News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

As governments tighten regulations and economic shocks ripple across markets, the question for households and investors is becoming less academic: when a country wobbles, where is your wealth actually parked—and how resilient is it?

The vulnerability of concentrated assets was thrown into sharp relief in China in November 2020, when Ant Group—founded by Jack Ma—was preparing what was expected to be the world’s largest initial public offering. The deal, widely reported at the time to be valued at roughly 50 trillion won (about $45 billion at then-prevailing exchange rates), was abruptly suspended after a sudden regulatory shift. The fallout extended far beyond a single listing. Chinese technology stocks sold off hard, and the sector’s lost market value over the following period was ultimately measured in the hundreds of billions of dollars, underscoring how quickly political and regulatory risk can reprice ‘growth’ narratives.

The broader lesson is not confined to any one jurisdiction. Market history has repeatedly shown that crises often arrive without a clean schedule—whether currency shocks, systemic banking stress, or global health emergencies—and the gap between those who prepared and those who did not can take years to close. For investors, the relevant question is less whether another disruption will occur than when it will—and how much optionality remains when it does.

A growing body of market commentary in Korea has begun to frame personal financial resilience around a handful of practical levers. The first is ‘diversification’ across assets that behave differently under stress. Portfolios heavily concentrated in local real estate, domestic equities, and won-denominated deposits may look stable in calm conditions, but they can become highly exposed to a single macro regime—Korea’s housing cycle, domestic liquidity conditions, or currency swings. By contrast, a mix of domestic and foreign holdings, real and financial assets, and traditional instruments alongside some digital exposure can reduce the probability that one shock dominates the entire balance sheet.

Second is building income streams beyond wages. As corporate employment becomes less predictable—and as AI reshapes white-collar and creative work—dependence on a single paycheck is increasingly viewed as a structural risk. The emphasis in this line of thinking is not on overnight gains, but on gradually creating at least one auxiliary cash-flow channel tied to an individual’s own capabilities: a side business, investment income, or content-linked revenue. The aim is ‘redundancy’—a system that does not fail all at once if one node breaks.

Third is managing leverage. Debt can enhance returns in benign environments, but it also compresses choice in downturns, forcing sales into weakness and narrowing the ability to seize opportunities when valuations reset. In that sense, savings is reframed less as passive accumulation than as the purchase of ‘optionality’—the ability to wait, move, or endure when conditions tighten.

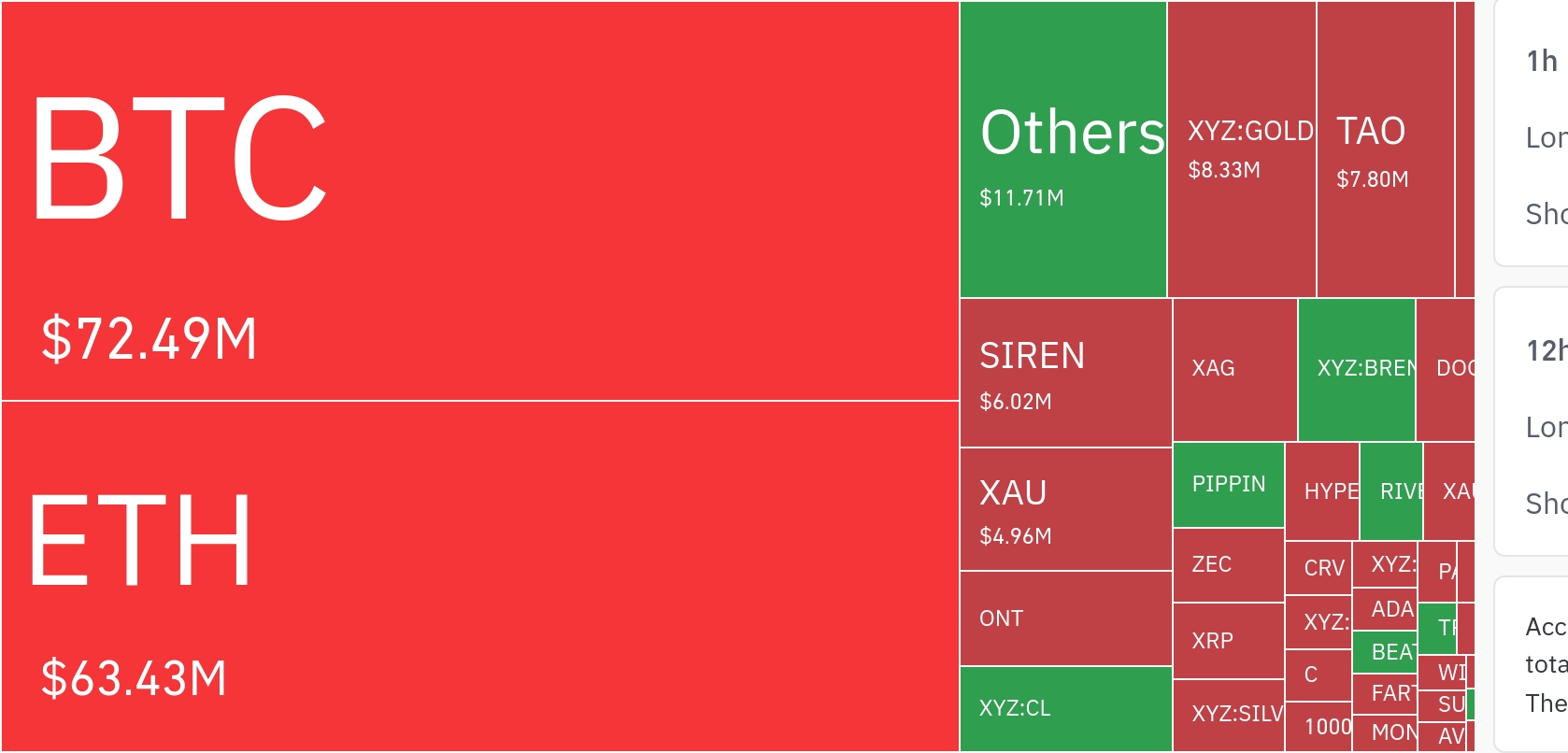

Where the discussion intersects most directly with crypto is in the argument that Bitcoin (BTC) should be understood not merely as a speculative asset, but as an ‘infrastructure’ for value storage and transfer. Bitcoin’s core proposition is that holdings can be secured and moved without reliance on a bank, brokerage, or cross-border permissioning process. In theory, a user controlling their private keys can transact globally with only an internet connection, making BTC a tool for geographic portability that traditional accounts do not always match—particularly during periods of capital controls, banking instability, or friction in opening overseas financial access.

That framing, however, comes with an operational caveat increasingly repeated by long-time market participants: custody matters. Keeping BTC on an exchange may be convenient, but it also means delegating control to an intermediary—reducing the very ‘self-sovereign’ characteristics that distinguish the asset. Self-custody, while requiring stronger security habits, is often presented as the mechanism that preserves Bitcoin’s borderless utility.

Finally, the editorial view emphasizes an intangible asset: independent judgment. In an environment saturated with real-time feeds, influencer narratives, and viral sentiment, the scarce skill is not information gathering but evaluation—verifying claims, separating signal from noise, and maintaining a time horizon long enough to outlast cycles. The ability to resist crowd behavior, proponents argue, can become a longer-lasting edge than any single trade.

The practical takeaway is incremental rather than dramatic. Opening a small overseas ETF account, testing a modest amount of BTC in self-custody, or even documenting side-project ideas are framed as low-cost first steps that can expand choices years later. In a period defined by policy uncertainty, technological disruption, and shifting liquidity, the most fragile position may be inertia—falling behind the pace of change until options quietly disappear.

For global markets, the implication is straightforward: resilience is increasingly being treated as a portfolio design problem as much as a macro forecast. Whether the next shock comes from regulation, geopolitics, or credit, individuals and institutions alike are being pushed toward the same goal—building structures that can bend without breaking when the external environment turns.

Comment 0