News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Ripple’s strongest quarter on record is colliding with a stubborn reality in the market: XRP (XRP) remains trapped in a prolonged slump, underscoring a growing disconnect between the company’s business momentum and the token’s price performance.

As of March 30, 2026 (UTC), XRP was trading around $1.32—down more than 63% from its July 2025 peak near $3.65. The drawdown has persisted even as Ripple posts blockbuster operating metrics and expands adoption among major financial institutions.

Ripple reported that its prime brokerage revenue tripled in the first quarter of 2026, marking what it described as a record-setting period. The company also highlighted a $750 million share buyback announced on March 11 (UTC), a transaction that implied a corporate valuation of roughly $50 billion. Separately, Ripple said its total payments processed has now surpassed $100 billion, and pointed to its infrastructure being used by treasury teams at Fortune 500 companies via GTreasury—an enterprise treasury platform acquired for $1 billion.

The market tension, however, lies in who benefits. Much of the economic upside from these business lines accrues to Ripple’s equity holders rather than XRP holders. In practical terms, banks and enterprise clients are increasingly settling via fiat rails or Ripple’s own stablecoin rather than relying on XRP as a bridge asset—diluting the direct linkage investors often assume between Ripple’s commercial traction and XRP demand.

That dynamic is especially visible in RLUSD, Ripple’s USD-pegged stablecoin launched in December 2024. RLUSD has grown to an estimated market capitalization of $1.56 billion, with roughly 88% of supply residing on the Ethereum (ETH) network—an allocation that further reinforces how Ripple’s ecosystem growth is not necessarily XRP-centric.

Institutional engagement, while expanding, has not translated into price strength. In February 2026 (UTC), several large financial institutions—including Deutsche Bank, Aviva Investors, and Société Générale—began using Ripple infrastructure, according to the report. Over the same period, XRP fell about 30%, reinforcing the market’s conclusion that institutional adoption of Ripple’s rails does not automatically generate incremental demand for the token.

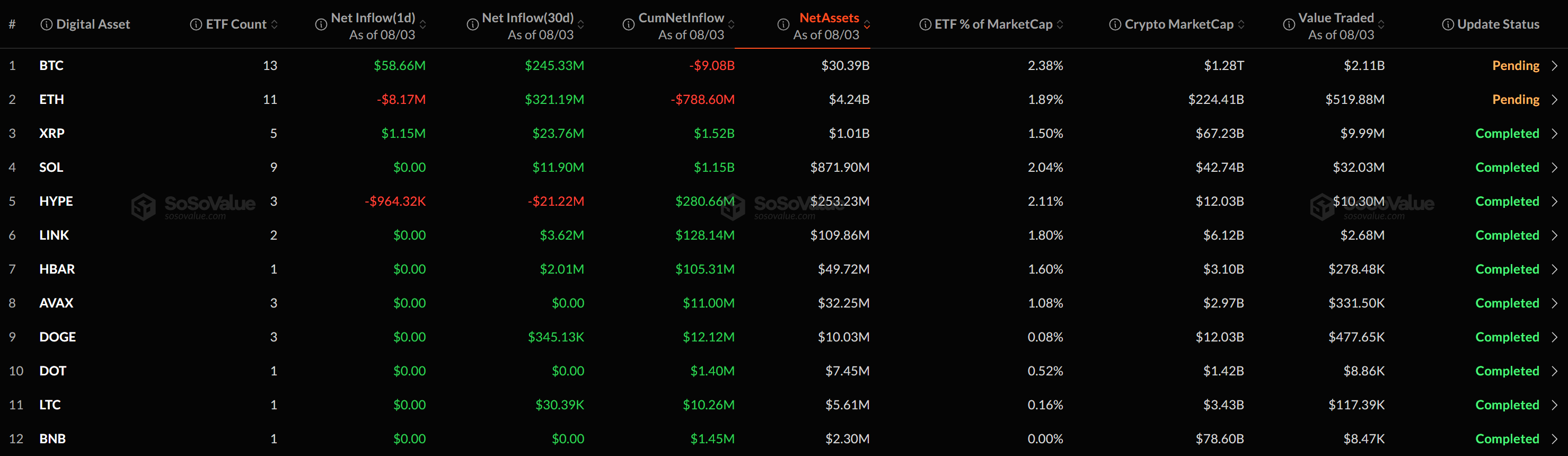

Trading data reflects the same imbalance. XRP’s 24-hour trading volume was about $1.91 billion, with nearly all of it concentrated on centralized exchanges, while decentralized exchange activity was roughly $1.81 million. XRP’s market capitalization stood near $81 billion, keeping it ranked fifth across the broader crypto market, with a market share around 3.53%.

Regulatory signals have improved, but key catalysts remain unresolved. A wave of spot XRP ETF applications—filed by asset managers including Grayscale, Bitwise, and Franklin Templeton among a group of six—did not receive approval by the expected March 27 decision window (UTC). The delay coincided with broader market-wide sell pressure, which added to downside momentum across major tokens.

Still, regulators have delivered a notable development for XRP’s classification. In March 2026 (UTC), the U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission issued a joint interpretive framework that formally categorized XRP as a 'digital commodity'—placing it in the same broad bucket as Bitcoin (BTC) and Ethereum (ETH). Market participants largely viewed the move as a meaningful step toward regulatory clarity, even if it did not immediately shift ETF timelines.

Ripple CEO Brad Garlinghouse has also argued that legislative progress could arrive this year, estimating an 80% chance of passage for the proposed crypto market structure 'Clarity Act'. However, he suggested the timeline may slip from late April to late May. Senator Cynthia Lummis, a leading voice on digital asset policy, said the Senate Banking Committee is targeting late April to complete revisions to the bill.

Analyst expectations for XRP remain mixed but broadly anchored to two variables: sustained institutional adoption and whether ETF approval ultimately materializes. Some market analysts are projecting XRP in the $2.25 to $2.50 range by the end of 2026. Standard Chartered, meanwhile, cut its 2026 target by roughly 65% to $2.80, following a reassessment after XRP’s slide toward $1.16 in February (UTC).

Longer-term forecasts diverge sharply. Estimates cited in the report ranged from a bearish 2030 scenario near $4 to a bullish case around $28—an outcome that would imply more than 20x upside from current levels, though such projections depend heavily on adoption pathways and market structure reforms that are far from guaranteed.

In the nearer term, XRP’s trend has remained negative. Over the past 24 hours, the token slipped about 0.12%, while it is down roughly 7.49% over seven days, 4.57% over 30 days, and 29.41% over 90 days (UTC).

For investors, the broader takeaway is that Ripple’s operational success is no longer a straightforward proxy for XRP performance. As Ripple expands enterprise offerings—particularly stablecoin and treasury infrastructure—markets are being forced to reassess XRP’s token economics and the degree to which real-world usage translates into on-chain demand. With regulatory clarity improving but ETF decisions still pending, the next major inflection point for XRP may hinge less on Ripple’s quarterly results and more on how policy and product approvals reshape market access.

🔎 Market Interpretation

- Business strength vs. token weakness: Ripple posted its strongest quarter (prime brokerage revenue up ~3x, $750M buyback implying ~$50B valuation, payments processed >$100B), yet XRP remains in a deep drawdown—about $1.32, down ~63% from the July 2025 peak near $3.65.

- Decoupling is driving the slump narrative: The market increasingly treats Ripple’s commercial traction as benefiting equity holders more than XRP holders, as enterprise settlement can occur via fiat rails or Ripple’s stablecoin rather than XRP as a bridge asset.

- RLUSD growth is a signal: RLUSD’s estimated $1.56B market cap and the fact that ~88% of supply is on Ethereum reinforces that the expanding Ripple ecosystem is not necessarily XRP-centric.

- Institutional adoption hasn’t supported price: Even with reported usage by major institutions (e.g., Deutsche Bank, Aviva Investors, Société Générale), XRP fell ~30% over the referenced period—strengthening the conclusion that “rails adoption” ≠ “token demand.”

- Market structure and liquidity profile: XRP’s activity remains CEX-dominant (24h volume ~$1.91B) with minimal DEX volume (~$1.81M), while market cap sits near $81B (ranked fifth; ~3.53% share).

- Regulatory clarity improved, catalysts delayed: A joint SEC/CFTC framework categorizing XRP as a “digital commodity” is constructive, but spot ETF decisions were delayed past the expected March 27 window, coinciding with broader market sell pressure.

- Near-term trend still negative: Performance remains weak across timeframes (approx. -0.12% 24h, -7.49% 7d, -4.57% 30d, -29.41% 90d), keeping sentiment cautious despite operating headlines.

💡 Strategic Points

- Re-rate XRP on token-specific demand, not Ripple’s revenue: Monitor indicators tied directly to XRP utility (bridge volume, on-ledger usage, liquidity corridors) rather than assuming Ripple’s enterprise growth automatically accrues to the token.

- Track substitution risk from RLUSD and fiat settlement: If more flows migrate to stablecoin/fiat rails, XRP’s role as a bridge asset may remain limited—pressuring the “adoption → price” thesis.

- ETF optionality remains a key catalyst: The path of spot XRP ETF approvals (applications from firms including Grayscale, Bitwise, Franklin Templeton and others) may matter more for price than quarterly operational metrics by expanding market access and liquidity.

- Regulatory framework is supportive but not sufficient: “Digital commodity” classification may reduce legal overhang, yet price impact may depend on follow-through (ETF timelines, exchange/product listings, institutional compliance pathways).

- Watch legislative timing risk: The proposed market structure “Clarity Act” is framed as a potential 2026 catalyst, but shifting timelines (late April → late May discussion) can prolong uncertainty and cap rallies.

- Use scenario-based expectations: Street targets cluster around $2.25–$2.50 into end-2026, with some higher calls (e.g., revised Standard Chartered view around $2.80). Longer-dated projections vary widely (~$4 bearish to ~$28 bullish by 2030), implying outcomes hinge on adoption pathways and policy/product approvals rather than linear growth.

- Market structure clue: Strong CEX concentration and weak DEX activity suggests XRP price discovery is heavily influenced by centralized venue flows, which can amplify macro sell-offs and delay “fundamental” repricing.

📘 Glossary

- Bridge asset: A token used to facilitate cross-asset or cross-currency settlement by acting as an interim medium of exchange (e.g., converting Currency A → XRP → Currency B).

- Fiat rails: Traditional payment networks and banking infrastructure used for transferring government-issued currencies (USD, EUR, etc.).

- Stablecoin (RLUSD): A cryptocurrency designed to maintain a stable value, typically pegged to a fiat currency; RLUSD is Ripple’s USD-pegged stablecoin.

- Market capitalization: Token price multiplied by circulating supply; a rough measure of total network value as priced by the market.

- CEX / DEX: Centralized exchange (custodial trading venue) vs. decentralized exchange (on-chain, non-custodial trading protocol).

- Spot ETF: An exchange-traded fund that aims to hold the underlying asset directly (here, XRP) rather than using futures contracts.

- Digital commodity: A regulatory classification suggesting a digital asset is treated more like a commodity (similar bucket to BTC/ETH in the article), often viewed as reducing securities-law uncertainty.

- Share buyback: A company repurchasing its own shares, often signaling financial strength and reducing outstanding equity float.

- Prime brokerage (crypto): Institutional services such as execution, custody, financing, and liquidity access tailored to large traders and funds.

Comment 0