News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

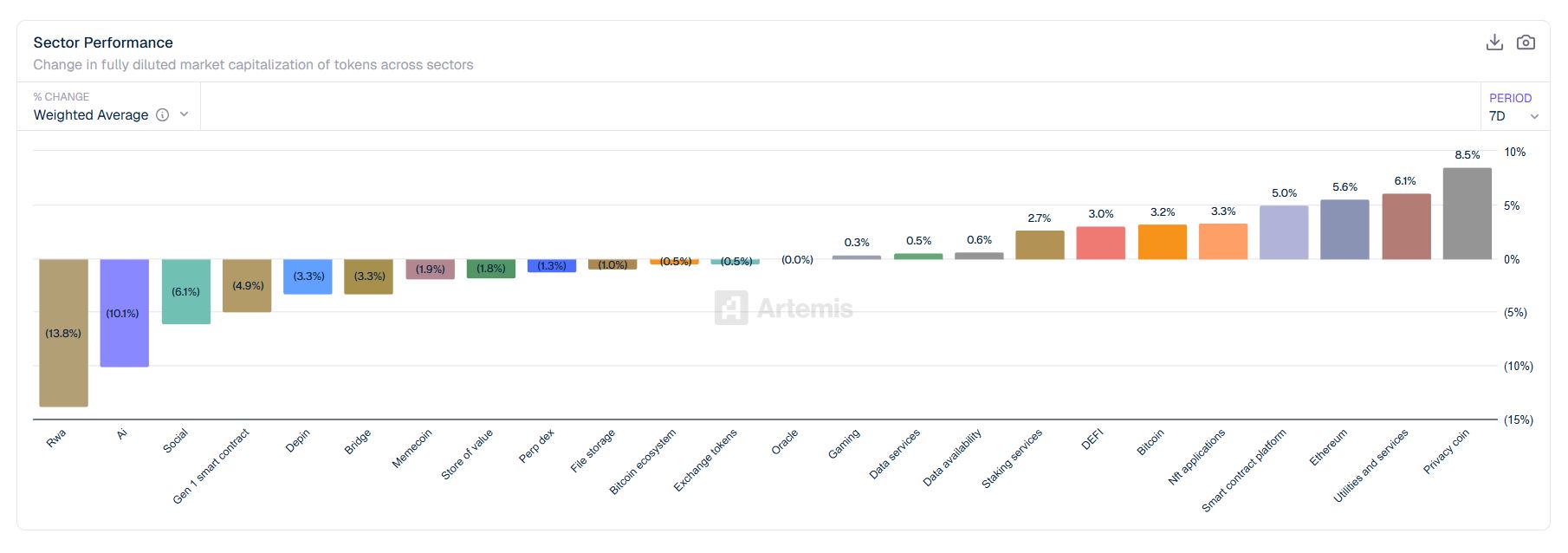

Crypto market flows are rotating back toward core infrastructure themes—led by 'privacy' tokens and Ethereum-linked assets—while higher-beta segments such as real-world assets (RWA) and AI-related tokens are seeing sharp weekly drawdowns, underscoring a renewed preference for durability over narrative-driven volatility.

Data compiled by Artemis, as of Monday 9:30 a.m. KST (Sunday 8:30 p.m. ET), shows the 'privacy coin' sector topped weekly gains in fully diluted valuation (FDV), rising 8.5%. That outperformance was followed by utilities and services (+6.1%), Ethereum (+5.6%), and smart contract platforms (+5.0%), indicating a broad bid for foundational crypto rails rather than peripheral use-case tokens.

Other major areas also held up relatively well. Bitcoin (BTC) posted a 3.0% weekly increase, while NFT applications (+3.3%) and decentralized finance (+3.2%) advanced in tandem. Staking services rose 2.7%, suggesting investors are again leaning into yield and network participation as risk appetite stabilizes in selected pockets of the market.

Several segments hovered near flat, reflecting a market still searching for direction outside the strongest themes. Oracles were unchanged (0.0%), while gaming (+0.3%), data services (+0.5%), and data availability (+0.6%) logged only modest gains—typical of sectors that often lag immediately after a leadership shift toward large-cap infrastructure.

The clearest sign of rotation, however, came from the steep declines in previously hot narratives. RWA tokens fell 13.8% on the week, the largest drop among tracked sectors, consistent with profit-taking after a prior run-up. AI-related tokens slid 10.1%, while social tokens dropped 6.1%, highlighting how quickly liquidity can exit crowded trades when momentum fades.

Weakness also spread across parts of the broader ecosystem. First-generation smart contract platforms declined 4.9%, while DePIN and bridge-related projects each fell 3.3%. Speculation-heavy segments were not spared: memecoins slipped 1.9%, 'store of value' themes fell 1.8%, and derivatives-focused DEX tokens weakened 1.3%, pointing to a pullback in riskier exposures and mid-layer infrastructure plays.

Meanwhile, smaller weekly declines in file storage (-1.0%), the Bitcoin ecosystem (-0.5%), and exchange tokens (-0.5%) suggested the selloff was not indiscriminate, but still reflective of a cooler tone in investor sentiment. Taken together, the sector-by-sector FDV moves suggest capital is increasingly consolidating into assets perceived as essential to the crypto stack—an allocation pattern that often emerges when traders prioritize liquidity, resilience, and clearer fundamental anchors.

🔎 Market Interpretation

- Rotation to core infrastructure: Weekly FDV performance shows capital moving into foundational crypto “rails” (privacy coins, Ethereum, utilities/services, smart contract platforms) rather than high-beta narratives.

- Durability over hype: Sharp declines in RWA (-13.8%) and AI (-10.1%) suggest momentum trades unwound quickly as risk appetite tightened.

- Selective risk-on pockets: BTC (+3.0%), DeFi (+3.2%), NFT apps (+3.3%), and staking (+2.7%) held up—implying investors still want exposure, but with liquidity and established demand drivers.

- Market breadth is uneven: Several sectors were near flat (oracles 0.0%, gaming +0.3%, data services +0.5%), consistent with a leadership shift where capital concentrates in fewer categories.

- Cooling, not capitulation: Smaller declines in exchange tokens (-0.5%), Bitcoin ecosystem (-0.5%), and file storage (-1.0%) indicate selling was targeted rather than indiscriminate.

💡 Strategic Points

- Preference signal: Outperformance in privacy (+8.5%) and Ethereum-linked segments (+5% to +5.6%) can be read as a bid for “base-layer” exposure when traders seek resilience.

- Watch for narrative re-entry conditions: RWA/AI weakness often stabilizes only after (1) volume compression, (2) improved relative strength vs. majors, and/or (3) a broader market risk-on impulse.

- Positioning implication: In rotations, leaders tend to be large-cap infrastructure first; laggards (oracles/gaming/data) may follow later if the uptrend broadens.

- Risk management takeaway: Crowded trades (AI, RWA, social) can see rapid liquidity exits—consider tighter sizing, clearer invalidation levels, or staged entries.

- Yield as a stabilizer: Staking services’ gains suggest demand for on-chain yield and network participation is returning, which can support L1/L2 ecosystems during consolidation phases.

📘 Glossary

- FDV (Fully Diluted Valuation): Token price multiplied by the total supply if all tokens were in circulation; often used to compare sectors but can overstate value when unlocks remain.

- Privacy coins: Cryptocurrencies focused on transaction confidentiality (e.g., obscuring sender/receiver/amount), often viewed as core infrastructure for privacy.

- RWA (Real-World Assets): Tokenized representations of off-chain assets (bonds, real estate, invoices) traded or used as collateral on-chain.

- High-beta: Assets that typically move more than the broader market—up more in rallies, down more in drawdowns.

- DeFi: Decentralized finance protocols enabling lending, trading, derivatives, and yield strategies without traditional intermediaries.

- DePIN: Decentralized Physical Infrastructure Networks—token-incentivized systems for real-world infrastructure (wireless, sensors, compute, etc.).

- Bridge: Infrastructure that transfers assets/data between blockchains; often sensitive to security and liquidity conditions.

- Oracles: Services that deliver external data (prices, events) to smart contracts, enabling many DeFi and on-chain applications.

Comment 0