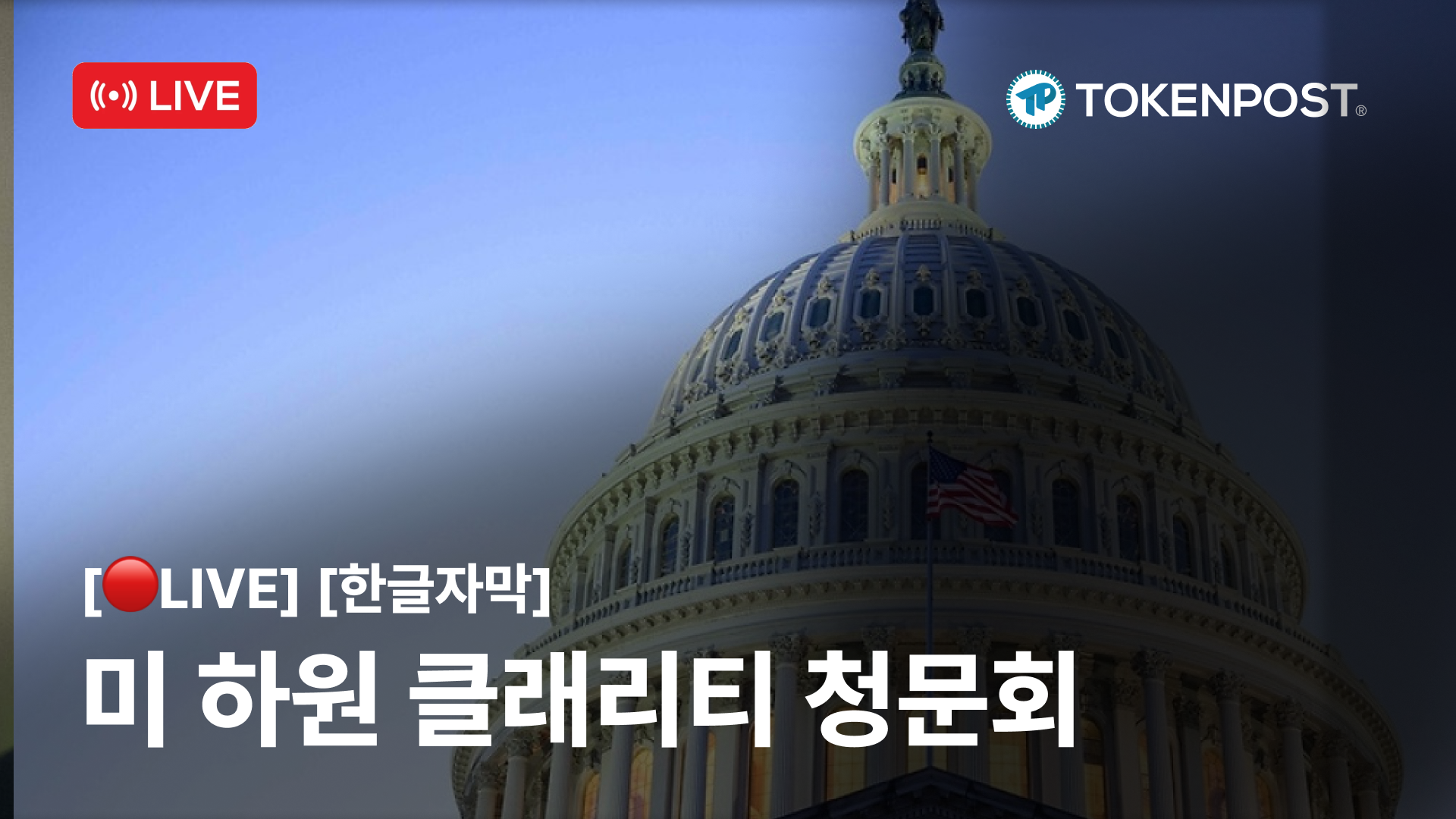

On the policy front, U.S. lawmakers are weighing steps that could further legitimize Bitcoin as a state-level reserve asset. Reports said the U.S. House of Representatives will discuss H.R. 8957, the “U.S. Reserve Modernization Act,” during an in-person hearing in New York tied to deliberations around the ‘Clarity Act’ framework for digital asset regulation. The proposal would enable the U.S. Treasury to acquire Bitcoin in a budget-neutral manner—without new taxpayer spending—while requiring periodic audits, secure custody standards, and public disclosure of government Bitcoin holdings. Supporters argue it could position Bitcoin alongside other long-term strategic reserves, although the measure remains at the discussion stage and faces political and implementation hurdles.

At the same time, Democrats are pushing for substantial changes to the broader U.S. crypto market structure bill, according to CNBC reporting cited by journalist Pete Rizzo. The reported objections center on ethics and governance, including the principle that elected officials should not profit from crypto—an argument that has included scrutiny of President Trump’s crypto-related revenue and potential conflicts of interest. The dispute adds another layer of uncertainty to the timeline for U.S. regulatory clarity, even as the industry presses for clearer rules around token classification, trading venues, and consumer protections.

In Europe, the European Central Bank is intensifying its messaging around stablecoins, warning that widespread adoption could erode commercial banks’ retail deposit base and reshape competition in the payments sector. ECB Executive Board member Piero Cipollone said large-scale stablecoin use could weaken the deposit-funded model that underpins much of the banking system. This week, the ECB selected 36 payment service providers—including banks, fintech firms, and payments companies—for a 12-month digital euro pilot. The pilot is scheduled to begin in the second half of 2027 and will test the operational feasibility of a retail central bank digital currency, with Cipollone arguing the digital euro could help preserve the role of public money while keeping banks engaged in the evolving payments ecosystem.

Legacy financial institutions are also building internal infrastructure for tokenized finance. Bank of America ($BAC) appointed Sonali Tyson as head of its global digital asset platform, tasking her with overseeing platform design, development, scaling, and governance, as well as integration with existing financial rails. The bank also named Adam Dixon to focus on tokenized deposits and stablecoins, digital collateral transfers, and crypto trading settlement and custody, while Kevin Milsom was appointed to lead AI transformation for the platform—signaling that major banks increasingly view digital assets and automation as linked strategic priorities.

Elsewhere, macro risk remained in focus after Iranian state media reported U.S. airstrikes in parts of Iran’s Hormozgan province early Friday local time, resulting in casualties and damage to infrastructure including bridges and a tunnel. Separately, Iranian outlets reported that the empty oil tanker Belma, while docked near Kharg Island—one of Iran’s key crude export hubs—was hit by two missiles attributed to U.S. forces. Any escalation around critical shipping and energy infrastructure can amplify volatility across oil and broader risk markets, which can spill over into crypto through changes in ‘risk appetite’ and dollar liquidity conditions.

On-chain flows also drew attention. Whale Alert flagged a transfer of 191,159,182 USD Coin (USDC) worth about $191.2 million from Aave to an unidentified whale wallet. Large stablecoin movements are often watched as a proxy for potential buying power, although market impact typically depends on whether funds subsequently move to exchanges or remain in self-custody.

Meanwhile, Solana-linked sell-side pressure remained a talking point as Pump.fun reportedly moved additional SOL to Kraken, continuing a pattern of monetizing fee revenue. On-chain analyst observations cited by local reporting estimated Pump.fun has sold a cumulative 4.812 million SOL since early 2024—about $812 million in total—at an average sale price near $168.7. The latest transfer reportedly involved 81,700 SOL as part of an additional $6.15 million cash-out, underscoring how application-level revenue extraction can become a persistent source of supply even during broader market uptrends.

As the week closes, the mix of bankruptcy-era payouts, expanding U.S. ETF product design, Washington’s regulatory bargaining, and Europe’s CBDC urgency highlights a market balancing renewed institutional access against persistent policy and macro uncertainty. The next FTX distribution round on July 31 will be monitored not just as a legal milestone, but as a real-time test of where recovered capital flows next.

🔎 Market Interpretation

- FTX repayments as a liquidity event: The July 31 creditor distribution (~$900M) is a near-term market catalyst because recipients may either re-enter crypto (supportive flows) or convert to fiat (potential sell/withdrawal pressure).

- Recovery progress reduces tail risk, but creates flow risk: With ~ $10B already distributed, the bankruptcy overhang is shifting from “will funds return?” to “where will funds rotate?”—a rotation dynamic that can move spot liquidity in BTC/ETH and majors.

- Institutional access is broadening beyond single-asset products: T. Rowe Price’s actively managed multi-token spot ETF signals a move toward portfolio-style crypto exposure (active weights, “sector rotation”), which can reinforce correlations across large-cap tokens and concentrate flows into index-like baskets.

- Regulatory headlines remain a two-sided volatility driver: Discussion of a Bitcoin reserve framework (H.R. 8957) is supportive in narrative terms, but partisan dispute over ethics/governance in market-structure legislation increases uncertainty on timing and final rules.

- Europe’s stablecoin caution + digital euro push: ECB warnings frame stablecoins as a threat to bank deposits, while the 2027+ digital euro pilot aims to keep public money central in payments—potentially shaping EU stablecoin rules, custody standards, and bank participation.

- Macro/geopolitics can spill into crypto via risk appetite: Reports of U.S. strikes in Iran and incidents near oil infrastructure raise the odds of oil volatility and broader risk-off moves, which can tighten dollar liquidity and pressure crypto beta.

- On-chain signals mixed: A large USDC transfer from Aave to a whale wallet suggests potential deployable liquidity, but impact depends on whether funds hit exchanges. Separately, ongoing SOL sales linked to Pump.fun represent persistent supply that can cap rallies in SOL during uptrends.

💡 Strategic Points

- Watch July 31–early August for flow confirmation: Monitor exchange inflows/outflows around the FTX distribution window (BTC/ETH/stablecoins) to infer whether repayments are being redeployed into crypto or cashed out.

- Position for “rotation” behavior, not just direction: If recovered funds return to crypto, they may concentrate in highly liquid assets (BTC/ETH) first, then rotate to large-cap alts—especially as multi-asset products make basket exposure easier.

- ETF composition can influence relative performance: Track TKNZ weight changes and any copycat products; active rebalancing could amplify momentum (buy winners/sell laggards) and increase cross-asset correlation inside the large-cap complex.

- Policy optionality vs. implementation risk: A “budget-neutral” Treasury BTC acquisition proposal is supportive as a long-term narrative, but credibility hinges on custody/audit standards and political feasibility; treat headlines as volatility rather than certainty.

- EU payments regime divergence risk: ECB’s stance implies tighter scrutiny of stablecoins; projects relying on EU retail stablecoin growth should account for potential constraints on issuance, reserve structure, and distribution via banks/PSPs.

- SOL-specific supply overhang monitoring: Track known programmatic sellers (e.g., Pump.fun-related addresses) and exchange deposit patterns; sustained application-fee monetization can create recurring sell pressure independent of broader market direction.

- Stablecoin whale moves need a second signal: Treat large transfers as “potential energy” until confirmed by subsequent exchange deposits, DEX activity, or lending/borrowing changes (e.g., collateralization and leverage build).

📘 Glossary

- Creditor distribution: Court-approved repayment to creditors during bankruptcy restructuring; can create market-moving liquidity depending on recipients’ actions.

- Convenience class claim: A bankruptcy claim category (here, <$50,000) often handled with simplified treatment; in this plan targeted at 120% of allowed claim value.

- Allowed claim value: The officially recognized amount a creditor is entitled to receive under the restructuring plan.

- Spot ETF (multi-token): An exchange-traded fund holding the underlying assets directly (not futures), here across multiple cryptocurrencies with active reweighting.

- Sector rotation (crypto): Shifting allocations among token “sectors” (e.g., L1s, DeFi, payments) based on momentum/trends, similar to equity sector rotation strategies.

- Budget-neutral acquisition: Purchasing an asset (e.g., BTC) without increasing net taxpayer spending, typically via reallocations or offsetting receipts.

- Stablecoin: A token designed to maintain a stable value (often pegged to USD) backed by reserves; widely used for trading, payments, and on-chain settlement.

- CBDC / digital euro: Central bank digital currency; a retail digital euro would be a central-bank-issued payment instrument for the public.

- Tokenized deposits: Bank liabilities represented on a blockchain-like system, aiming to combine bank money with programmable settlement features.

- On-chain flows: Observable blockchain transactions used to infer behavior like accumulation/distribution, exchange deposits, or liquidity positioning.

Comment 0