News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

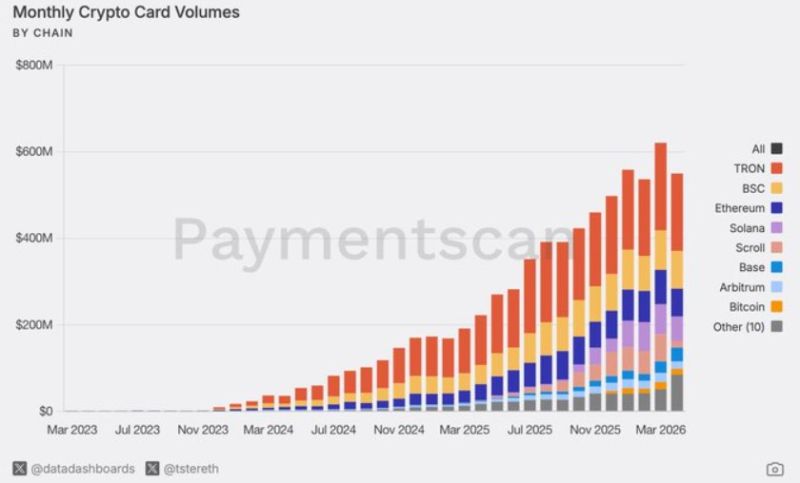

Two numbers are increasingly shaping the direction of the crypto economy: roughly $600 million in monthly crypto card payments and a $5.58 billion onchain credit market. Together, they point to the same inflection—stablecoins are moving from a speculative parking asset toward functioning financial infrastructure that touches everyday spending and real-world borrowing demand.

The payments side has accelerated quickly. Crypto card transaction volume was close to negligible in early 2023, but the curve began to change around September 2024. Over the following eight months, volumes climbed more than 500%, surpassing $600 million per month by March 2026, according to the data cited in the report.

Chain-level activity suggests that stablecoin payments are flowing where transaction costs are low and settlement is fast. TRON and BNB Chain (BSC) account for a significant portion of volume, with Ethereum (ETH), Solana (SOL), Base, and Arbitrum following behind. That distribution highlights a practical shift: users are choosing networks less for narrative appeal and more for utility and cost efficiency.

A key takeaway is the role of traditional card rails. Visa has captured around 90% of the crypto card market in the dataset, underscoring that this growth is not happening in isolation from legacy finance. Visa’s approach, as described in the analysis, is to reduce dependence on traditional sponsor-bank structures and instead form direct partnerships with newer blockchain infrastructure providers—effectively retooling the card network to run atop stablecoin settlement rails.

One fast-growing example cited is Jupiter Global, a crypto card service offering 4% to 10% cashback. The service reported an April transaction-volume jump of more than 660% month over month, illustrating how familiar consumer incentives—card rewards and rebates—are being replicated onchain. If rewards and user experience converge with mainstream credit cards, crypto cards no longer need to win on ideology; they can compete on economics.

Market pricing appears to be reacting to that thesis. An IMF empirical study published in March 2026 (WP/26/52) found that after passage of the GENIUS Act, the market capitalization of companies focused on cross-border payments fell by about 27%, signaling investor expectations that stablecoin-based payment infrastructure could displace portions of incumbent business models. In that sense, the crypto card metric has become a real-time indicator of how quickly the market’s bet is translating into consumer behavior.

Yet the larger story may be what happens off the checkout page. The analysis estimates that total onchain stablecoin supply is roughly $300 billion—far more than what is currently being used for payments. Much of that capital remains idle, generating little or no productive yield while waiting for a credible destination.

Early DeFi yields were often internal and self-referential: token incentives, leverage loops, liquidity mining, and rehypothecation of the same collateral to chase more emissions. The system could be lucrative, but it largely relied on crypto-native demand—money circulating inside a closed loop rather than funding activity tied to the broader economy.

That is where 'onchain credit' enters as a potential next leg of stablecoin utility. Instead of relying on speculative demand, the yield is framed as coming from real-world borrowing needs: businesses, funds, fintech platforms, and credit intermediaries borrowing stablecoins to finance operations and cash-flow needs. The onchain credit market is reported to have grown about 22x in 2025, from $252 million to $5.58 billion.

In the broader tokenization landscape, the report places onchain credit at roughly 17.3% of a $30 billion 'RWA' (real-world asset tokenization) market, with projections that the wider RWA sector could approach $4 trillion by 2030. Whether that trajectory ultimately materializes remains uncertain, but the implication is clear: if stablecoin supply is already in the hundreds of billions, crypto-native venues alone may not be large enough to absorb it productively.

Scale is the crux. A $300 billion stablecoin base looking for sustainable yield needs a market vast enough to deploy capital without depending on reflexive crypto leverage. The analysis argues that the only market with that capacity is the real economy’s credit complex—and that onchain credit is the bridge that could route stablecoin liquidity into that demand.

This frames a broader evolution in DeFi. The first generation of decentralized finance proved it could create liquidity and attract capital onchain at unprecedented speed. The second generation question is harder: can that liquidity be made to 'work' in the real economy rather than circulating within crypto’s own incentive structures?

Crypto cards offer one answer at the consumer layer, demonstrating that stablecoins can function as a spending instrument. Onchain credit is attempting to answer the same question at the capital-allocation layer, turning stablecoins into a source of financing rather than a passive store of value. The concurrent growth of both markets suggests the shift is not theoretical. With monthly payments surpassing $600 million and onchain credit expanding rapidly, the market is increasingly signaling that stablecoins’ next destination may be less about speculation—and more about becoming a durable component of modern financial plumbing.

🔎 Market Interpretation

{

"core_signal": [

{

"metric": "$600M+ monthly crypto card payments",

"what_it_implies": "Stablecoins are being used as everyday spending money rather than just a liquidity ‘parking’ asset.",

"trend": "Crypto card volume rose 500%+ over ~8 months, reaching $600M/month by March 2026 after being near-negligible in early 2023."

},

{

"metric": "$5.58B onchain credit market",

"what_it_implies": "Stablecoin utility is expanding into real-economy credit demand (working capital, financing) instead of circular DeFi leverage.",

"trend": "Estimated 22x growth in 2025 (from $252M to $5.58B)."

}

],

"network_and_rail_dynamics": [

{

"observation": "Most stablecoin payment activity clusters on low-fee, fast-settlement chains.",

"chains_highlighted": ["TRON", "BNB Chain (BSC)", "Ethereum", "Solana", "Base", "Arbitrum"],

"interpretation": "User behavior is shifting from narrative-driven chain preference to cost/utility-driven choice."

},

{

"observation": "Legacy card infrastructure remains central.",

"detail": "Visa represents ~90% of crypto card volume in the referenced dataset.",

"interpretation": "Adoption is occurring through integration with existing rails rather than replacing them outright; Visa is repositioning toward direct partnerships with blockchain infrastructure providers and stablecoin settlement."

}

],

"market_pricing_readthrough": [

{

"study": "IMF WP/26/52 (March 2026)",

"event": "Passage of the GENIUS Act",

"reported_effect": "Cross-border payments-focused companies’ market caps fell ~27%",

"interpretation": "Investors are pricing stablecoin payment rails as a competitive substitute for portions of incumbent cross-border payment models."

}

],

"bigger_context": [

{

"constraint": "Stablecoin supply is ~ $300B, far larger than today’s payment throughput.",

"implication": "Even strong payment growth may not absorb supply; the key question becomes where sustainable yield and productive deployment comes from."

},

{

"thesis": "Onchain credit is positioned as the bridge from idle stablecoin liquidity to real-economy borrowing demand.",

"why_it_matters": "Scaling productive yield likely requires a market as large as the broader credit complex, not purely crypto-native leverage loops."

}

]

}

💡 Strategic Points

{

"what_to_watch_next": [

{

"indicator": "Crypto card monthly volumes and active users",

"why_it_matters": "Acts as a near real-time proxy for stablecoin consumer adoption and merchant acceptance; sustained growth suggests stablecoins are becoming ‘spendable cash.’"

},

{

"indicator": "Onchain credit outstanding and borrower mix",

"why_it_matters": "A shift toward business/fintech/credit-intermediary borrowing would signal yield is coming from exogenous demand rather than internal DeFi incentives."

},

{

"indicator": "Chain distribution of payment flows",

"why_it_matters": "Persistent dominance by low-fee networks implies cost sensitivity is decisive; infrastructure and UX are likely to matter more than brand narratives."

},

{

"indicator": "Card-network strategy (Visa partnerships, settlement paths)",

"why_it_matters": "If major networks keep migrating settlement toward stablecoin rails, stablecoins become embedded inside existing payment plumbing rather than living at the periphery."

}

],

"competitive_implications": [

{

"theme": "Incumbent payments pressure",

"detail": "The IMF-reported 27% market-cap drawdown suggests markets expect stablecoins to compress margins in cross-border payments and potentially reduce reliance on certain intermediaries."

},

{

"theme": "Rewards as adoption lever",

"detail": "High cashback (e.g., 4%–10%) and familiar card UX can shift the value proposition from ideology to economics, accelerating mainstream uptake if unit economics are sustainable."

}

],

"risk_and_open_questions": [

{

"question": "Are reward programs (4%–10% cashback) durable?",

"risk": "If rewards are subsidy-driven, volumes may be incentive-sensitive rather than structurally sticky."

},

{

"question": "Is onchain credit truly real-economy linked?",

"risk": "If lending demand remains mostly crypto-native or recursively collateralized, ‘productive yield’ may revert toward reflexive leverage dynamics."

},

{

"question": "Regulatory and compliance trajectory",

"risk": "Stablecoin and payments regulation could shift rapidly; the GENIUS Act’s impact shows policy changes can reprice whole sectors."

},

{

"question": "Scalability and credit risk management",

"risk": "To deploy a $300B stablecoin base, underwriting, default management, and transparency standards must scale without recreating opaque risk."

}

],

"practical_takeaways": [

{

"for_market_participants": "Treat crypto card volume and onchain credit growth as complementary adoption metrics—consumer checkout + capital allocation—both needed for ‘financial infrastructure’ status."

},

{

"for_builders": "Optimize for cost, settlement speed, and compliance-ready integrations; users are signaling preference for utility-first networks and familiar rails."

}

]

}

📘 Glossary

{

"terms": [

{

"term": "Stablecoin",

"definition": "A crypto asset designed to maintain a stable value (often pegged to USD), used for payments, trading, and increasingly credit/financing."

},

{

"term": "Crypto card payments",

"definition": "Card transactions funded by crypto (often stablecoins) where settlement and/or funding flows occur via blockchain while using traditional card acceptance networks."

},

{

"term": "Card rails",

"definition": "The legacy payment network infrastructure (e.g., Visa) that routes authorization, clearing, and settlement for card transactions."

},

{

"term": "Stablecoin settlement rails",

"definition": "Payment settlement processes that move value using stablecoins onchain, potentially reducing intermediaries and cross-border friction."

},

{

"term": "Onchain credit",

"definition": "Borrowing and lending activity executed via blockchain-based platforms, where stablecoins are lent to borrowers and repaid with interest."

},

{

"term": "DeFi (Decentralized Finance)",

"definition": "Blockchain-based financial services (trading, lending, derivatives) executed via smart contracts rather than traditional intermediaries."

},

{

"term": "Liquidity mining",

"definition": "Incentivizing users to provide liquidity by paying token rewards; can drive growth but may be subsidy-dependent."

},

{

"term": "Rehypothecation",

"definition": "Re-using the same collateral multiple times to back additional borrowing, increasing leverage and interconnected risk."

},

{

"term": "Leverage loops",

"definition": "Strategies where borrowed funds are recycled to acquire more collateral and borrow again; can inflate yields and risk without external demand."

},

{

"term": "RWA (Real-World Assets) tokenization",

"definition": "Representing claims on real-economy assets (e.g., bonds, invoices, private credit) as tokens onchain to enable programmable finance and wider distribution."

},

{

"term": "Cross-border payments",

"definition": "Payments sent across countries/currencies; often high-friction and a key area where stablecoin settlement may reduce costs and time."

},

{

"term": "GENIUS Act",

"definition": "A referenced regulatory milestone in the article’s cited IMF study; associated with a market repricing of cross-border payments firms after passage."

}

]

}

Comment 0