News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

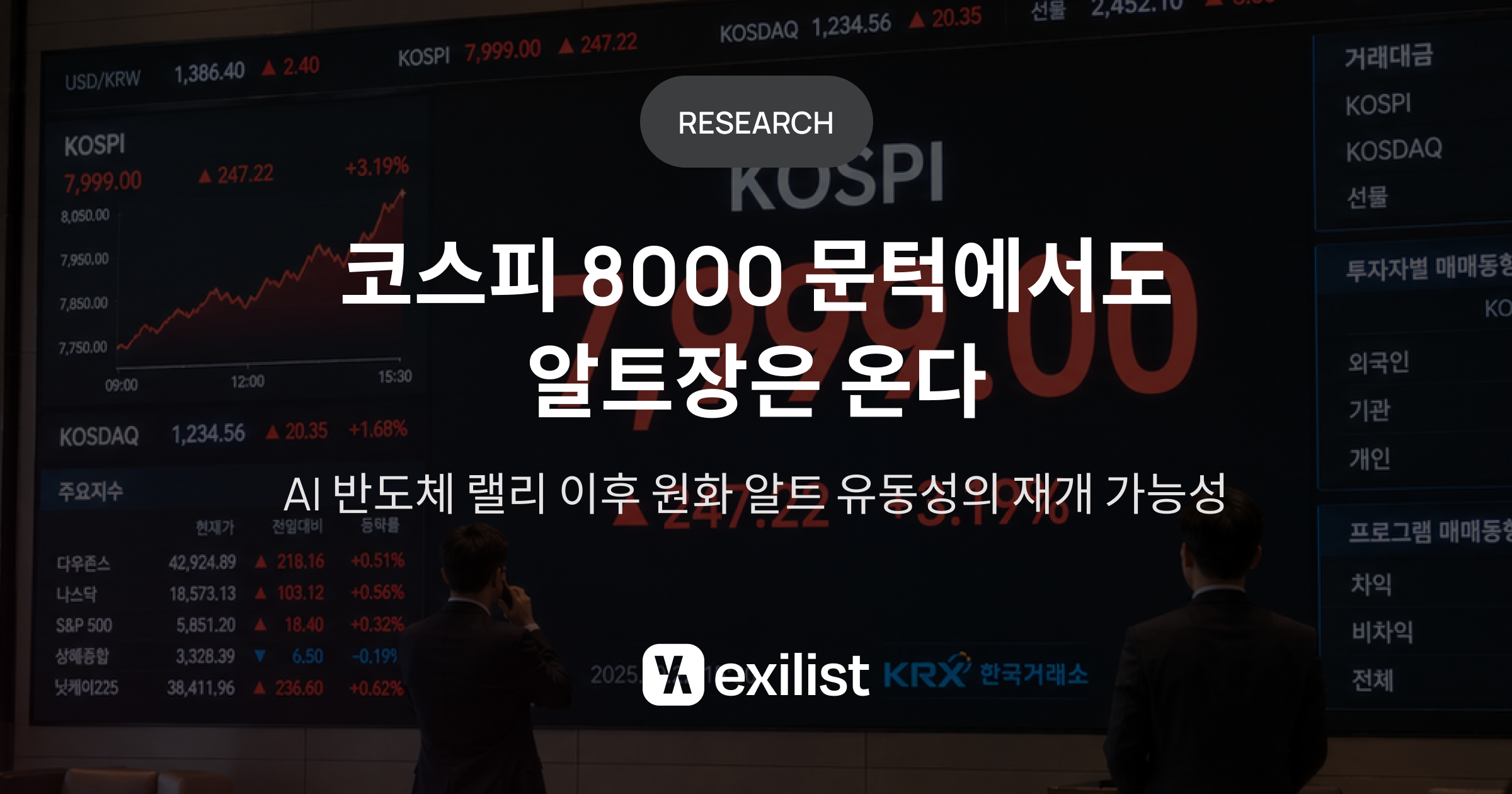

South Korea’s roaring equity rally toward a symbolic ‘KOSPI 8000’ is not necessarily bad news for crypto—at least not in the medium term. Research firm Exilist argues the stock surge has temporarily pulled liquidity away from digital assets, but may ultimately function as an early signal of recovering retail risk appetite that could later spill back into the country’s ‘KRW market’ and reignite an altcoin-led cycle.

In a report focused on May 2026, Exilist pointed to the KOSPI’s rapid climb toward the 8,000 level—driven largely by Samsung Electronics and SK hynix—as a defining backdrop. The rally has been underpinned by enthusiasm for generative AI, a global build-out of data centers, and rising demand for high-bandwidth memory (HBM), all of which revived earnings expectations and pulled Korean retail capital decisively into large-cap equities.

At first glance, that rotation looks like a headwind for crypto. Exilist, however, frames the move less as an exit from risk and more as a shift in where risk is being expressed—an important distinction in a market where retail flows often chase momentum across asset classes.

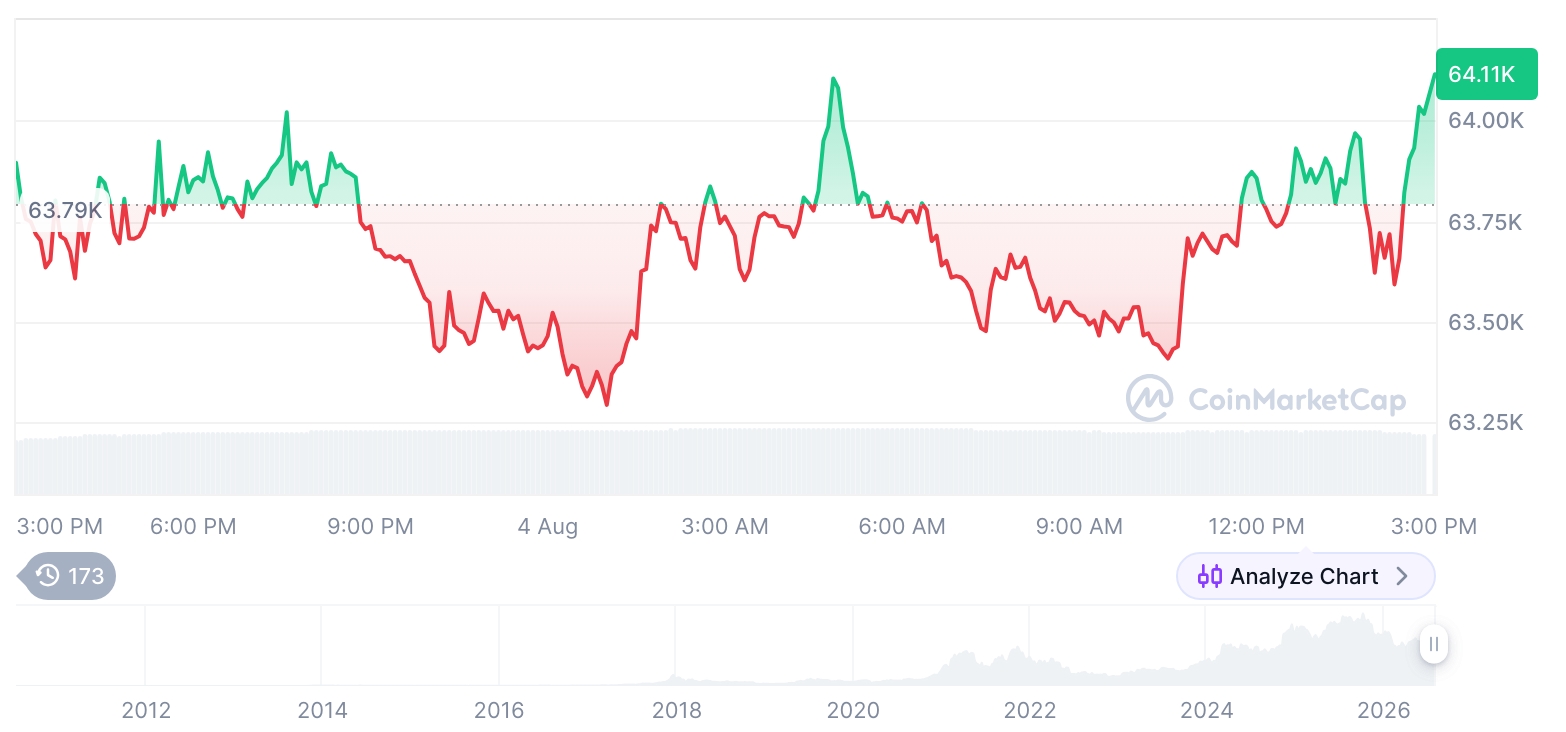

Globally, the data still does not resemble a classic ‘altseason.’ Bitcoin (BTC) has reclaimed the $80,000 level, and the total crypto market capitalization has hovered around $2.7 trillion, but capital remains concentrated in BTC. Bitcoin dominance has stayed near 60%, while widely followed ‘altseason’ indicators from platforms such as CoinMarketCap and BlockchainCenter have yet to reach levels typically associated with broad-based altcoin outperformance.

Exilist cautions against treating those readings as proof that an altcoin cycle is off the table. The report describes such indicators as inherently ‘lagging,’ noting that some of the most outsized returns tend to arrive before the metrics fully flip. It also argues that institutional capital tends to enter through the path of least friction—spot ETFs and mature custody—favoring BTC first and leaving altcoins to benefit later as risk tolerance expands.

Domestically, Exilist cites signs that the apparent slump in Korea’s crypto market may be more about reduced risk exposure than a full retreat. Citing local coverage of Bank of Korea data, the report notes that crypto holdings among users at the country’s five major exchanges fell from 121.8 trillion won (about $88.6 billion) in late January 2025 to 60.6 trillion won (about $44.1 billion) by late February 2026. Average daily trading value also dropped sharply over the same period.

Yet one pocket of behavior moved in the opposite direction: stablecoins. Exilist highlights that stablecoin holdings rose from roughly 88.5 billion won (about $64 million) in late July 2024 to 872.3 billion won (about $634 million) by late December 2025, and still stood at 607.1 billion won (about $441 million) at the end of February 2026. In other words, spot positions may have been cut, but ‘dollar-linked dry powder’ appears to remain on the sidelines.

Separate data cited in the report also suggest the domestic market is in a ‘waiting mode’ rather than an outright exodus. According to an industry survey by South Korea’s Financial Services Commission and the Korea Financial Intelligence Unit (FIU), KRW deposits at exchanges were estimated at around 8.1 trillion won (about $5.9 billion) at the end of 2025 even as trading volumes cooled. The number of accounts eligible to trade reportedly rose to 11.13 million, reinforcing the idea that participation infrastructure is intact even when speculative intensity fades.

Exilist argues the state of Korea’s ‘KRW market’ matters disproportionately for altcoins because of the country’s unique microstructure. Citing Kaiko data, the report notes that the Korean won remains a top-tier fiat currency for centralized exchange trading volume globally, with activity heavily concentrated on Upbit and Bithumb. Crucially, much of that activity is skewed toward altcoins rather than Bitcoin, making the KRW market a structural amplifier for altcoin price moves when retail liquidity returns.

Additional support comes from TRM Labs data on global retail crypto activity in Q1 2026. Exilist says South Korea ranked roughly second globally behind the United States by retail trading volume, maintaining a high standing even as worldwide activity cooled. The report also points to diverging exchange trends: while Coinone and Korbit reportedly saw sharp volume declines, Upbit’s volume increased and Bithumb’s drop was more limited—suggesting that remaining liquidity is becoming more ‘compressed’ into the two dominant KRW venues. From Exilist’s perspective, a recovery in KRW trading volume on Upbit and Bithumb is the most actionable signal to watch for a renewed altcoin cycle.

Rather than positioning the KOSPI rally as the enemy of altcoins, Exilist places it earlier in a behavioral chain. The report argues that if late-arriving retail investors chase AI-linked mega caps near the top and then face drawdowns during a correction, some may pivot toward higher-beta exposures—first into speculative small-cap themes and potentially into KRW-denominated altcoins. Exilist links this pathway to behavioral finance’s ‘prospect theory,’ which suggests investors who are in losses can become risk-seeking as they attempt to recover.

On narrative catalysts, the report identifies AI-related tokens, real-world assets (RWA), and tokenized stocks as particularly resonant themes for Korean retail. Exilist’s reasoning is that the public has already internalized a simple story—“AI growth benefits semiconductors”—and that the same mental model could extend to “AI growth benefits AI infrastructure, data, and agent-related tokens.” In altcoin cycles, the report contends, broadly understandable narratives often reach price discovery faster than nuanced technical differentiation.

Tokenized stocks are framed as another intuitive bridge. Korean retail investors already trade domestic equities, U.S. equities, and 24/7 crypto markets; combining those experiences into an on-chain wrapper could prove compelling. Exilist points to projects such as Ondo (ONDO) as examples tied to this trend, while warning that investors must distinguish among ownership structures, redemption mechanics, dividend handling, and jurisdictional regulation—areas where tokenized products can differ materially from traditional securities.

Regulatory developments abroad could also reduce the ‘discount rate’ applied to large, infrastructure-oriented altcoins, according to Exilist. The report argues that U.S. moves toward stablecoin legislation and discussions around digital asset market structure may not be uniformly positive for every token, but can lower uncertainty for major networks if markets begin to perceive a reduced risk of sudden securities classification. In that scenario, a post-Bitcoin rotation could broaden toward assets such as Ethereum (ETH), Solana (SOL), and XRP (XRP).

For Korean traders, taxation is another timeline catalyst. Under current rules, taxation on crypto income is scheduled to apply to transfers and lending from Jan. 1, 2027, making 2026 effectively the last full year viewed as pre-tax. Exilist argues that this could act as a form of time pressure that encourages higher-beta positioning—particularly if a large-cap equity pullback coincides with the window.

Beyond retail flows, Exilist points to signs of sustained long-term capital in crypto infrastructure. The report cites Andreessen Horowitz’s (a16z crypto) formation of a new $2.2 billion fund in 2026 as evidence that institutional conviction in foundational layers remains even during periods of muted trading. It also notes that RWA tokenization has expanded into the multi-billion-dollar range across multiple chains, suggesting that any altcoin rebound this cycle may rest on a broader base than simple exchange listing momentum.

Exilist ultimately outlines a staged roadmap: ‘Bitcoin leads’ → AI semiconductor rally fuels Korean retail FOMO → mega-cap correction → search for higher beta → recovery in major alts → ‘KRW market’ re-ignition → sharp moves in low-liquidity microcaps. A key point is that explosive ‘junk coin’ rallies are viewed as a late-cycle confirmation, not the starting gun. The more meaningful early markers, the report argues, would be a strengthening of major altcoins and a clear uptick in KRW-market trading volumes.

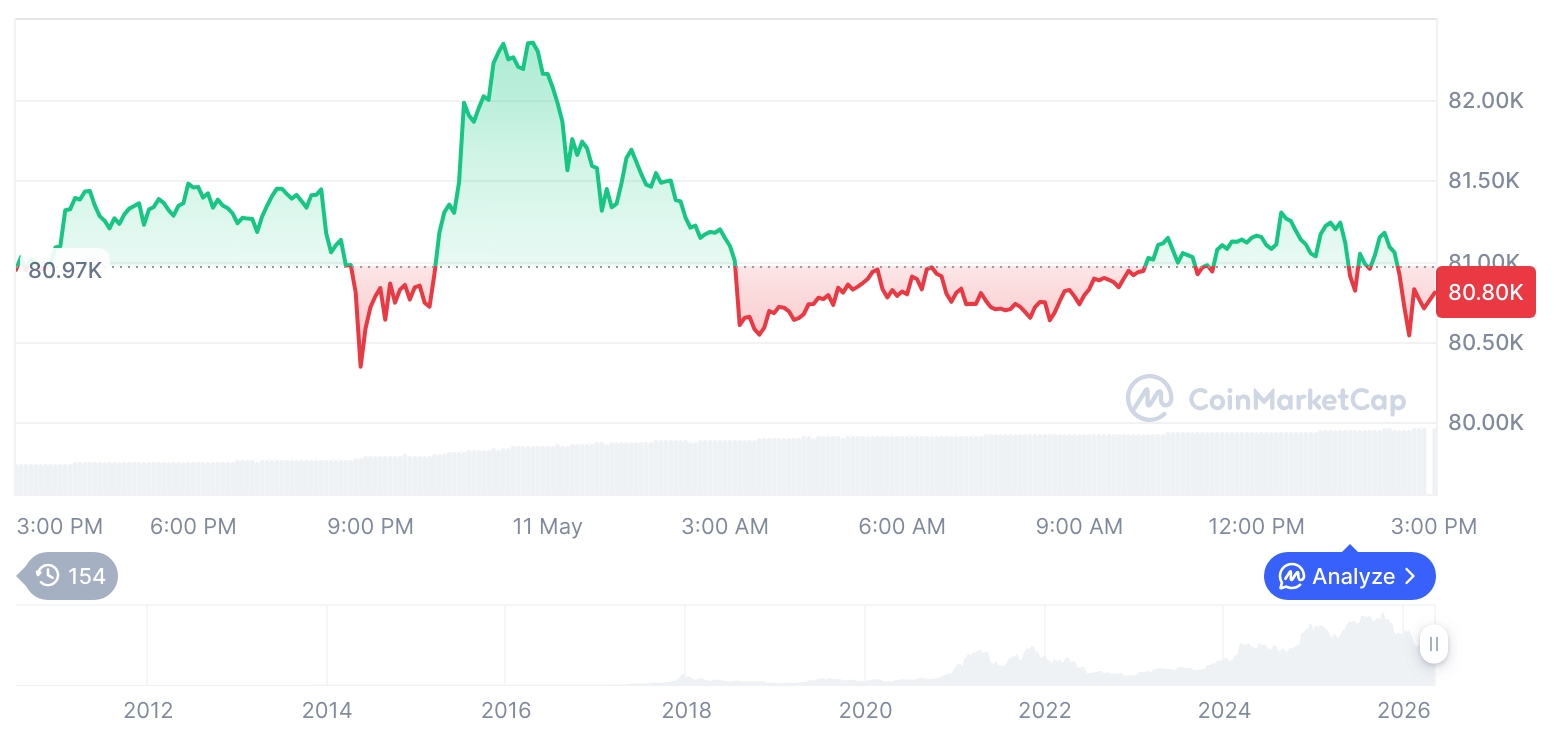

Risks remain significant. Exilist warns that if Bitcoin fails to hold support around $80,000 and sells off, any liquidity handoff into altcoins could be delayed. A longer-than-expected equity boom could also keep capital anchored in stocks. The report also cautions against treating stablecoin supply and balances as immediately deployable altcoin buying power, and notes that regulatory clarity can be a double-edged sword—reducing uncertainty for some assets while restricting others.

Still, Exilist’s central conclusion is that the next altcoin upswing—if it materializes—may not be driven solely by global liquidity, but by Korea-specific retail profit-and-loss dynamics and the reawakening of risk appetite signaled by the equity surge. In that framing, ‘KOSPI 8000’ and the AI semiconductor rally are less a competing trade than a potential precursor to the next rotation—one that could once again elevate South Korea’s KRW market as a key arena for altcoin price action.

🔎 Market Interpretation

- KOSPI surge as “risk-on barometer,” not anti-crypto: Exilist argues Korea’s push toward a symbolic KOSPI 8000 has temporarily diverted retail liquidity into mega-cap equities (Samsung, SK hynix), but may signal rebuilding risk appetite that often rotates across assets and can later return to crypto.

- Global crypto still BTC-led: BTC reclaiming $80,000 and total cap near $2.7T hasn’t produced a classic altseason; BTC dominance ~60% and popular altseason indicators remain muted. Exilist emphasizes these metrics are lagging and may confirm moves after early alt outperformance begins.

- Korea crypto “cooling” looks like de-risking, not abandonment: Exchange user crypto holdings fell sharply (per Bank of Korea-cited data), and trading values dropped—consistent with reduced exposure during an equity momentum phase.

- Stablecoin balances imply sidelined purchasing power: KRW-denominated stablecoin holdings rose materially into late 2025 and remained elevated into Feb 2026, suggesting dry powder is parked even if spot alt exposure was reduced.

- KRW market is structurally important for altcoins: The won is a top-tier fiat by CEX volume, with activity concentrated on Upbit and Bithumb and skewed toward altcoin trading. When Korean retail returns, KRW venues can amplify alt moves, especially in lower-liquidity names.

- Behavioral pathway highlighted: Exilist links a potential post-mega-cap correction rotation into higher beta (including alts) to prospect theory—loss-averse investors may become risk-seeking while trying to recover drawdowns.

💡 Strategic Points

- Primary early signal to watch: A sustained rebound in KRW trading volume—especially on Upbit and Bithumb—is framed as the most actionable confirmation of a Korea-led alt rotation.

- Sequence/roadmap (staged cycle): “Bitcoin leads → AI semiconductor equity FOMO in Korea → mega-cap correction → hunt for higher beta → recovery in major alts (ETH/SOL/XRP) → KRW market re-ignition → late-cycle microcap spikes.” “Junk coin” pumps are treated as late confirmation, not the start.

- Positioning implication: If rotation occurs, Exilist expects it to start with large, liquid alt infrastructure before flowing into smaller caps—consistent with how institutional capital enters (ETFs/custody-favored BTC first, then broader risk).

- Narratives likely to resonate with Korean retail:

- AI tokens (infrastructure/data/agent themes) as an intuitive extension of “AI → semiconductors.”

- RWA/tokenization as adoption expands into multi-billion-dollar scale across chains.

- Tokenized stocks as a bridge between equity trading habits and 24/7 crypto markets; requires diligence on ownership, redemption, dividends, and jurisdiction.

- Policy/timeline catalyst (Korea taxes): With crypto taxation on certain activities slated from Jan 1, 2027, Exilist flags 2026 as a perceived “last pre-tax year” that could pull risk-taking forward if market conditions align.

- Regulatory risk premium: Potential U.S. progress on stablecoin legislation/market structure could lower perceived classification risk for major networks—supporting a post-BTC broadening—though benefits won’t be uniform across tokens.

- Key risks:

- BTC breakdown below ~$80K could delay any alt handoff.

- Prolonged equity boom could keep retail capital anchored in stocks longer than expected.

- Stablecoins aren’t guaranteed buyers (balances may be hedges, transfer capital, or inactive).

- Regulatory clarity can cut both ways (some assets helped, others restricted).

📘 Glossary

- KOSPI: South Korea’s main stock index; “KOSPI 8000” is used here as a symbolic milestone for a powerful equity rally.

- KRW market: Crypto trading pairs quoted in Korean won (KRW), primarily on Korean exchanges; often more altcoin-heavy than USD markets.

- Altseason: A period when altcoins broadly outperform Bitcoin; often tracked with indices/indicators that can be lagging.

- Bitcoin dominance: BTC’s share of total crypto market capitalization; higher dominance usually implies capital concentration in BTC over alts.

- Rotation: Investor capital shifting between asset classes or sectors (e.g., equities → majors → altcoins) as momentum and risk appetite change.

- HBM (High-Bandwidth Memory): Advanced memory used in AI and data-center workloads; a driver of Korea’s semiconductor-led equity rally.

- Stablecoins: Tokens designed to track fiat value (often USD); described here as “dry powder” when parked for future deployment.

- RWA (Real-World Assets): Tokenized representations of off-chain assets (e.g., treasuries, credit, commodities) on blockchain rails.

- Tokenized stocks: On-chain products referencing equities; terms vary by structure (beneficial ownership vs. derivative exposure, redemption rights, dividends, and regulatory treatment).

- Prospect theory: Behavioral finance concept that people may take greater risks to recover losses than to achieve gains, potentially fueling higher-beta pivots.

- Higher beta: Assets that typically move more than the market (higher volatility); often sought after during speculative phases.

- Spot ETF: Exchange-traded fund holding the underlying asset (e.g., BTC), often serving as a lower-friction on-ramp for institutions.

Comment 0