News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Crypto teams are increasingly reaching for token ‘buybacks’ as a go-to defense when prices slide—on the intuitive premise that reducing circulating supply should lift value. But a review of onchain data across multiple projects suggests the opposite: buybacks rarely create durable token value, and often simply burn runway that could have been used to build products or grow users.

The debate was crystallized by Bankr (BNKR) developer 0xDeployer, who pushed back on community demands for more repurchases. Even if the project “spent all revenue from the last six months on $BNKR buybacks,” he argued, “the chart would look the same two weeks later—except we’d be out of money to keep building.” It reads like a rhetorical flourish, but recent buyback programs from Jupiter (JUP), dYdX (DYDX), and Clanker (CLANKER), alongside widely cited counterexamples such as Hyperliquid (HYPE) and Aave (AAVE), paint a consistent picture: buybacks tend to be a ‘capital return’ mechanism, not a growth engine.

Why TradFi buybacks don’t map cleanly onto crypto

In traditional equity markets, buybacks are typically executed from surplus cash and framed as a tax-efficient way to return capital to shareholders. Quant studies, including research attributed to Two Sigma, have found that companies repurchasing shares often already show stronger profitability, leverage profiles, and cash-flow metrics before those buybacks occur. In other words, buybacks are frequently an outcome of business strength, not the cause of it.

Token markets invert that sequence. Many crypto buybacks are launched under social pressure, funded from budgets that would otherwise support development, liquidity incentives, or distribution. And unlike equities—whose dilution is usually bounded by board-approved issuance—tokens can face large and pre-committed emissions and unlock schedules that turn repurchases into a rounding error against supply expansion.

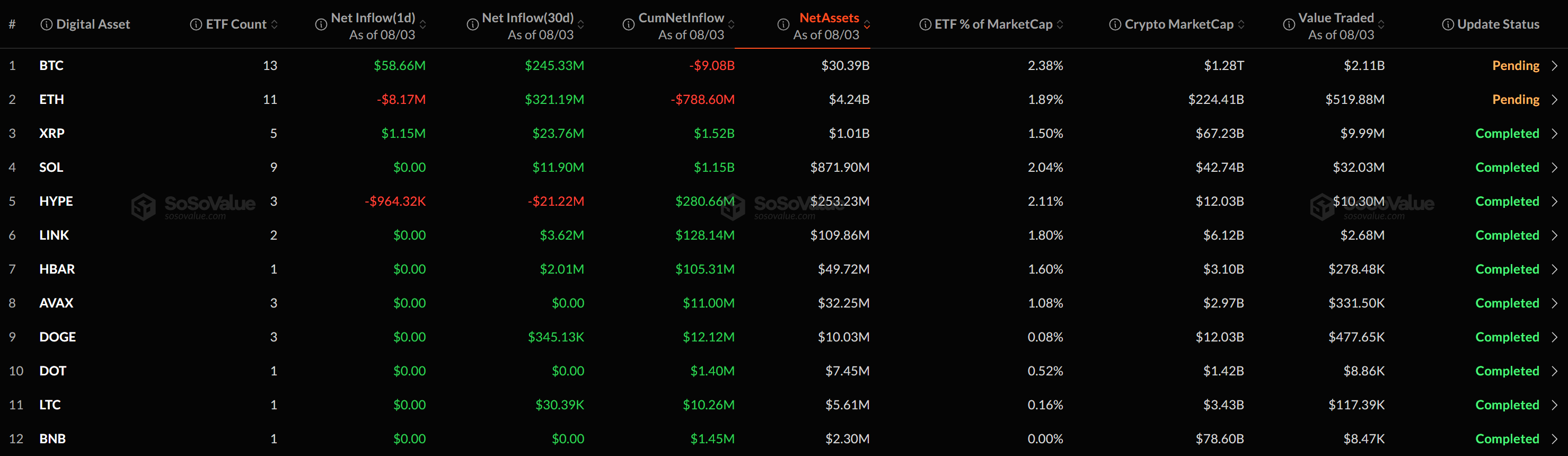

Case 1: Jupiter (JUP)—about $70 million spent, still down roughly 92% from peak

Jupiter (JUP), a leading Solana-based DEX aggregator, introduced a buyback program in February 2025, allocating 50% of fees to repurchasing JUP and locking purchased tokens for three years. Over roughly 12 months, the protocol deployed about $70 million.

By early 2026, however, JUP traded around $0.15—about 92% below its high. The core issue wasn’t a lack of buyback commitment; it was the scale of supply dynamics. Circulating supply had expanded meaningfully since launch, while unlocks of roughly tens of millions of tokens per month were scheduled to continue into mid-2026. Against the implied sell pressure, the buyback absorbed only a small fraction of unlock-driven supply—insufficient to reset market pricing.

Jupiter co-founder Siong Ong acknowledged the limitations in early January 2026, saying the project had spent more than $70 million on buybacks with little impact on price—arguing those resources would be better redirected into incentives for both existing and new users. Around the same time, Helium’s leadership similarly signaled that token repurchases were being deprioritized, describing them as an inefficient use of funds in a market that was not rewarding projects merely for buying their own tokens.

Case 2: dYdX (DYDX)—clear rules, real revenue, and still a steep drawdown

dYdX (DYDX) launched a buyback program in March 2025, earmarking roughly 25% of protocol revenue for repurchases under a defined framework. If buybacks were going to work anywhere, proponents argued, it would be in a mature DeFi protocol with recurring revenue and transparent execution.

Even so, over the subsequent year DYDX fell sharply—around 88% over the period cited in the analysis. The takeaway is not that buybacks are irrelevant, but that they are often overwhelmed by broader market regimes, sector rotations, and token-specific supply overhangs. In practice, buybacks did not function as an effective downside shock absorber.

Case 3: Clanker (CLANKER)—failed even under near-ideal design

The strongest argument against buyback determinism comes from Clanker (CLANKER). After Farcaster acquired Clanker in October 2025, the buyback architecture was designed to be unusually stringent: a large share of protocol fees was automatically routed to perpetual CLANKER repurchases, with minimal human discretion.

Following the announcement, CLANKER surged more than 400% in a week—only to drift back toward pre-announcement levels later. Onchain activity showed a tight linkage between fee generation and buyback size, including weeks where automated purchases spiked into the multi-million-dollar range. Yet the token price declined during periods of the heaviest execution. Even after a meaningful portion of supply had been repurchased, the market did not apply a sustained ‘re-rating’ to the asset.

The implication was blunt: the initial rally looked more like a narrative-driven repricing around an acquisition event than a buyback-driven structural bid.

What about Hyperliquid (HYPE) and Aave (AAVE)?

Hyperliquid (HYPE) and Aave (AAVE) are often cited as buyback “successes” because both appreciated during windows when repurchases were active. But the direction of causality matters. Hyperliquid’s buyback capacity was underwritten by unusually large protocol fees—numbers that place it among crypto’s revenue leaders—paired with tokenomics viewed as relatively robust. In that framing, buybacks amplified an already-strong signal rather than creating it. Even then, the token later pulled back materially from its peak, underscoring that repurchases do not immunize assets from risk-off cycles.

Aave’s revamped token-economics plan included recurring repurchases of roughly $1 million per week for several months, and the token price more than doubled from spring 2025 levels cited in the report. Yet AAVE subsequently fell sharply from its highs as macro conditions shifted in early 2026, despite Aave’s position as a DeFi category leader by total value locked. The program proved unable to offset broader drawdowns once liquidity conditions deteriorated.

Across both cases, buybacks looked like a downstream effect of ‘product strength’ and ‘revenue scale’—not a lever that could manufacture either.

The real cost of a buyback dollar: runway

For early-stage teams, the opportunity cost is acute. A dollar allocated to repurchasing tokens is also a dollar not spent on engineering hires, product iteration, audits, distribution, partnerships, or user incentives. Several teams have explicitly framed the trade-off as existential: the ability to survive the next market cycle may depend more on preserving runway than on attempting to manage price through financial engineering.

If not buybacks, what actually supports token value?

The analysis points to two structural levers that markets appear to reward more consistently than repurchases. First is a ‘utility sink’—a mechanism where using the protocol requires holding, staking, or spending the token, creating demand that scales with adoption rather than treasury outlays. Second is ‘controlled emissions’: if supply expansion is disciplined and predictable, price discovery has a chance to converge with real usage and revenue. Conversely, aggressive unlock schedules can overwhelm even well-funded buyback programs.

Ultimately, the onchain evidence across the case studies converges on the same conclusion: buybacks are best understood as a ‘return-of-capital’ tool, not a growth strategy. Markets tend to reward projects that build products users actively want—not projects that simply repurchase their own tokens. The central question teams must answer before discussing buybacks is straightforward: is there a clear, non-speculative reason to own the token? If that answer is uncertain, buybacks are unlikely to make it clearer.

Comment 0