News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

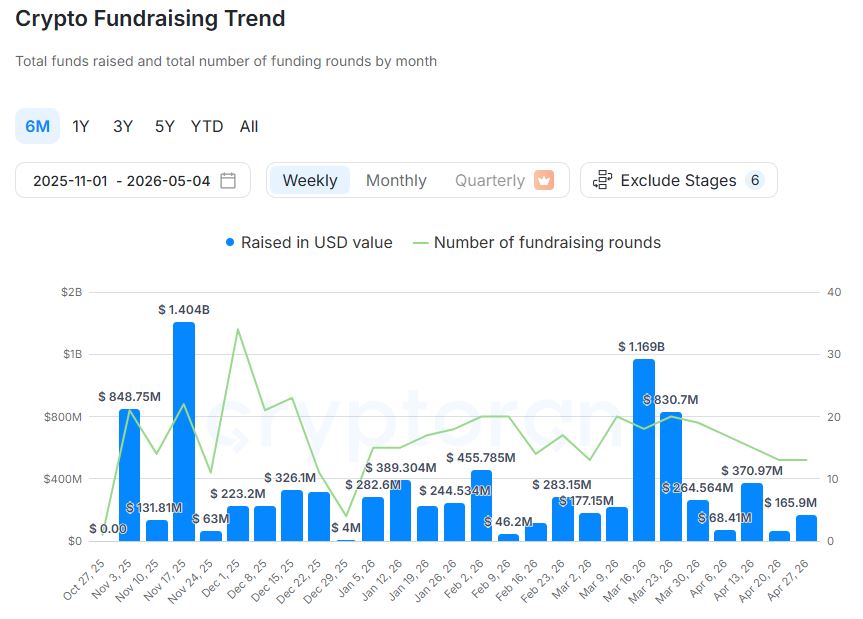

Crypto venture funding rebounded in the final week of April, with weekly deal value jumping to roughly $165.9 million—more than double the prior week—signaling a short-term recovery in 'liquidity inflow' even as broader activity indicators remain subdued.

Data compiled by CryptoRank shows that a total of 13 funding rounds closed between April 27 and May 3 UTC, raising about $165.9 million. While the number of deals was unchanged from the previous week (also 13 rounds), the total capital raised surged from $65.28 million, reflecting a sharp increase in average check sizes and the presence of several outsized transactions.

Among the week’s notable raises, fintech and infrastructure projects attracted fresh capital across seed, Series A, and strategic rounds. Velo secured $14 million in a Series A backed by Tether, while Squads raised $18 million in a strategic round led by Solana Ventures and other investors. Fence closed a $20 million Series A with participation from Galaxy. On the smaller end of the spectrum, Legend.trade raised $3.5 million in a seed round that included Electric Capital, and Kaisa Network collected $1 million in a pre-seed round.

Several deals also stood out for their scale and structure. Fun completed a $72 million Series A led by Multicoin Capital and other backers, providing the week’s largest disclosed venture round. M&A activity also contributed meaningfully to total weekly volume, including a $100 million acquisition involving MoonPay as well as a separate $43 million M&A transaction by AI Financial.

The weekly bounce comes against a backdrop of softer month-to-date and trailing-30-day metrics. CryptoRank’s figures show that April ended with 64 deals totaling about $662.46 million, down from March’s 84 deals and $2.6 billion. Earlier in the year, January recorded 66 rounds totaling $1.14 billion, followed by February’s 70 rounds and $894.34 million. So far in May, one round totaling $72 million has been recorded.

On a trailing 30-day basis, CryptoRank’s investment activity index fell 46% month-over-month to a 'Low' reading, suggesting that the latest weekly surge has not yet translated into sustained momentum. Over the same period, the number of rounds reached 65—down 39.8% from the prior month—while total capital raised was about $2 billion, a steep 73.6% decline. Average round sizes clustered in the $3 million to $10 million range, with seed-stage financings remaining the most active.

Sector allocation data points to continued investor preference for product rails and distribution channels rather than purely speculative plays. During the period referenced by CryptoRank, API-focused projects formed the core of funding concentration. Looking at the past six months, payments accounted for the largest share of investment at 32.58%, followed by decentralized exchanges (DEX) at 21.72%, real-world assets (RWA) at 19%, APIs at 14.03%, and perpetuals at 12.67%.

Investor participation remained led by large, repeat players. Coinbase Ventures was the most active with 29 deals, followed by GSR with 17 and Tether with 16. Animoca Brands logged 13 deals, while Castrum Capital recorded 12, YZi Labs 11, and Andreessen Horowitz’s a16z crypto 10.

While the late-April rebound suggests investors are still willing to deploy capital into select themes—particularly payments, APIs, and ecosystem infrastructure—the broader data indicates that risk appetite is cautious. For the market, the key signal going forward will be whether larger rounds and acquisitions continue to offset the ongoing decline in deal count, or whether the week’s spike proves to be a temporary burst in an otherwise cooling funding cycle.

Comment 0