News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Korbit Research Center, the research arm of South Korean crypto exchange Korbit, says the market for 'perpetual futures' is rapidly expanding beyond cryptoassets into 'real-world assets' (RWA)—a shift that is beginning to blur the line between offshore derivatives trading and traditional capital markets.

In a report released Thursday ET, titled Perpetual Futures: Beyond Crypto Markets to RWA, the center outlined how both centralized and decentralized venues have accelerated the listing and adoption of perpetual contracts tied to stock indices, individual equities, and even FX rates. Perpetual futures are derivative contracts designed to track an underlying asset price without an expiry date, typically relying on a 'funding rate' mechanism to keep prices anchored to spot markets.

According to the report, global centralized exchanges such as Binance have used offshore licensing structures and proprietary indices to list new perpetual products quickly, while decentralized perpetual exchanges—often referred to as 'perp DEXs'—have pushed listing authority into protocol-level governance. Korbit pointed to Hyperliquid as a leading example of this trend, arguing that the shift has materially increased the speed at which new RWA-linked contracts can be launched and traded.

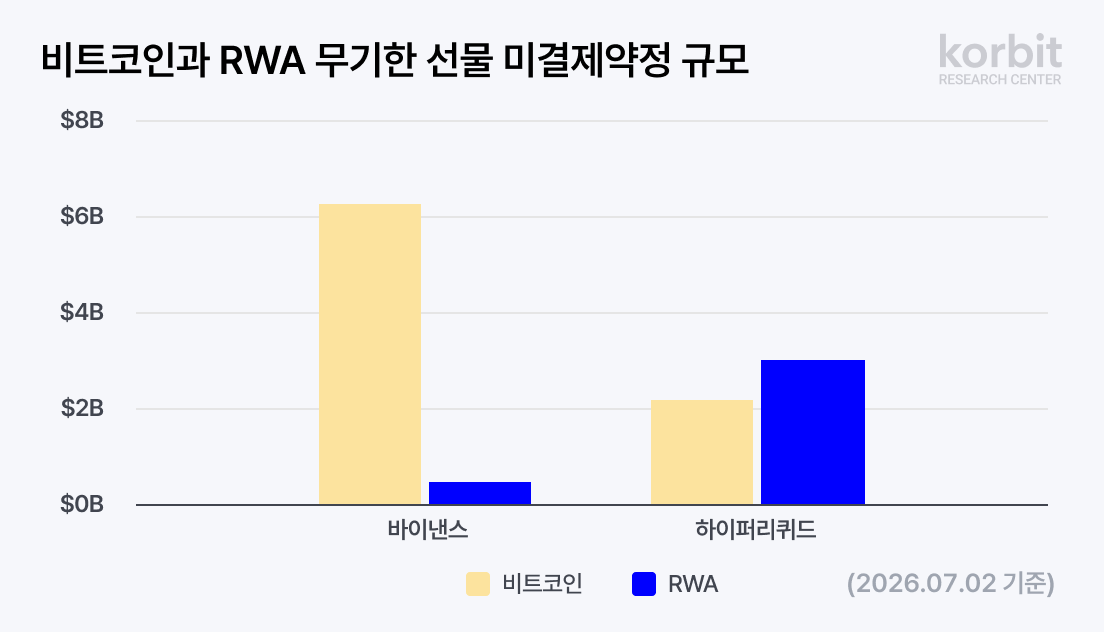

Korbit’s data highlights the scale of the move: as of July 2, open interest in Hyperliquid’s RWA perpetual futures reached roughly $2.9 billion, exceeding open interest in the venue’s Bitcoin (BTC) perpetual futures at about $2.1 billion. Open interest is a widely watched measure of derivatives positioning, reflecting the notional value of outstanding contracts and offering a proxy for market participation and leverage.

The report also tested how reliably these RWA perpetual products track their reference markets. Using publicly available data and its own verification methods, Korbit found that an S&P 500 perpetual closely replicated index and futures pricing during U.S. market hours with a correlation coefficient of 0.98—suggesting minimal distortion under normal trading conditions. In another case, a perpetual linked to SK hynix showed a high correlation of 0.97 to 0.99, and appeared to 'pre-price' the next day’s opening level during overnight hours when South Korea’s cash equity market was closed.

However, Korbit cautioned that price formation becomes more fragile when there is no credible spot reference. Perpetual contracts tied to private companies such as Cerebras and SpaceX, the report said, effectively generate their own prices within the exchange ecosystem due to the absence of observable spot-market transactions. That dynamic raises questions about how markets should interpret these instruments—particularly during volatility, low liquidity, or liquidation cascades.

To be included in a regulated perpetual futures framework, Korbit argued that an underlying asset would need several structural prerequisites: a continuous reference price, deep liquidity, real-time arbitrage pathways, and transparent pricing and liquidation systems. Without these pillars, the report suggested, markets can become vulnerable to pricing gaps and forced-liquidation events that do not reflect fundamentals.

The research comes as offshore perpetual markets increasingly list contracts referencing prominent Korean equities—including Samsung Electronics and SK hynix—allowing 24/7 trading outside local market hours. Korbit emphasized that this activity largely sits beyond the reach of South Korea’s Capital Markets Act, creating a regulatory blind spot when prices for domestic assets can be discovered, and potentially distorted, in venues not overseen by Korean authorities.

Korbit also noted the emergence of perpetuals linked to the won-to-dollar exchange rate, arguing that if dislocations or liquidation-related incidents occur in these offshore markets, domestic policy tools may have limited ability to respond. That concern, the report implied, is not only about investor protection but also about broader confidence in benchmark pricing for Korean-linked financial instruments.

“RWA perpetual futures are already operating at a multi-billion-dollar scale, and assets with robust reference-price infrastructure tended to show higher price reliability,” said Jiseong Jeong, a research fellow at Korbit Research Center. “With Korean assets being priced in places beyond the reach of domestic rules, it’s time to discuss how to monitor these markets and what contingencies are needed.”

The report underscores a broader industry shift: as perpetual futures expand into traditional asset classes, crypto-native derivatives infrastructure is increasingly intersecting with equities and FX—raising new questions about market integrity, cross-border supervision, and the future shape of '24/7' price discovery.

Comment 0