News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

As expectations for imminent rate cuts fade, crypto markets are being forced to navigate a tougher reality: not just slower growth, but a shrinking margin for policymakers to loosen financial conditions. Yet amid that macro tension, Bitcoin (BTC), tokenization, and stablecoins are moving faster into regulated finance—suggesting that institutional integration can accelerate even when monetary relief does not.

In a recent note, Exilist Research pointed to the International Monetary Fund’s baseline outlook and the U.S. Federal Reserve’s April Beige Book as evidence that renewed supply-side shocks are narrowing central banks’ options. The IMF, in its April spring meetings, projected global growth could slow to 3.1% this year while headline inflation may climb as high as 4.4%, even under a scenario where energy prices rise 19% in 2026. Exilist argued the implication is structural: inflation risks driven by supply pressures can constrain easing even when growth cools.

The Fed’s Beige Book conveyed a similar tension. While eight of the 12 regional Federal Reserve Banks described economic activity as “slight to modest” expansion, it also noted that Middle East conflict risks and tariff changes are complicating hiring and investment decisions, leaving many businesses in a wait-and-see posture. Exilist interpreted the message as a shift toward corporate defensiveness rather than an imminent recession signal—an important distinction for markets still trying to price the timing of policy pivots.

Resilience in the U.S. and China, rather than comforting investors, has arguably become part of the problem. U.S. March retail sales rose 1.7% month over month, but the increase was widely seen as partly reflecting higher gasoline prices pushing up nominal spending. That dynamic—consumption that looks strong but is boosted by rising costs—weakens the case for the Fed to cut quickly. China, meanwhile, posted 5.0% year-on-year GDP growth in the first quarter and held its loan prime rate (LPR) steady for an 11th consecutive month in April, signaling that while property-sector and demand challenges persist, policymakers do not yet feel compelled to unleash major stimulus. Together, the two largest economies not rolling over sharply extends the market’s uncomfortable narrative: higher discount rates could persist longer than hoped.

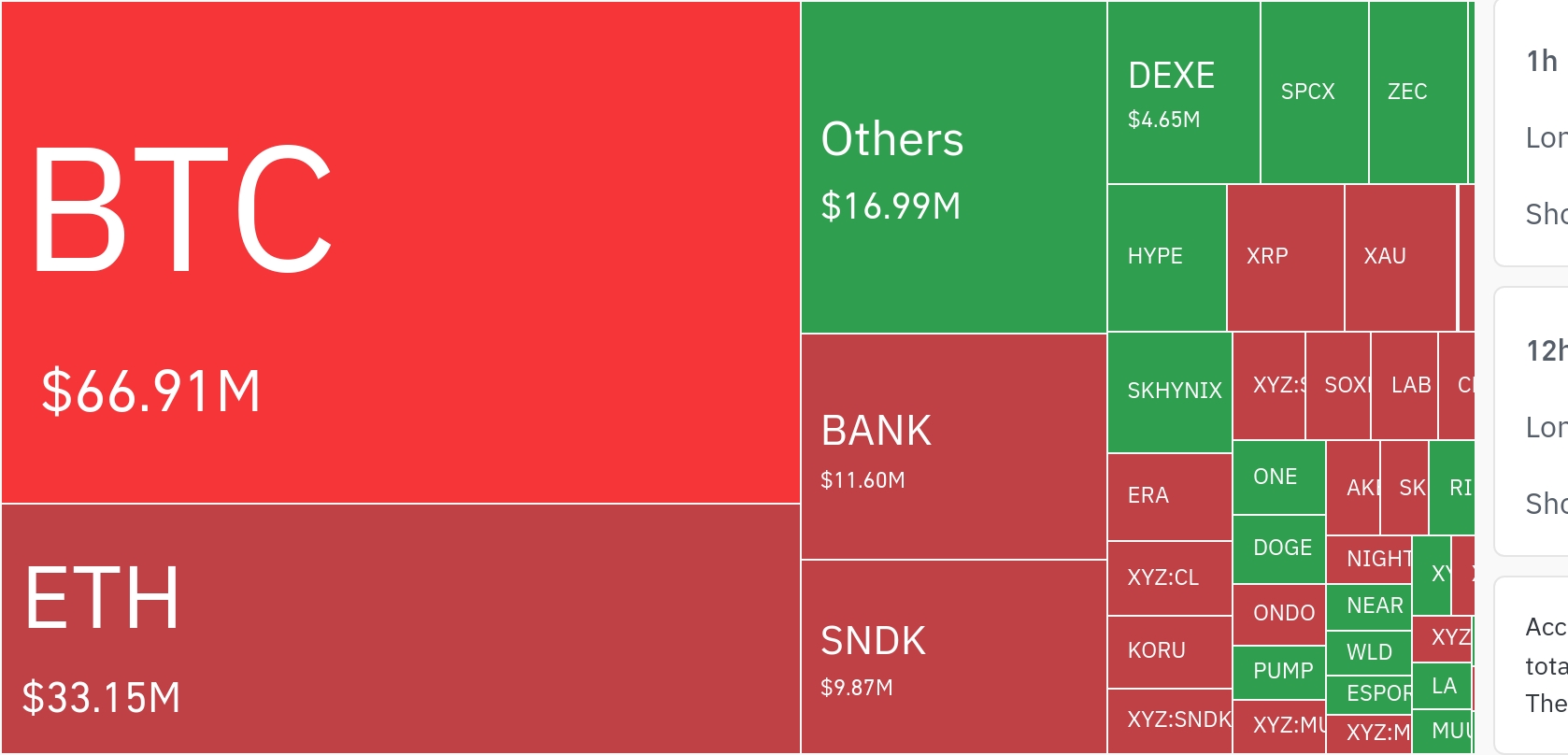

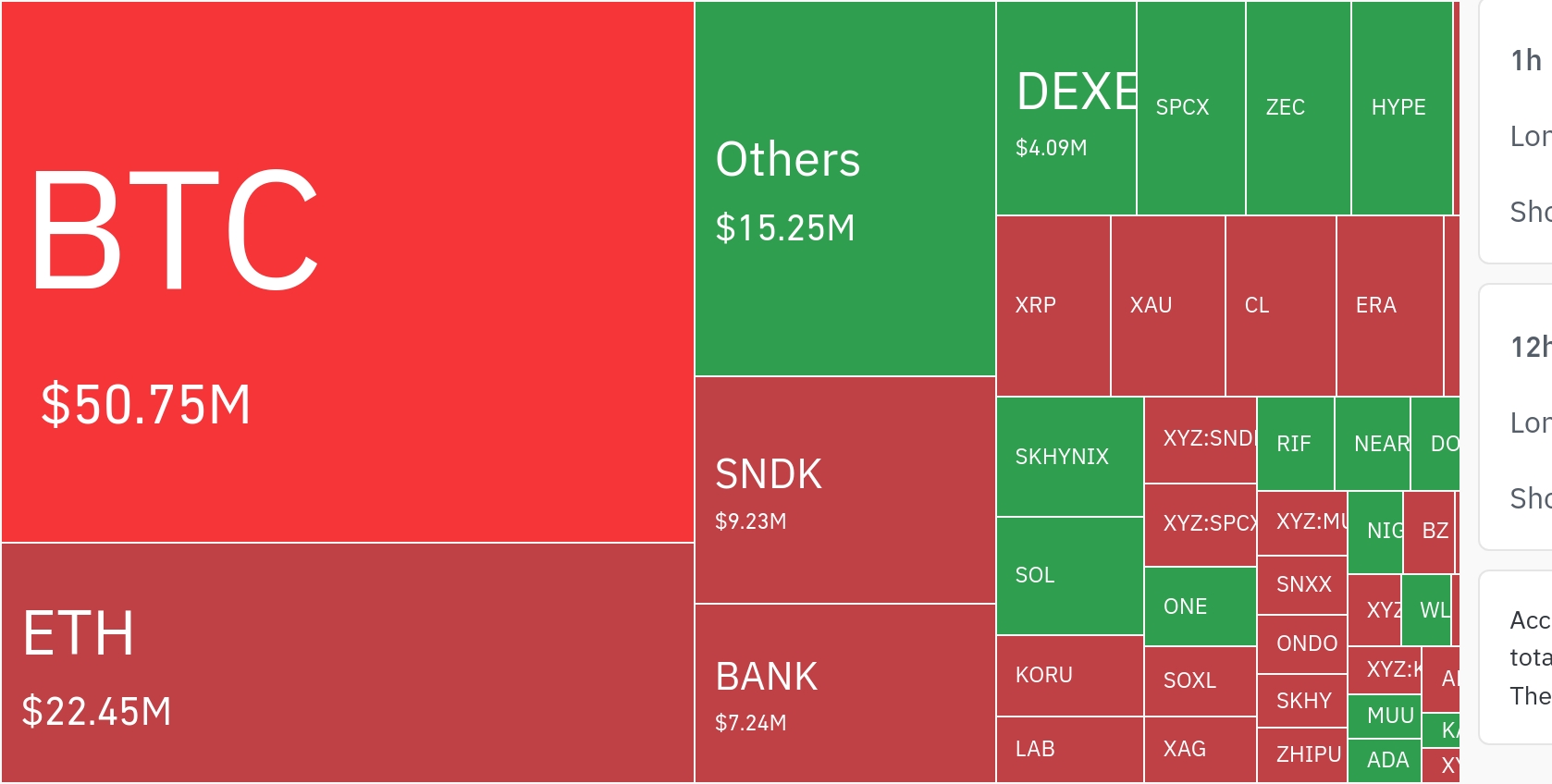

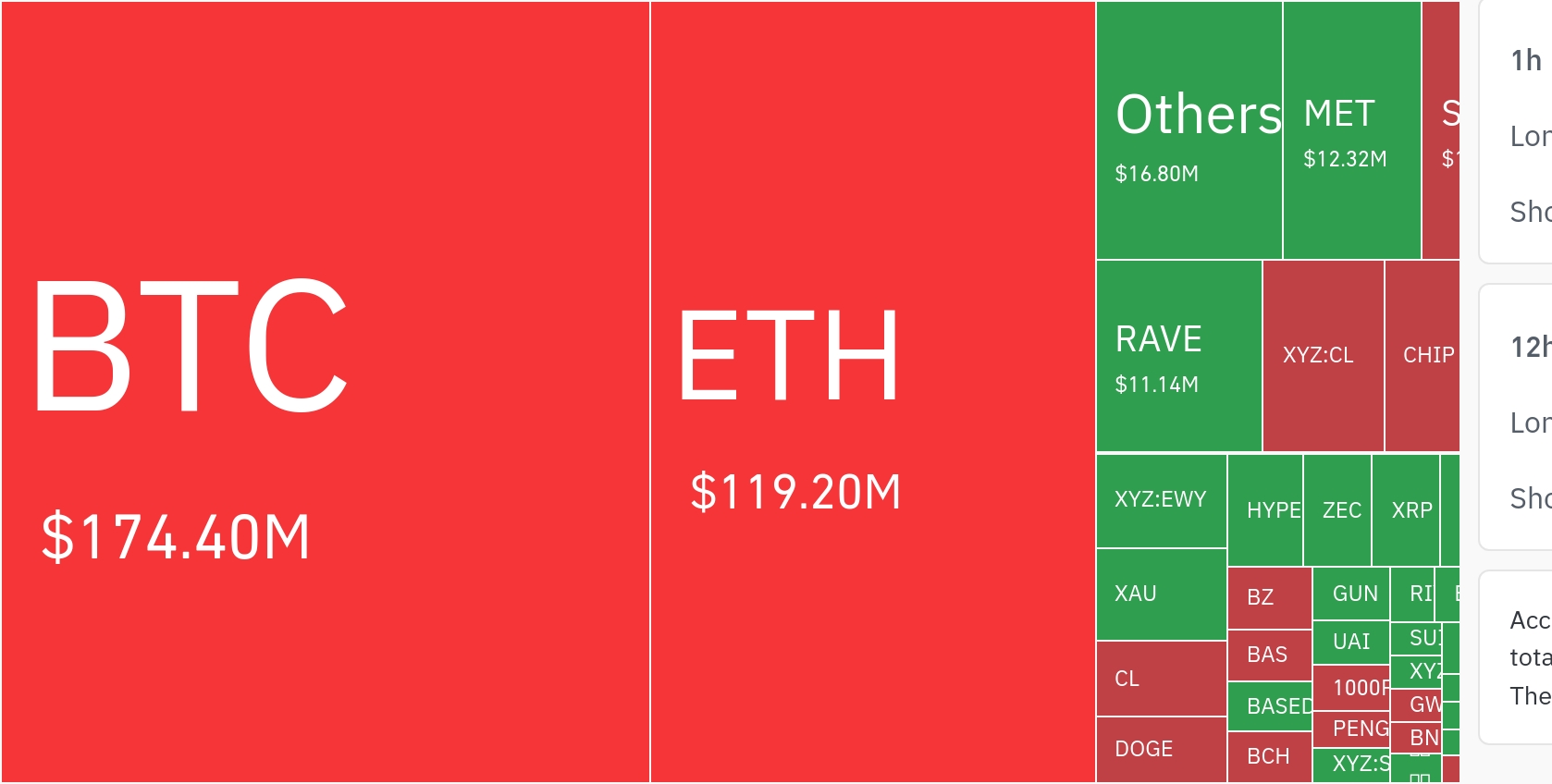

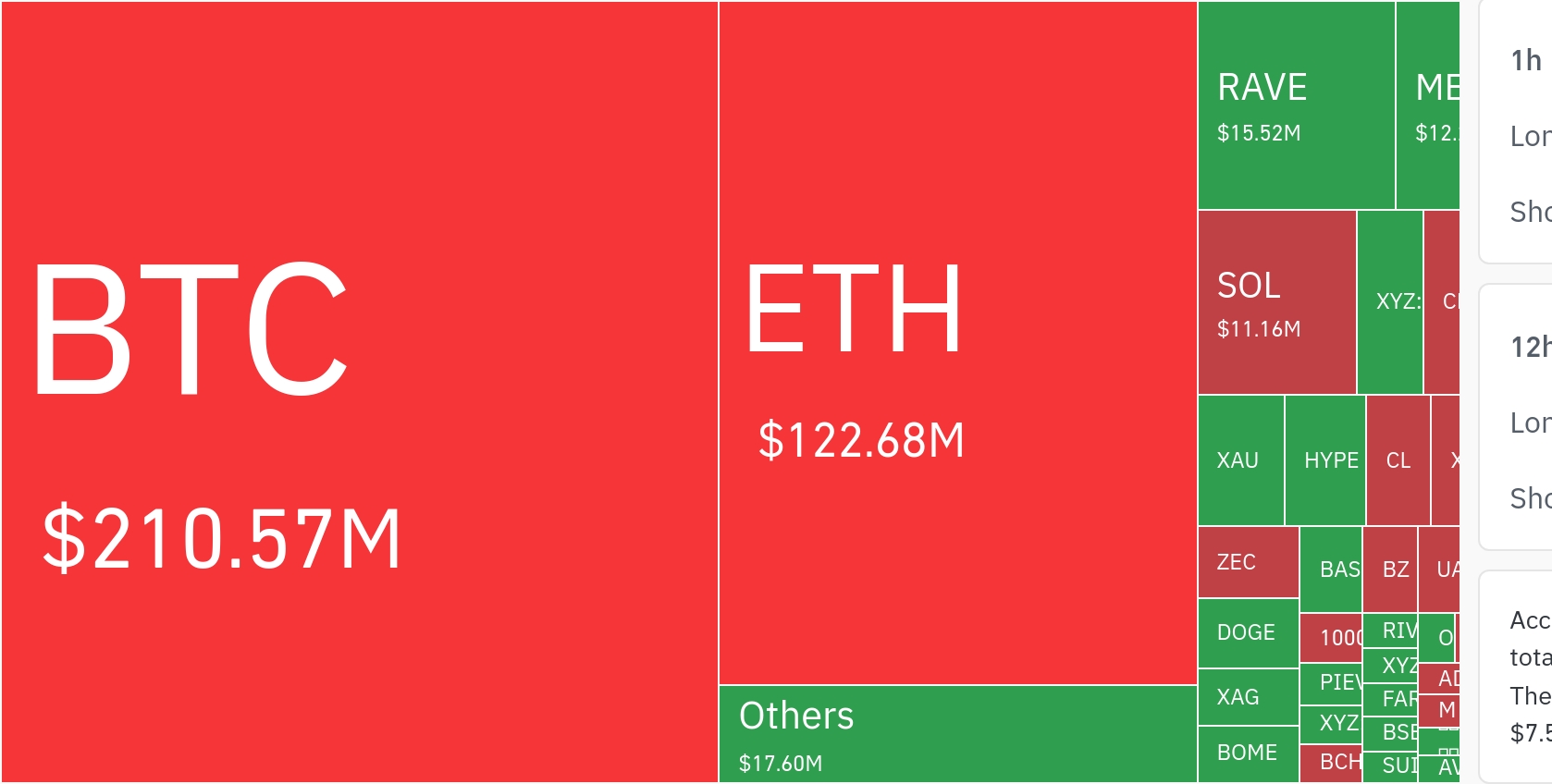

Against that backdrop, Bitcoin’s rebound this week carried a clear message about what is driving the bid. On Tuesday UTC (April 22), Bitcoin rose about 2.5% to around $77,600 amid improved risk sentiment linked to expectations of an extended ceasefire and eased concerns over energy-driven stress. Exilist noted the move looked less like a pure safe-haven rally and more like BTC acting as a ‘high-beta’ risk asset—one that tends to respond quickly when oil pressure moderates and the U.S. dollar’s advance pauses. Still, the firm emphasized that even if markets have not fully reclassified Bitcoin as a defensive asset, structural demand is increasingly reinforcing downside support.

That support has been visibly institutional. U.S. spot Bitcoin ETFs recorded net inflows of roughly $186.1 million on April 15, $26.1 million on April 16, $663.9 million on April 17, and $238.4 million on April 20—about $1.1145 billion across four disclosed sessions, according to figures cited by Exilist. Separately, CoinShares reported weekly inflows of $1.4 billion into digital asset investment products, marking the third consecutive week of net inflows and the strongest weekly pace since January. Exilist concluded the rebound appeared driven more by sustained ‘institutional spot demand’ than by simple short covering.

Corporate treasury buying has added another layer to the supply story. Strategy, the company formerly known as MicroStrategy, disclosed in an April 20 Form 8-K that it purchased an additional 34,164 BTC, lifting total holdings to 815,061 BTC. Exilist framed the distinction succinctly: ETFs provide a public-market channel for capital to enter BTC exposure, while corporate treasury accumulation can effectively lock circulating supply into longer-term holdings. With signs that large-holder net selling has eased, the overall supply-demand setup appears healthier than during the prior drawdown.

Regulation, too, is shifting from the question of whether crypto belongs in finance to the more operational question of how on-chain market structure should work. In the U.S., Securities and Exchange Commission (SEC) Chair Paul Atkins said on April 21 that he would propose an ‘innovation exemption’ framework that could allow tokenized securities to begin trading on-chain within defined constraints. The significance, Exilist argued, is that policymakers are moving from treating digital assets as an exception to designing how parts of capital markets can be ported onto blockchains. That shift could concentrate benefits toward market-structure-adjacent firms—broker-dealers, alternative trading systems (ATS), custodians, and tokenized securities infrastructure—rather than purely retail-facing exchanges.

The Commodity Futures Trading Commission (CFTC) signaled a parallel posture. Commissioner Michael Selig said rulemaking would not be delayed even as the agency operates with limited staffing at the top, while stressing ‘zero tolerance’ for fraud, manipulation, and insider trading. For the industry, Exilist noted, the key is not the absence of enforcement but clarity—what is permitted, what is prohibited, and under which supervisory regime.

Tokenization is also evolving from issuance experiments to competition over secondary-market plumbing. Hong Kong’s Securities and Futures Commission (SFC) on April 20 released a framework allowing secondary trading of authorized tokenized investment products, initially enabling authorized open-ended funds to be traded on regulated virtual asset trading platforms. The pivot matters because secondary trading forces the hard questions of market design—distribution, price discovery, and investor access—rather than one-off issuance mechanics.

In the same jurisdiction, crypto asset management narratives are developing beyond corporate treasuries. Bitfire said it acquired Avenir Group’s investment team and trading system for $1.6 million and aims to scale its regulated Bitcoin strategy, ‘Alpha BTC’, with a target of attracting more than 10,000 BTC of external capital within a year. The message is that competition is increasingly about regulated portfolio construction and risk management—not simply who can accumulate the most BTC.

Stablecoins, meanwhile, are stretching beyond payments into the realm of currency competition and corporate finance strategy. Circle ($CRCL) CEO Jeremy Allaire recently argued that yuan-denominated stablecoins represent a major opportunity, describing stablecoins as a technology that can “export” currency through global payment rails. He suggested China could introduce a yuan-based stablecoin within three to five years and projected that USD Coin (USDC) supply could rise 72% to $75.3 billion by the end of 2025. Whether or not the timeline proves accurate, Exilist highlighted the deeper shift: the industry is increasingly framing stablecoins not as internal crypto liquidity, but as instruments in cross-border monetary influence.

Public-sector voices are signaling similar concerns. Bank for International Settlements (BIS) General Manager Pablo Hernández de Cos warned that some stablecoins can behave more like an ETF than money due to redemption frictions, and said the absence of international coordination could deepen market fragmentation and regulatory arbitrage. In Europe, French Finance Minister Roland Lescure has called attention to the small scale of euro-denominated stablecoins, urging expanded development of tokenized deposits and euro stablecoins—an indication that jurisdictions are now debating reserves, redemption design, and the extension of currency zones rather than simply “adoption.”

Private infrastructure is also adapting. Tether participated on April 15 in a $134 million funding round for publicly listed company SDEV, linking the stablecoin economy more directly to public-market capital formation. Fireblocks, for its part, launched a feature enabling institutional clients to deploy stablecoin balances on its platform into on-chain lending markets to pursue yield—another sign that stablecoins are increasingly treated as instruments for treasury management, collateralization, and structured capital markets products.

South Korea is experiencing both the upside and the strain of these crosscurrents. From April 1 to April 20, the country’s exports rose 49.4% year over year to $50.4 billion, while imports totaled $39.9 billion, producing a $10.4 billion trade surplus. Korean equities have also recovered in April following a sharp March sell-off as foreign inflows returned, with global capital again concentrating around the AI semiconductor and memory value chain. The rebound has been driven less by easy liquidity and more by renewed conviction in tangible earnings and capex visibility.

But the pressures are equally clear. Bank of Korea Governor Rhee Chang-yong, on his first day in office, signaled a cautious stance on monetary policy while setting broader priorities involving won internationalization, digital innovation in payments, and macroprudential balance. Around the same time, South Korean and U.S. finance authorities publicly noted that excessive won volatility is undesirable—underscoring that the policy debate extends beyond the speed of rate cuts to the deeper design of currency and capital-market accessibility.

Energy costs are also feeding into inflation signals. South Korea’s March producer price index rose 4.1% year over year and 1.6% month over month, the fastest pace in more than three years, while coal and petroleum product prices jumped 31.9%. Even as SK hynix announced a 19 trillion won investment to build an advanced packaging plant for AI memory, the structural vulnerability of being an energy importer continues to transmit pressure through the exchange rate and inflation—one reason Korean markets can look strong yet feel uneasy.

Exilist ultimately argued that in the current environment, the most important signal is not the next short-term price swing but which components of crypto are concretely entering regulated financial infrastructure. Bitcoin still trades with macro sensitivity, but ETF flows and corporate treasuries are reinforcing demand. Regulation is moving from enforcement-first ambiguity toward market-structure design. Stablecoins are being debated as rails for currency reach and as instruments for treasury operations. Even without a clean macro resolution, institutional capital and policymakers appear to be treating crypto less as a peripheral asset class and more as a piece of the next financial system architecture.

🔎 Market Interpretation

- Macro backdrop is “higher-for-longer” constrained: IMF growth slowing (~3.1%) alongside sticky inflation risk (~4.4%) and renewed supply shocks (energy, geopolitics, tariffs) reduces central banks’ room to cut even if activity cools.

- Beige Book implies caution, not collapse: U.S. regions show slight/modest growth, but businesses delay hiring/investment amid geopolitical and tariff uncertainty—more defensive corporate behavior than imminent recession.

- Resilience becomes restrictive: U.S. retail sales strength is partly nominal (gasoline-driven), weakening the case for fast Fed easing; China’s steady LPR signals limited urgency for major stimulus—supporting the “discount rates stay high” narrative.

- Bitcoin still trades like a risk asset: BTC’s rebound (~$77.6k) tracked improved risk sentiment and easing energy stress; it behaved more “high-beta” than pure safe haven, though structural demand is increasingly cushioning drawdowns.

- Institutional bid is the key price support: Spot BTC ETF inflows (~$1.11B across four sessions cited) plus CoinShares’ $1.4B weekly inflows suggest demand-driven upside rather than short-covering rallies.

- Supply dynamics tighten via treasuries: Strategy’s additional 34,164 BTC (total 815,061 BTC) highlights how corporate accumulation can effectively reduce circulating supply versus ETFs that broaden access.

- Regulatory stance shifts to “how it works”: U.S. (SEC’s proposed innovation exemption for tokenized securities; CFTC steady rulemaking with strict anti-fraud focus) and Hong Kong (SFC enabling secondary trading of tokenized products) indicate a move from classification debates to market-structure implementation.

- Stablecoins reframed as currency and treasury tools: Debate expands from crypto liquidity to cross-border monetary influence and corporate finance (BIS warnings on redemption frictions; Europe pushing euro stablecoins/tokenized deposits; infrastructure enabling yield and public-market funding links).

- South Korea illustrates the crosscurrent: Strong exports/equities and AI capex coexist with inflation/energy import vulnerability and currency-volatility sensitivity—mirroring the global theme of growth resilience alongside policy constraints.

💡 Strategic Points

- Positioning framework: Treat BTC as macro-sensitive “risk-on with structural sponsorship.” Monitor oil/USD/real yields for short-term direction, but track ETF/treasury flows for downside support and medium-term trend.

- Key evidence to watch weekly:

- Spot BTC ETF net flows and concentration by issuer (signal of persistent institutional allocation vs episodic trading).

- Corporate treasury announcements (supply lock-up effect) and on-chain large-holder net selling/buying.

- Energy and tariff headlines (supply-side inflation shocks that delay easing).

- Regulated crypto winners likely shift “up the stack”: Potential beneficiaries are broker-dealers, ATS venues, custodians, compliance/KYC tooling, tokenization and settlement infrastructure—firms closest to market plumbing rather than purely retail exchanges.

- Tokenization’s inflection is secondary markets: Moving from issuance pilots to secondary trading forces solutions for distribution, price discovery, investor eligibility, and custody—raising barriers and favoring regulated platforms.

- Stablecoin due diligence focus: Evaluate redemption mechanics (T+0 liquidity, gates, fees), reserve composition, legal claim structure, and cross-jurisdiction licensing—BIS concerns imply “money-like” perception may not match实际 convertibility under stress.

- Portfolio construction trend: Growth of regulated BTC strategies (e.g., asset managers scaling systematic approaches) suggests competition shifts toward risk management, drawdown control, and compliance-grade reporting—not just accumulation narratives.

- Scenario map (next 3–12 months):

- Sticky inflation + resilient growth: Rates stay high; BTC trades choppy but supported by institutional inflows; market-structure plays (custody/ATS/tokenization rails) gain relative appeal.

- Growth rollover without inflation relief: Risk assets pressure; watch whether ETF inflows remain net positive—if yes, BTC downside may be contained versus prior cycles.

- Rapid disinflation: Risk-on broadens; BTC beta increases; stablecoin and tokenization activity could accelerate via easier funding conditions.

- Regional signal from Korea: In energy-importing economies, FX and producer prices can transmit energy shocks quickly; watch won volatility and PPI as early indicators of broader Asia risk sentiment and policy constraints.

📘 Glossary

- Supply-side shock: Inflationary pressure caused by disruptions or cost increases (energy, logistics, tariffs) rather than demand overheating.

- Headline inflation: Overall inflation including volatile items like food and energy (distinct from “core” inflation which excludes them).

- Fed Beige Book: A periodic qualitative report summarizing economic conditions across the 12 Federal Reserve districts.

- Discount rate / higher discount rates: The interest-rate environment used to value future cash flows; higher rates typically pressure valuations of risk assets.

- High-beta asset: An asset that tends to amplify market moves—rising more in risk-on periods and falling more in risk-off periods.

- Spot Bitcoin ETF: An exchange-traded fund that holds actual bitcoin (spot) to provide regulated exposure via traditional brokerage accounts.

- Short covering: Price buying driven by traders closing short positions, often causing sharp but potentially temporary rallies.

- Corporate treasury accumulation: A company buying and holding BTC as a reserve asset; can reduce liquid supply if held long-term.

- Innovation exemption (SEC, proposed): A potential regulatory framework to allow certain on-chain trading/issuance under defined conditions while rules evolve.

- Tokenized security: A traditional financial instrument (e.g., equity/fund interest) represented on a blockchain, typically with regulated issuance and transfer rules.

- ATS (Alternative Trading System): A regulated trading venue (often matching buyers/sellers) that is not a traditional exchange.

- Secondary trading: Trading of an already-issued asset between investors (as opposed to primary issuance). Critical for liquidity and price discovery.

- Stablecoin redemption friction: Delays, fees, minimums, or operational constraints that prevent stablecoins from always trading exactly at par with the reference currency.

- Tokenized deposits: Bank deposit claims represented on-chain, typically designed to retain bank-like money characteristics under regulation.

- Regulatory arbitrage: Shifting activity to jurisdictions with looser rules, potentially increasing systemic and consumer risks.

Comment 0