News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

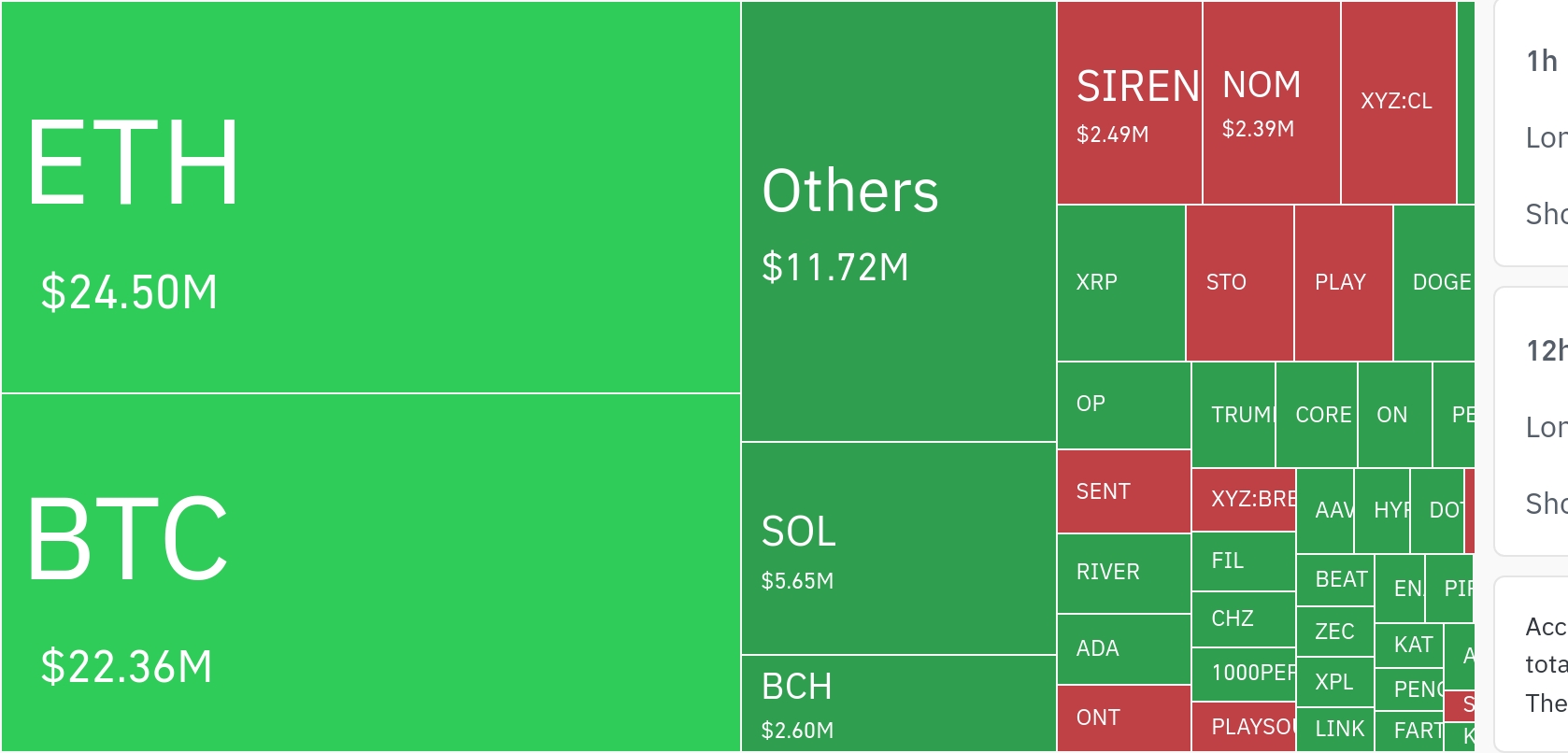

Ethereum (ETH) network fees jumped roughly 36% over a single day as a burst of real-world asset (RWA) settlement activity and stablecoin flows concentrated into narrow time windows, tightening available blockspace and driving a sharp uplift in revenue. The move is notable not because of a simple price-linked spike in usage, but because it signals a shift toward 'high-value' payment and settlement demand—activity that tends to be stickier than speculative trading.

Market data showed ETH down about 2.69% on a snapshot basis during the same period, underscoring that the fee surge was not merely a function of token price momentum. Instead, the fee dynamics reflected intraday congestion as larger, institution-oriented transactions hit Ethereum mainnet and its Layer 2 (L2) networks simultaneously.

A key catalyst highlighted by market watchers is the expanding role of Circle ($CRCL) in onchain settlement—particularly its Arc L1 initiative and the broader scaling of USDC-based RWA payments. Arc is being framed less as a standalone chain and more as a payments and settlement rail designed to pull institutional capital onchain. As tokenized instruments such as U.S. Treasuries, T-bills, and commodities are increasingly settled using USD Coin (USDC) on Ethereum L2s, large batch transactions can cluster around specific cutoffs, amplifying temporary congestion and fee generation.

In that context, Ethereum’s fee revenue begins to resemble 'real yield' rather than simple transactional friction. The demand driver is not meme-coin speculation or retail bursts, but recurring clearing and settlement needs tied to institutional workflows. For Ethereum, this reinforces the thesis that the network continues to operate as a 'high-value network' where blockspace is priced by the economic value of the activity it supports.

Solana (SOL), by contrast, posted only a modest 0.18% increase over the same window, with analysts pointing to 'stagnant throughput monetization' as a limiting factor. While Solana’s architecture is optimized for high-speed, low-cost execution and can process large volumes of transactions, critics argue the network’s revenue capture is structurally weaker—fees are comparatively thin and value accrual is more concentrated around validators rather than consistently flowing to long-term token holders.

That imbalance has been visible in Solana’s historical fee profile. During prior meme-coin cycles, annualized fees reportedly reached as high as $2.8 billion, only to fall sharply afterward—by as much as 79%—illustrating how quickly fee revenue can evaporate when traffic is primarily speculative and cyclical.

On a 30-day basis, the revenue gap also appears pronounced. Estimates cited by market participants put total fees at about $320.35 million for Ethereum versus $186.13 million for Solana—roughly a 72% advantage for Ethereum. Average daily fees were estimated near $10.7 million for Ethereum compared with about $6.2 million for Solana. Beyond raw totals, the networks’ value capture differs by design: Ethereum pairs fee burning with staking economics, while Solana’s distribution is more validator-centric, shaping how economic value accumulates across each ecosystem.

The divergence looks less like a one-off spike and more like an emerging structural trend. Over a 7-day cumulative window, figures referenced by analysts showed Ethereum at roughly $58.11 million in fees versus Solana at $34.78 million—maintaining a similar gap of about 67% even after smoothing out daily volatility.

One of the more counterintuitive dynamics supporting Ethereum’s revenue resilience is what some observers call the 'L2 scaling paradox'. Even as average fees per transaction have fallen toward the $0.01 range, total revenue has increased. The logic is economic: lower per-transaction costs can attract more institutional-grade settlement flows, expanding total payment volume and allowing the network to earn more in aggregate through 'scale effects'. In this framing, L2s such as Base and Arbitrum are not simply diluting fee capture; they are broadening the market, while still generating indirect value for Ethereum’s core settlement layer.

Solana’s challenge, analysts argue, is the mirror image. Transaction counts may remain high, but the unit economics are so compressed that network-wide revenue does not scale proportionally. The chain sustains a 'high-volume' model, yet its 'revenue density' per unit of activity remains comparatively low.

Overall, the episode adds weight to a market narrative that the competition among smart-contract platforms is shifting away from headline TPS metrics and toward which network can consistently process more economically meaningful transactions. Ethereum’s rising share of RWA and stablecoin settlement flows is increasingly viewed as a durable fee driver, while Solana is still broadly associated with traffic-led cycles. If these patterns persist, analysts say the long-run valuation gap between ecosystems may increasingly track differences in fee structure and revenue durability—because revenue remains one of the most direct indicators of sustainable network demand.

🔎 Market Interpretation

- Ethereum fee shock was usage-driven, not price-driven: ETH fell ~2.69% while network fees jumped ~36%, implying congestion from transaction timing and composition rather than speculative price momentum.

- Blockspace tightened due to institutional-style batching: RWA settlements and stablecoin (USDC) flows clustered into narrow cutoffs, creating intraday congestion and a meaningful lift in fee revenue.

- “High-value” settlement demand looks stickier: The article frames the fee increase as tied to recurring clearing/settlement workflows (RWA + stablecoins), which are typically more durable than meme-coin or retail bursts.

- Ethereum vs Solana monetization divergence: Solana saw only ~0.18% fee increase and is described as facing weaker throughput monetization—high activity, but thin fee capture and value accrual skewed toward validators.

- Revenue gap appears structural, not anecdotal: Cited estimates show ETH leading in fees over 30D ($320.35M vs $186.13M) and 7D ($58.11M vs $34.78M), maintaining ~67–72% advantage across windows.

- Market narrative shift: Competition is increasingly framed around “economically meaningful transactions” and durable fee structures, not headline TPS.

💡 Strategic Points

- Watch RWA + stablecoin settlement calendars: If settlement windows are driving congestion, fee/revenue spikes may correlate with institutional batch cutoffs rather than crypto-native trading cycles.

- Circle/USDC rails as a demand multiplier: Circle’s Arc L1 initiative is portrayed as a settlement rail that can pull institutional flows onchain; increased USDC RWA settlement on Ethereum L2s may keep demand elevated.

- “Real yield” framing strengthens ETH’s value proposition: Revenue linked to payments/settlement is positioned as closer to sustainable network demand than revenue tied to speculative mania.

- L2 scaling paradox supports aggregate revenue: Even if per-tx fees fall toward ~$0.01, total revenue can rise if lower costs expand total settlement volume (scale effects) and preserve Ethereum’s role as final settlement.

- Solana’s monetization risk: A high-volume/low-fee model may struggle to translate usage into durable network-wide revenue; past meme cycles showed fees can expand rapidly then decay sharply (reported up to ~$2.8B annualized, then -79%).

- Valuation implication: If durable fee drivers persist (RWA, stablecoins, institutional settlement), analysts expect ecosystem valuation gaps to track revenue durability and fee-structure design (burning + staking vs validator-centric distribution).

📘 Glossary

- Network fees (gas): Payments users make to include transactions in blocks; rise when blockspace demand exceeds supply.

- Blockspace: The limited capacity of a blockchain to process transactions per block; scarcity can drive fee spikes.

- RWA (Real-World Assets): Tokenized representations of offchain assets (e.g., U.S. Treasuries, T-bills, commodities) settled onchain.

- Stablecoin flows: Transfers of price-pegged tokens (e.g., USDC) often used for payments, settlement, and treasury operations.

- USDC: USD Coin, a dollar-pegged stablecoin issued by Circle, widely used for onchain settlement.

- Circle Arc / Arc L1: Referenced as a Circle-linked initiative framed as a payments/settlement rail to onboard institutional activity onchain.

- L1 (Layer 1): The base blockchain (e.g., Ethereum mainnet) that provides core security and settlement.

- L2 (Layer 2): Scaling networks (e.g., Base, Arbitrum) that execute transactions off L1 and post proofs/data to L1, reducing per-tx costs.

- Fee burning: Mechanism (notably on Ethereum via EIP-1559) where part of fees are destroyed, affecting supply dynamics.

- Staking economics: Rewards and incentives for securing a network by locking tokens; interacts with fee/revenue distribution.

- Throughput monetization: How effectively a chain converts transaction volume (TPS) into revenue captured by the protocol/ecosystem.

- Revenue density: Revenue generated per unit of activity; higher density implies more economically meaningful usage per transaction.

- Real yield (contextual): Fee revenue viewed as stemming from fundamental economic activity (payments/settlement) rather than transient speculation.

Comment 0