News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

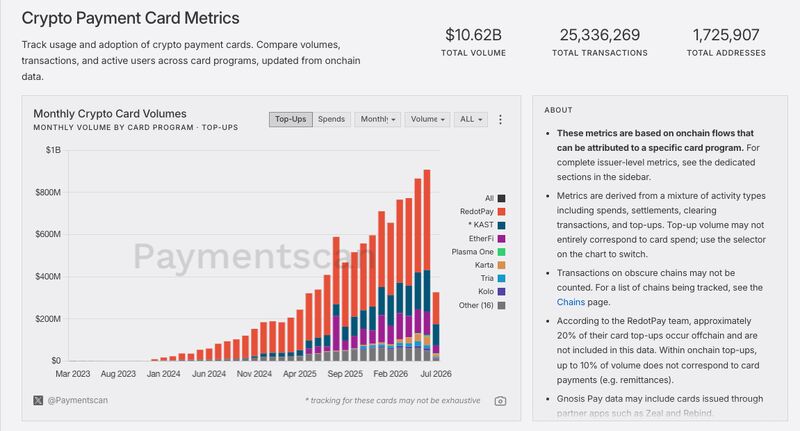

Crypto-linked payment cards have surpassed $10.62 billion in cumulative onchain spending volume, underscoring how stablecoin-based “card rails” are moving from early experimentation toward wider everyday use. New data suggests the sector’s growth has shifted markedly in the past year, with monthly top-ups accelerating at a pace more consistent with an early ‘mass adoption’ phase than a slow-burn niche product.

The figures come from Paymentscan, an onchain payments data analytics platform that tracked crypto payment card activity from March 2023 through July 2026. Over that period, Paymentscan recorded roughly 25.33 million transactions tied to about 1.72 million active addresses, with total processed volume reaching $10.62 billion.

The most notable takeaway is the market’s changing growth profile. Paymentscan’s dataset splits into two distinct phases: an initial “infrastructure build” period marked by gradual gains, followed by a sharper expansion phase beginning in late 2025.

From March 2023 through mid-2025, monthly top-up volume rose steadily but slowly, taking nearly two years to reach around $400 million. That period aligns with foundational work across the ecosystem—issuer onboarding, integration with payment networks, and the slow process of acquiring and retaining card users who can reliably fund and spend from onchain balances.

After September 2025, however, the curve steepened. Monthly top-ups roughly doubled over about 10 months, approaching $900 million around June 2026. In chart terms, Paymentscan’s data implies that the volume accumulated over the most recent 10 months is comparable to what the market built during the prior two and a half years—an inflection that points to broader adoption rather than incremental growth.

Usage intensity also appears to be increasing. Based on Paymentscan’s totals, 1.72 million active addresses generated 25.33 million transactions—about 15 transactions per address on average. While active addresses cannot be cleanly equated to unique individuals (a single user can control multiple wallets), the repeat-use density is more consistent with routine spending than one-off testing. For a subset of users, crypto cards may be shifting from a backup option to a primary ‘day-to-day payment’ method.

Paymentscan’s transaction mapping indicates that stablecoins underpin most of this activity. Top-ups are typically executed via onchain transfers of dollar-pegged tokens such as Tether (USDT) and USD Coin (USDC), then routed through card programs that convert the stablecoin balance into a point-of-sale purchase experience. The scale—tens of millions of transactions—adds weight to the argument that stablecoins are increasingly functioning as practical ‘payment instruments’ rather than purely trading collateral.

At the same time, the market structure appears highly concentrated by program. Paymentscan’s breakdown shows RedotPay accounting for a dominant share of observed activity, with other programs such as KAST, EtherFi, Plasma One, Karta, Tria, and Kolo trailing at a significant distance. With much of the growth clustered among Asia-based issuers, that concentration raises sensitivity to program-level policy changes, banking partner shifts, or regulatory developments that could ripple through headline metrics.

In absolute terms, $10.62 billion remains small against global card payment giants. Visa ($V) alone processes on the order of $15 trillion annually, making the crypto-card total equivalent to less than a day of Visa’s throughput. Still, the signal Paymentscan emphasizes is not scale but slope: the recent acceleration suggests expanding distribution and improving product-market fit, particularly as stablecoins continue to offer fast settlement and relatively low-friction cross-border value transfer.

The trend also carries implications for South Korea’s payments landscape. Paymentscan characterizes the current adoption curve as being built on dollar-based stablecoin rails, even as South Korea remains in the discussion stage around a won-denominated stablecoin. In the absence of a widely used KRW stablecoin, a central question is which issuer networks and settlement currencies will capture domestic onchain payment demand as crypto cards and stablecoin-linked spending become more common at the point of sale.

🔎 Market Interpretation

- Crypto card rails are exiting the pilot stage: Cumulative onchain-funded card spending has surpassed $10.62B, signaling stablecoin-based card funding is becoming a repeat-use consumer payment behavior rather than isolated trials.

- A clear inflection began in late 2025: Paymentscan data shows two phases—(1) slow “infrastructure build” from Mar 2023–mid 2025, then (2) rapid expansion starting around Sep 2025, consistent with an early mass-adoption curve.

- Growth is driven by faster top-up velocity: Monthly top-ups took ~2 years to reach ~$400M, then roughly doubled in ~10 months to ~$900M by Jun 2026—implying the market added in ~10 months what previously took ~2.5 years.

- Stablecoins are acting like payment instruments: The dominant funding method is onchain transfers of USDT/USDC into card programs that deliver normal point-of-sale experiences, strengthening the case that stablecoins are moving beyond trading collateral.

- Concentration risk is high: Activity is heavily clustered in a small number of programs (notably RedotPay), with many issuers Asia-centered—making the sector sensitive to issuer policy changes, bank partner disruptions, or regulatory shocks.

- Scale is small vs. traditional rails, but the slope matters: $10.62B cumulative is tiny compared with Visa’s ~$15T/year, yet the acceleration suggests improved distribution and product-market fit (especially for cross-border and low-friction settlement use cases).

- South Korea implication: Adoption is currently built on USD stablecoin rails while KRW-stablecoin discussions continue; the competitive question becomes which issuer networks and settlement currencies will capture Korea’s onchain payment demand.

💡 Strategic Points

- Watch monthly top-up run-rate as the core KPI: Top-ups are a leading indicator of spending capacity; continued growth from the ~$900M/month area would confirm broader daily-use penetration.

- Assess issuer/program dependency: With RedotPay dominating observed activity, investors and operators should model downside scenarios tied to program rule changes, banking partner churn, or region-specific compliance actions.

- Product-market fit appears strongest where traditional friction is high: Stablecoin-funded cards can outperform in cross-border contexts (faster settlement, fewer intermediaries), suggesting expansion will likely track remittance, travel, and international e-commerce corridors.

- Behavioral signal: repeat usage is rising: ~25.33M transactions across 1.72M active addresses (~15 tx/address) indicates a meaningful subset of users are spending repeatedly, not just testing once.

- Interpret “active addresses” carefully: Wallet addresses are not equal to unique users; growth could reflect multi-wallet behavior. Pair address metrics with transaction frequency and value per top-up to gauge true adoption.

- For Korea-focused stakeholders: If KRW stablecoin rollout lags, USD stablecoin rails may become the de facto onchain payment layer—raising policy questions around FX exposure, consumer protection, and domestic settlement preferences.

📘 Glossary

- Onchain spending volume: The total value of transactions that occur via blockchain transfers and are linked to card top-ups/spending flows.

- Top-up: Funding a payment card program by transferring crypto/stablecoins into the card account balance.

- Stablecoin: A token designed to track a fiat currency value (commonly USD), e.g., USDT (Tether) and USDC (USD Coin).

- Card rails: The underlying payment network infrastructure (e.g., card networks, issuer processing, settlement) that enables point-of-sale card payments.

- Active address: A blockchain address that participated in transactions during the measured period; not a direct proxy for unique individuals.

- Issuer: The entity/program that provides the card product, handles onboarding, compliance, and relationship with banking/payment partners.

- Product-market fit (PMF): Evidence that a product satisfies a real market demand, often reflected in accelerating usage and repeat behavior.

- Inflection point: A shift in growth pattern where adoption transitions from gradual increases to rapid acceleration.

Comment 0