News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

The hardest part of investing is often not finding the next trade, but resisting the urge to act at all—a lesson that resonates in today’s crypto market, where 24/7 price action and constant headlines can turn impatience into costly overtrading.

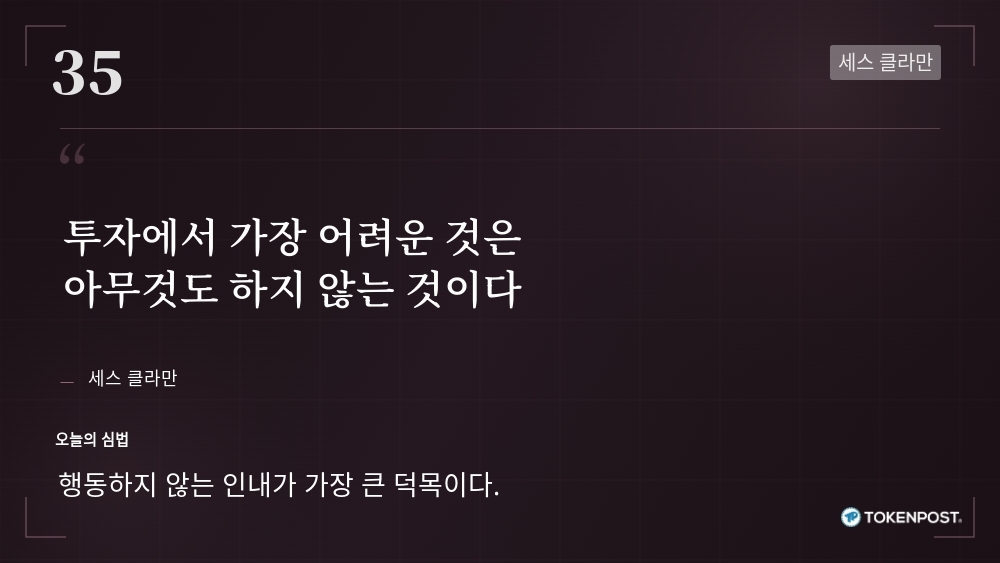

A Korean-language investor education series this week highlighted a widely cited line from value investing heavyweight Seth Klarman: “The most difficult thing in investing is doing nothing.” The message was presented not as a call to buy or sell any specific asset, but as a reminder that disciplined inaction can be a competitive edge in volatile markets.

The piece also revisited a framework popularized by financial writer Morgan Housel: investors should separate ‘luck’ from ‘skill’ with brutal honesty. The example often used is Microsoft co-founder Bill Gates—his access to a school with early computing resources is frequently described as a product of circumstance as much as ability. In market terms, the lesson is straightforward: attributing gains entirely to skill can breed overconfidence, while blaming losses entirely on bad luck blocks learning and improvement.

In crypto, where narratives can change within hours and liquidity can disappear quickly, mislabeling luck as skill can be especially damaging. A trader who profits from a sudden ‘liquidity inflow’ or an unexpected policy headline may assume the outcome was repeatable, increasing position sizes or leverage at exactly the wrong time. Conversely, dismissing a drawdown as a fluke can prevent an investor from recognizing flawed risk management, poor entry discipline, or an overconcentrated portfolio.

Klarman’s career is often cited as an institutional-scale example of patience as a core principle. The founder of Baupost Group, Klarman is known for a strict interpretation of value investing: buying only when assets trade at a steep discount to intrinsic value and holding substantial cash when such opportunities are scarce. He is also the author of Margin of Safety, a book considered so rare in print that secondhand copies have historically sold for thousands of dollars—an indicator of his influence in long-term, fundamental investing circles.

While crypto markets differ sharply from the public equities landscape that shaped Klarman’s reputation, the underlying behavioral challenge is comparable. When ‘good opportunities’ are not clearly present—whether due to stretched valuations, deteriorating liquidity conditions, or elevated event risk—doing less can be a form of risk control. In practice, that may mean waiting for clearer setups, reducing exposure, or simply avoiding constant portfolio tinkering driven by fear of missing out.

The broader takeaway is that investor outcomes are often determined not only by analysis, but by behavior under uncertainty. Recognizing the mix of luck and skill—and cultivating the patience to ‘do nothing’ when conditions do not justify action—remains a durable lesson as digital asset markets continue to mature.

🔎 Market Interpretation

- Inaction as edge in 24/7 markets: The article frames “doing nothing” as an underused advantage in crypto, where constant price movement and news amplify impulsive decision-making.

- Behavior outweighs analysis in volatility: Outcomes can hinge less on finding trades and more on avoiding overtrading, FOMO-driven reallocations, and reactionary leverage.

- Luck vs. skill misreads are magnified in crypto: Sudden liquidity shifts or policy headlines can create “right for the wrong reasons” wins; treating these as repeatable skill can lead to larger, poorly timed risk-taking.

- Risk control through selectivity: When valuations feel stretched, liquidity deteriorates, or event risk rises, reducing activity (or exposure) is presented as a legitimate defensive posture—not missed opportunity.

💡 Strategic Points

- Adopt a “default to no trade” filter: Require clear, pre-defined setups before acting; if conditions are ambiguous, staying flat is a decision, not indecision.

- Separate process from outcome: After gains/losses, review whether the decision was sound given information at the time—avoid labeling every win as skill and every loss as bad luck.

- Control position sizing after headline-driven moves: Treat profits from unexpected catalysts (liquidity inflows, policy news) as potentially non-repeatable; avoid increasing leverage simply due to recent success.

- Use patience as a risk-management tool: When opportunity quality is low, consider holding more cash/stables, trimming exposure, and reducing “portfolio tinkering” frequency.

- Identify preventable drawdown causes: If losses occur, check for repeatable errors—overconcentration, weak entry discipline, lack of stop/exit rules—rather than dismissing them as flukes.

- Establish guardrails against overtrading: Limit number of trades per week, set review windows (e.g., weekly rebalances), and define “no-trade zones” around major event risk.

📘 Glossary

- Overtrading: Excessive trading frequency, often driven by emotion or noise, that increases fees, slippage, and errors.

- Intrinsic Value: An estimate of an asset’s “true” value based on fundamentals; central to value-investing frameworks.

- Margin of Safety: Buying with a buffer between price and estimated intrinsic value to reduce downside risk if assumptions are wrong.

- Liquidity: How easily an asset can be bought/sold without moving price materially; thin liquidity increases volatility and execution risk.

- Liquidity Inflow: A surge of capital or buying capacity entering a market that can lift prices quickly, sometimes temporarily.

- Leverage: Borrowed exposure that amplifies gains and losses; can be especially dangerous when volatility spikes.

- Event Risk: Price risk tied to discrete events (regulatory decisions, macro data, exchange incidents) that can trigger sharp moves.

- FOMO (Fear of Missing Out): A behavioral bias that pushes investors to chase moves or narratives to avoid feeling left behind.

Comment 0