News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Bitcoin (BTC) options positioning continues to tilt bullish, with traders increasingly concentrating activity in ultra-high strike call contracts—an expression of ‘tail-risk upside’ that can amplify during periods of strong risk appetite or volatility repricing.

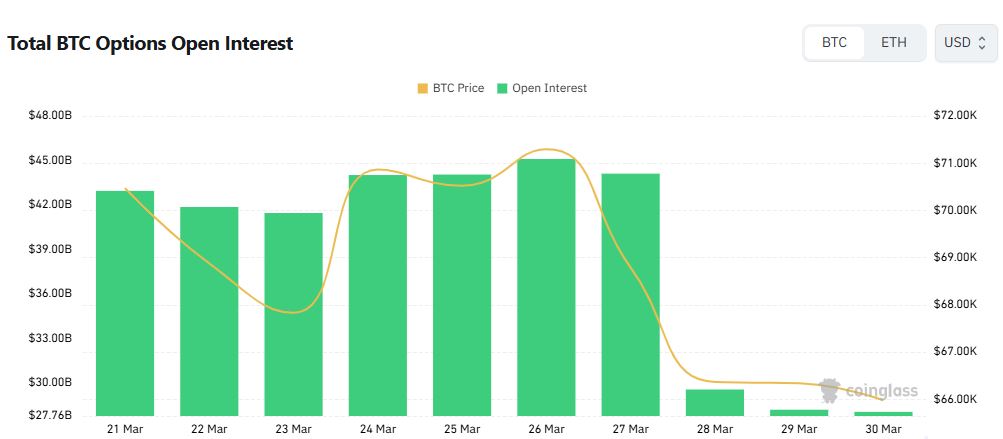

As of 12:00 a.m. ET on March 30, data compiled by Coinglass showed total Bitcoin options open interest (OI) at approximately $28.05 billion, down about 0.5% from the prior day’s $28.19 billion. Calls accounted for 57.14% of outstanding contracts, compared with 42.86% for puts, reinforcing a market structure that remains skewed toward upside exposure.

Options trading volume over the past 24 hours totaled roughly $1.386 billion. By venue, Deribit led with $375 million, followed by Bybit at $471 million, Binance at $266 million, OKX at $235 million, and CME at $39 million. In volume terms, call options represented 54.84% versus 45.16% for puts, suggesting bullish flow remains dominant even in short-term activity.

Where the market becomes more notable is in the strike selection. The largest concentrations of open interest were seen in a $120,000 call expiring Dec. 25, 2026 on Deribit, alongside $60,000 puts expiring Dec. 25, 2026 and June 26, 2026, also on Deribit. The mix of high-strike calls paired with sizeable put positioning at a much lower strike highlights a common institutional-style posture: retaining upside participation while maintaining downside hedges around key levels.

Meanwhile, the most actively traded contracts in the past 24 hours featured extreme upside strikes. The top volume contract was a $380,000 call expiring June 26, 2026 on Deribit, followed by a $300,000 call expiring June 26, 2026 on Bybit. A $74,000 call expiring March 30, 2026 on Bybit also ranked among the most traded contracts, pointing to continued demand across both far-out “lottery ticket” upside and more conventional bullish exposures.

Market participants typically use options to either take leveraged directional views or hedge existing spot and derivatives positions. Open interest measures the total number of outstanding contracts and is often used as a gauge of how much positioning has accumulated, while changes in call/put share and trading volume can help distinguish longer-horizon positioning from short-term defensive activity. In this case, the call-heavy OI structure alongside active trading in very high-strike calls indicates that some traders are paying for convex upside exposure—while the persistence of meaningful put interest suggests that volatility protection remains part of the broader positioning landscape.

Overall, the data points to a Bitcoin options market that is still structurally optimistic, but not complacent—balancing ‘upside convexity’ demand with ongoing hedging interest, a combination that often emerges when investors expect large potential moves rather than a narrow trading range.

Comment 0